Wayside Technology: Get Ready To Be Bored, And Profitable (NASDAQ:WSTG)

NicoElNino/iStock via Getty Images

While Meta (FB) is speaking about transforming the world, and arguments are being had about how Alphabet (GOOGL) may own the internet if we don't get Web3 going, there is a small little company that is quietly increasing cash flow and returning profits to shareholders over the past few years.

This company is Wayside Technology Group, Inc. (WSTG). This little company has continually shown to increase cash flow and has a great business structure that allows them to have spotless financials. They have set themselves up for a very profitable and growing future.

Let's dig in...

Company Description

Wayside is a global IT channel company providing both distribution and cloud technology solutions through its Climb (distribution), TechXtend (US reseller), Grey Matter (UK and Ireland reseller) and Cloud Know How (professional services) operating segments. We specialize in emerging technology vendors, distributing their products to 4,000 + partners worldwide. -- Taken from waysidetechnology.com

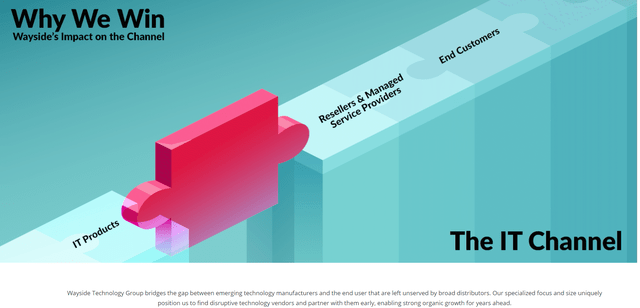

Let's simplify it even more with a great little picture from their website:

waysidetechnology.com

To put this another way, think about Wayside being the group that sells vacation packages to the travel agents to sell to those going on vacations. Traveling to Paris sells itself, much like Microsoft's software. But what about a trip to Africa? You aren't going to just go on, buy a ticket, and fly into a vacation there, you need some help from the agent who needs help to find packages to sell you. This is much like one of Wayside's IT partner's products, such as Cloudian, a hybrid cloud data management software.

It's tough to connect to resellers if you are a company in this niche without having someone that can partner it up. Spend money on a full marketing firm and salesmen or simply partner with Wayside? They put the product in the resellers' hands and educate them about how and who to sell it to. Not only that, but they also offer in-house continuing assistance with product help.

If it seems simple, it is. And I love that.

MOAT

For those unfamiliar with moat, it is the ability for a company to maintain their competitive advantage and fend off competition. This is just like the protection of the medieval moats that were found around castles. I primarily like the description and categories of moat found here by Phil Town of Rule 1 Investing. I won't go into each one here, so I encourage you to read about them if you are unfamiliar.

So what moat does WSTG have?

This can always be a place of argument depending on how you view the strength and weaknesses of a company but I see one major moat that fits Wayside.

That moat is Switching.

Most companies that partner with Wayside do it for the simple reason that Wayside knows resellers, knows how to educate these sellers, and knows how to ultimately help get products into the customers' hands. Companies that have partnered with them already are seeing benefits and moving out of that to switch to another company costs resources (time and money). This seems unlikely once they partner with a vendor.

Add to that the fact that Wayside recently became an approved vendor of the NCPA, a national government purchasing co-op, and you can see the reach extending enough to create some safety in the business.

Pros/Cons

Pros:

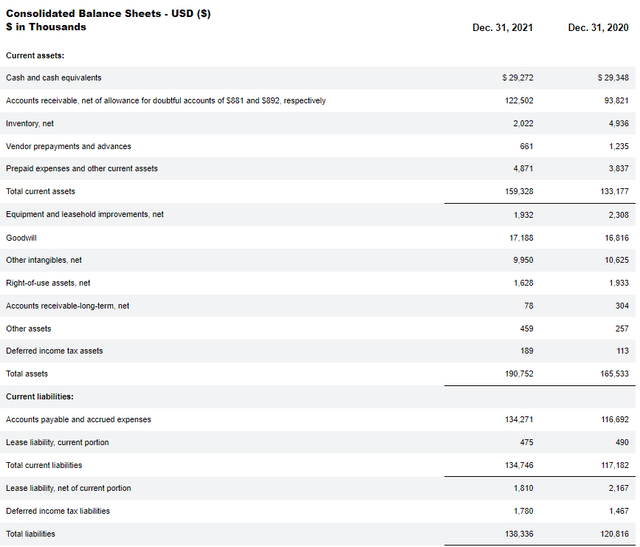

No Debt. My oh my, there are a few things that I love in life, and finding a profitable company that has a balance sheet clear of debt is one of them. WSTG has done a phenomenal job developing a business plan that would allow for slow and steady cash flow growth without needing debt. Take a look at their most recent balance sheet below and you will see what I mean.

