Verb Technology Seeks Growth Ignition From Market Launch (NASDAQ:VERB)

https://www.ispeech.org/text.to.speech

zeljkosantrac/E+ via Getty Images

A Quick Take On Verb Technology

Verb Technology (NASDAQ:VERB) recently reported its Q1 2022 financial results on May 16, 2022, missing revenue and expected earnings estimates.

The company provides organizations with various SaaS-based video software systems.

In my view, the firm has the potential to spark growth from its Market service, which is officially launching now.

Although I'm currently on Hold for VERB, interested investors should look at results from the market launch in generating actual revenue and in subsequent management comments while remaining mindful of the firm's significant work to do in reducing operating losses while stimulating growth.

Verb Technology Overview

American Fork, Utah-based Verb Technology was originally organized as Cutaia Media Group and through multiple mergers and name changes became Verb in 2019.

Management is headed by founder and CEO Rory Cutaia, who was previously a partner at the Corinthian Capital Group, a private equity firm that invested in middle market companies.

The company has created a CRM system that enables businesses to add customized calls-to-action to videos and track user clicks and engagement via its analytics engine.

Prospects can also click to buy or call the business from buttons embedded in the video, potentially increasing conversion rates in the process.

Verb has also created vertical-specific versions of the platform for healthcare, educational, television and livestreaming markets.

The market for video-centric CRM applications is difficult to determine since it is such a niche product area.

However, the strong growth of consumer and business viewing of videos continues.

Major vendors that provide CRM technologies include:

-

Salesforce (CRM)

-

SAP (SAP)

-

Oracle (ORCL)

-

Microsoft (MSFT)

-

Infusionsoft

-

Zoho CRM

Other players include global system integrators such as consulting firm Accenture (ACN) and related participants.

Verb Technology's Recent Financial Performance

-

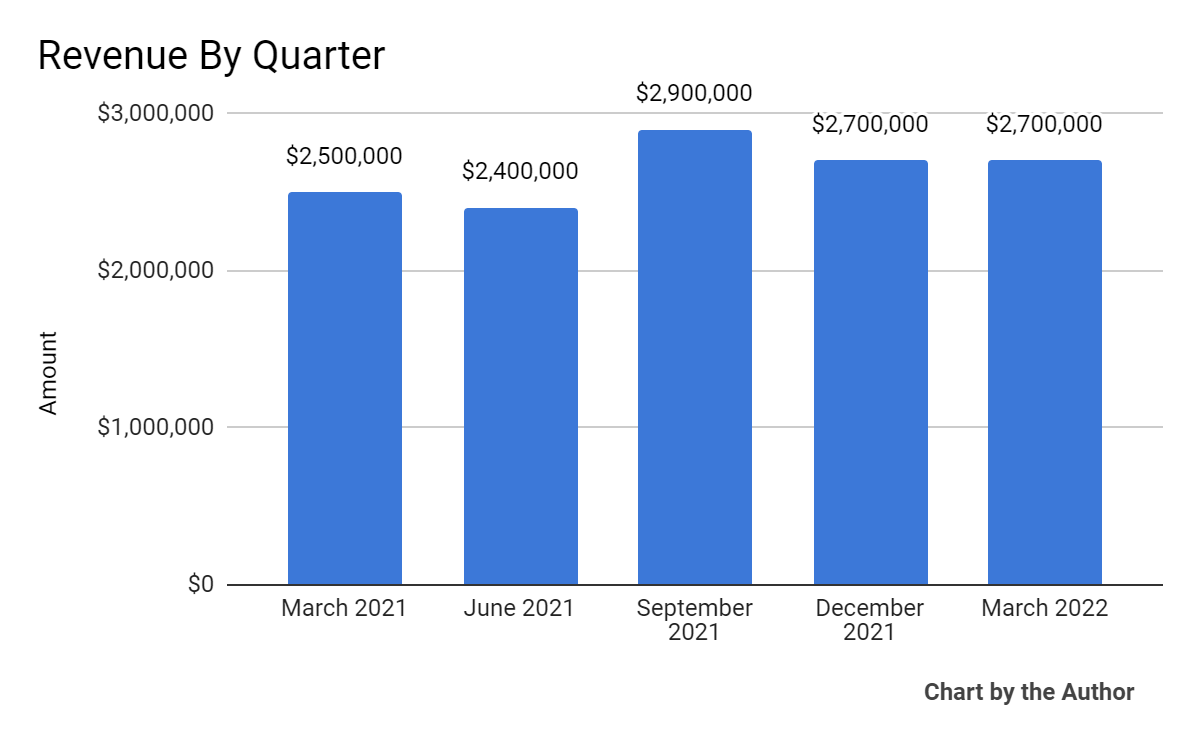

Total revenue by quarter has grown unevenly and at a slow rate of growth:

5 Quarter Total Revenue (Seeking Alpha)

-

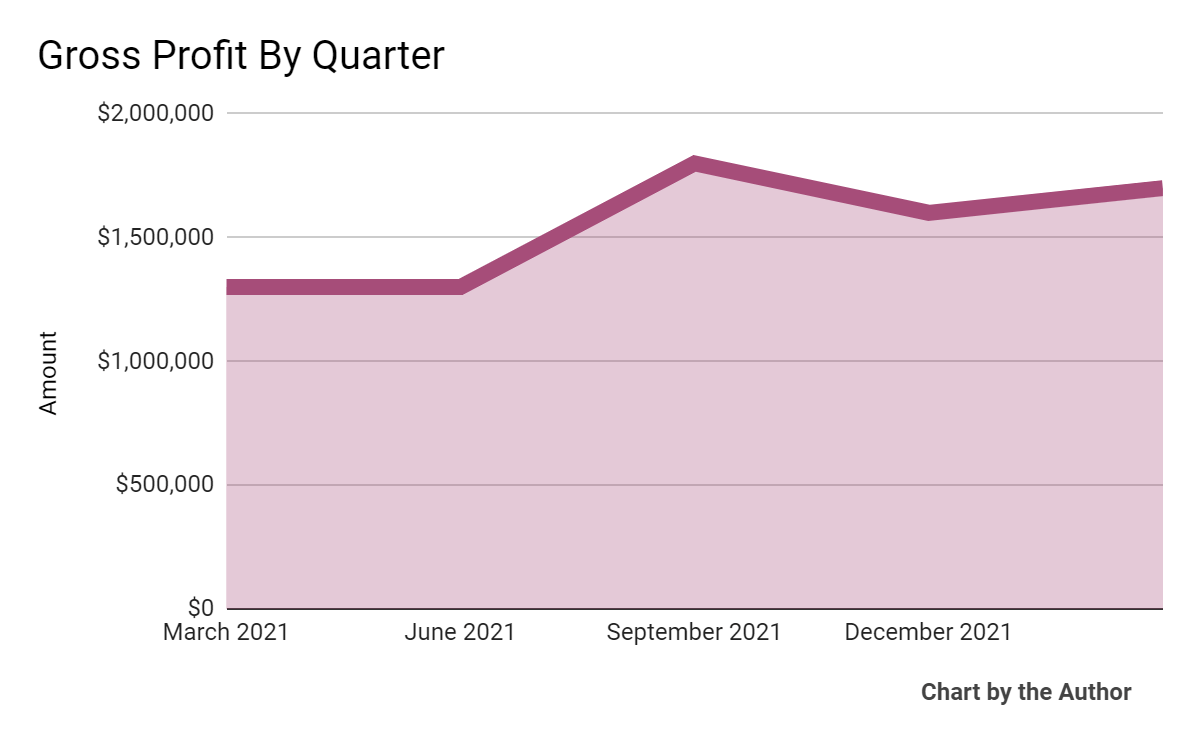

Gross profit by quarter has risen slightly:

5 Quarter Gross Profit (Seeking Alpha)

-

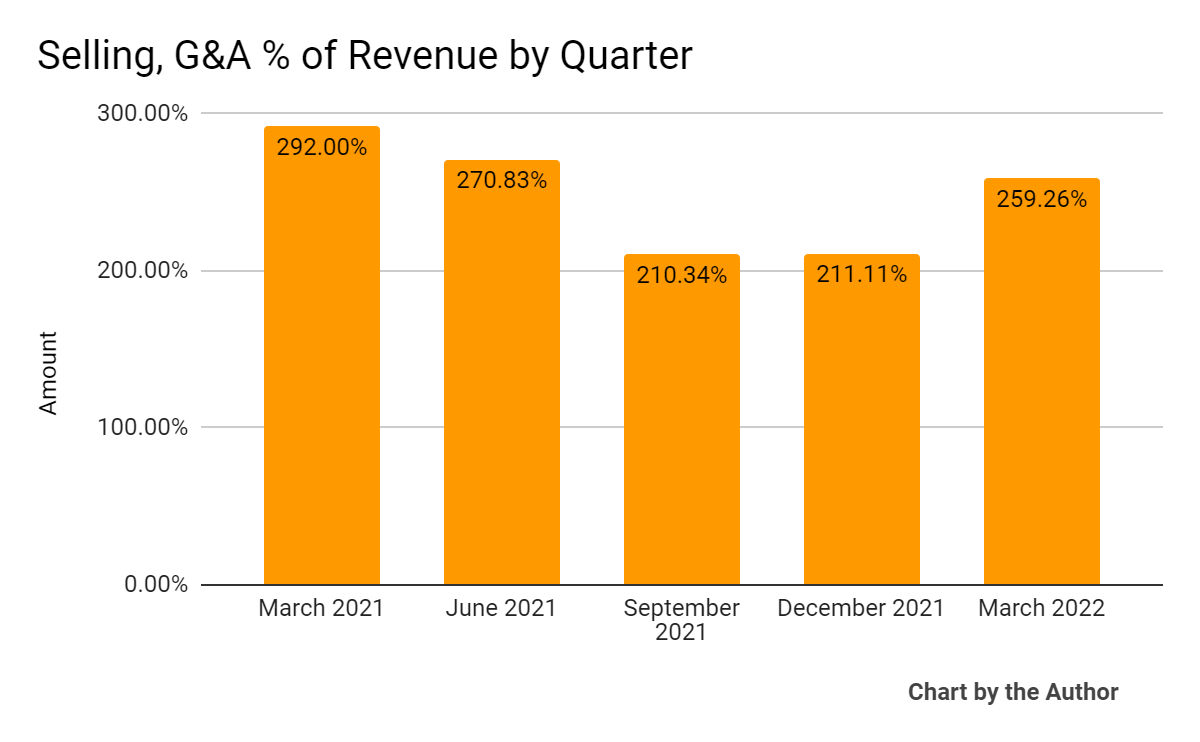

Selling, G&A expenses as a percentage of total revenue by quarter have remained extremely high:

5 Quarter Selling, G&A % Of Revenue (Seeking Alpha)

-

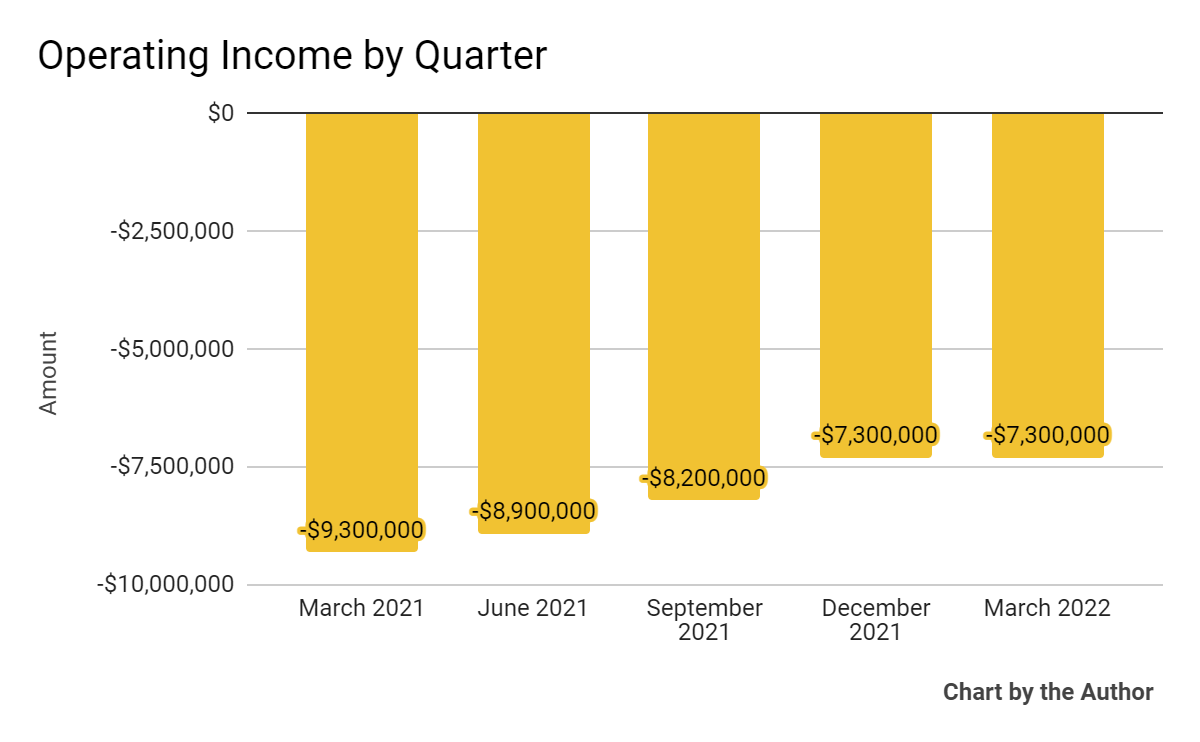

Operating losses by quarter have remained substantial:

5 Quarter Operating Income (Seeking Alpha)

-