WSTG IR

Cash on Hand. Having no debt is one thing, but having a significant amount of cash on hand for M&A is another. Wayside checks off both boxes and has had a recent history of making solid acquisitions. In 2020, Wayside closed on two acquisitions, Interwork Technologies ($3.6m) and CDF Group ($17.4m).

Here's a quote about CDF from their latest 10-K:

Distribution segment gross profit for the year ended December 31, 2021 increased 25%, or $7.4 million, to $36.5 million compared to $29.1 million for the same period in 2020. The increase in Distribution segment gross profit resulted primarily from the impact of the acquisition of CDF and Interwork acquisitions for the full year ended December 31, 2021 and lower early pay discounts and other rebates and discounts offered to our customers as a percentage of adjusted gross billings.

Solutions segment gross profit for the year ended December 31, 2021 increased 135%, or $5.3 million, to $9.2 million compared to $3.9 million for the same period in 2020. The increase in Solutions segment gross profit resulted primarily from increased sales from the acquisition of CDF for the full year ended December 31, 2021.

These are lovely numbers to see and show that management is very precise in what they are using cash to acquire. They have recently stated that they will continue to look for additional acquisitions to increase geographic reach and even stated that they were willing to take on some long-term debt to acquire a business if it is "transformative".

Security/Data Products. This is simply common sense. We are continuing to drive into a world that is online, and with that data management and the security that surrounds it are paramount. The fact that Wayside has a portfolio of products that do just this gives me hope for future growth.

Cons:

Not Diversified. Most of the time when I am looking at companies that rely on vendors, such as REITs, I do not want to see a business that lacks diversification in their revenue streams. This is the same when it comes to Wayside. One potential problem that I see with their current revenue is that two vendors (CDW Corporation & Software House International) account for about 25% of consolidated net sales and two customers (Sophos & SolarWinds) accounted for 30% of consolidated purchases. This is a significant risk if something happens to these vendors/customers and something to watch closely as they move forward.

Acquisition Dependent. Now I don't want to get really doom and gloom here because we just went in depth how acquisitions are a strength, but so is organic growth. The new NCPA should help but it seems reasonable to say that Wayside's growth will depend highly on future acquisitions. While management has shown the ability to be competent at this in the past, it doesn't mean they will be in the future. Not a red flag here, but another thing that should be in the investor's mind.

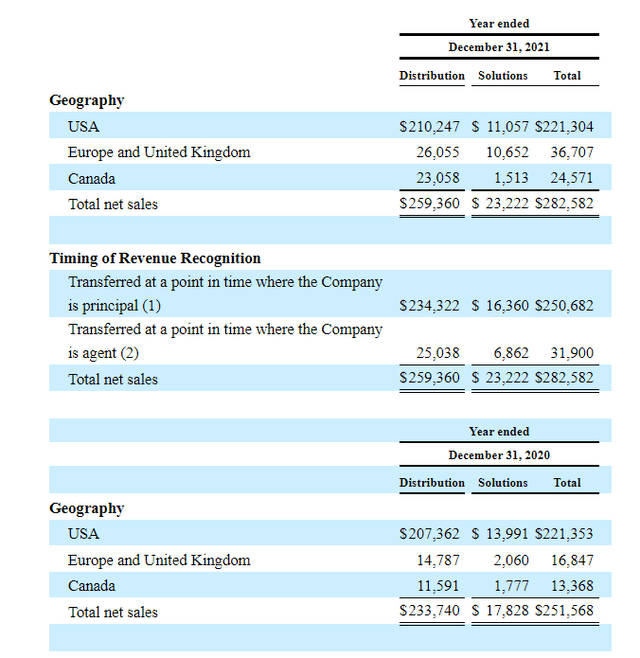

Stagnant US Revenue YoY. While Wayside has been growing in a lot of places, sales in the US over the past year has not been one of them. Year-over-year numbers in the US were almost identical to 2020 while most of their growth came from the Europe/UK region (125%) and Canada (85%). While stagnancy in the US may seem small in comparison to the growth outside, we must take into account that Wayside does 78% of its sales in the states.

WSTG 10-K

Valuation

Now I have my own method of valuing companies, much like those that write these articles. Valuations, no matter how you do them, always take a certain amount of speculation, whether it is organic growth, acquisitions, future debt refinancing, changes to the landscape of the industry, effects of inflation, etc.

When performing estimates of a company's value, I like to look at them in through two different lenses. These lenses include:

- EPS-based Valuation with Dividend (5 years)

- Free Cash Flow Valuation (8 years)

Let's begin with the EPS valuation.

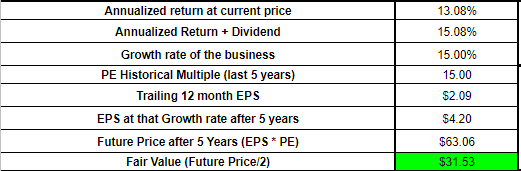

Since taking a historical average would be inconsistent at this point, I will have to take some liberties with WSTG here. I see WSTG as a company that can very well grow their EPS at a 15% clip over the next five years without much of an issue due to acquisitions and the future of the industry that they are in. Presented below is how I run those numbers.

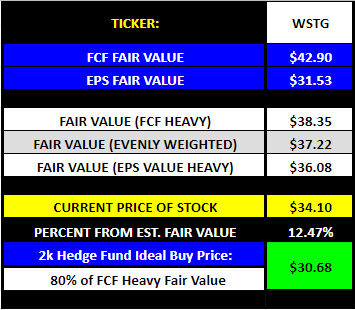

My Spreadsheet

This equation is somewhat simplistic as you can see but presents me with a good idea of the company from a pure EPS format. With WSTG, you can see that it is trading currently above my estimated fair value and would return around 15% per year over the next five years. Not bad as it does double my money in five years.

This isn't the full picture though.

My second equation is based off of free cash flow, which in my equation is simply operating cash flow minus maintenance capital expenditures combined with growth and discount rates (aka Buffett owner's earnings). Here is what that looks like on paper.

My Spreadsheet

I typically will take a look at historical rate of FCF growth and make an educated guess at the future rate, but WSTG has been a bit all over the place over that time period, with new management taking the helm as well. I went ahead and stuck with the 15% I used in the EPS valuation for the first four years, then slowed it to 10% per year for the last four years. As for the discount rate, I will continue to use a 3% discount rate until the 10-year treasury reaches higher levels.

One thing that is a little bit different than The Oracle is that I use an 8-year instead of a 10-year calculation. Why is this? Well, I stole this one from Phil Town as well, where he speaks about the payback time that private equity investors expect. He literally wrote a book about this, so instead of me wading through it, I suggest you take a look at his explanation.

Finally, there is one last step, which is how to combine the two calculations. There are a couple of ways to do this. First, I could take a 50/50 split and average the two prices. Second, I could assume that the next 8-10 years of stock price depends more on FCF growth and label it 60/40 in favor of the FCF calculation. Finally, my third choice is to perform the opposite and go 60/40 in favor of an EPS valuation.

My Spreadsheet

For me, I believe that the increases from WSTG will be highly related to acquisitions and may not show up in EPS immediately. This means that I will be going 60/40 towards FCF.

So what value do I place on WSTG? Currently, I value Wayside Technology at just over $38 a share. This is about 12.5% higher than its price at writing. The ability for WSTG to create free cash flow without debt and work to use its newly acquired companies to reduce costs and extend reach is a significant reason while I am sitting at this valuation.

My Buy Price

Whenever I am buying, I am looking in a five to ten-year horizon and want to be able to safely see annualized returns of around 15%. Note that I said safely, which will mean that I need to be conservative.

At the time of writing, WSTG has a yield on cost of just above 2%. That places me in a position where my returns need to be about 15% to reach or beat my goal.

What does this look like in reality? At current price ($32), a 15% annualized return for the next five years places the stock price at about $64.36. Let's set a relatively conservative PE ratio of 15 for the stock (currently ~16) and we are looking at needing the company to reach an EPS of $4.29 by the end of the year 2026.

How does this look? Well, with EPS currently sitting at $2.09 per share, then Wayside needs to produce an annualized EPS growth rate of just over 15%. This seems like a decent bet to take in my opinion, because of the possibility of large acquisitions and a growing solutions department. Ultimately, I have no problem placing my bet on beating the $4.29 estimate.

Not so fast though...

If you remember, we were using the FCF calculation for 60% of our fair value estimate, so this EPS calculation may actually not be a solid metric to look at. On a Price to FCF basis, WSTG currently sits at just above 11. According to Gurufocus.com, the average for the industry currently stands at just above 20. Let's look at Price/FCF referencing our calculations above. Year 5 produces ~$22.4m of FCF. This is about $5.21 per share (assuming no buybacks). Multiply this by 15, which is in between their current average and the industry median, and you find us sitting at $78 per share in 2026. This would be an astounding return of ~19%, which is above my goal returns.

You can see my calculator takes a default 20% off the estimated fair value for a margin of safety. With that all being said though, I feel confident to continue to invest in WSTG as long as it is below my current fair value estimate of $34 due to its financial position and M&A opportunities.

The Charts

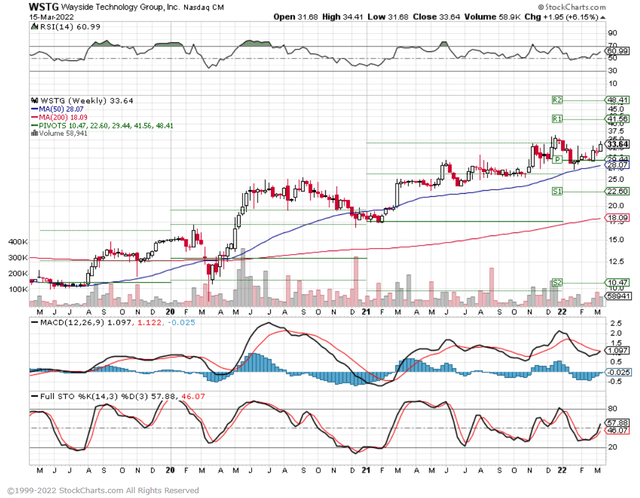

Weekly Chart:

stockcharts.com

The weekly chart for WSTG shows a stock that is close to being in prime position to buy, sitting right above support and with a MACD that is looking to make a full crossover and potentially run. Add to this a stochastic that is pointing North, a 50-day moving average that is trending in the right direction, and resistance lingering a distance away and I feel confident buying now.

Daily Chart:

stockcharts.com

The daily chart is showing a somewhat similar story with a strong MACD and current volume pointing North. WSTG has been hovering around the $29-30 mark for some time but has recently broken through the $30 resistance. Again, I would feel comfortable making a purchase here as it looks pointed to make a run at the $35 resistance.

Insiders

Checking out the trades made by insiders is always a great idea when you are looking to purchase a company. While sales only sometimes matter, buys typically carry weight for me.

Looking at the past 6 months of WSTG, there are 3 major moves:

- March 9th, 2022 - Vito Legrottaglie (VP & CIO) Sold 5,000 shares (9% of shares) @ $31.50

- December 3rd, 2021 - Andrew Clark (CFO) Purchased 200 shares (1% of shares) @ $29.90

- August 9th, 2021 - Jeffrey Geygan (Director) Purchased 2,047 shares (1.33% of shares) @ $28.97

Looking back a bit further, 2020 and 2021 were full of continuous purchases by insiders, and Vito's sale was the first since June of 2020. This points to a potential thought of overvaluation, but I would need to see more patterns of sales to make that distinction.

Conclusion

Wayside Technology Group, Inc. is quite simply a very boring company with a business that could make you fall asleep. This is precisely one of the reasons that I love it. It is simple to understand, profitable, in a growing industry, and has a flawless balance sheet.

I already own WSTG and have continued to purchase it for over a year now. After the latest earnings release and call, this pattern will continue for me until it reaches a valuation that concerns me or I get to a point where it makes up too much of my portfolio (currently >4%).

Thanks for reading. Until next time, Happy Investing!

Gloss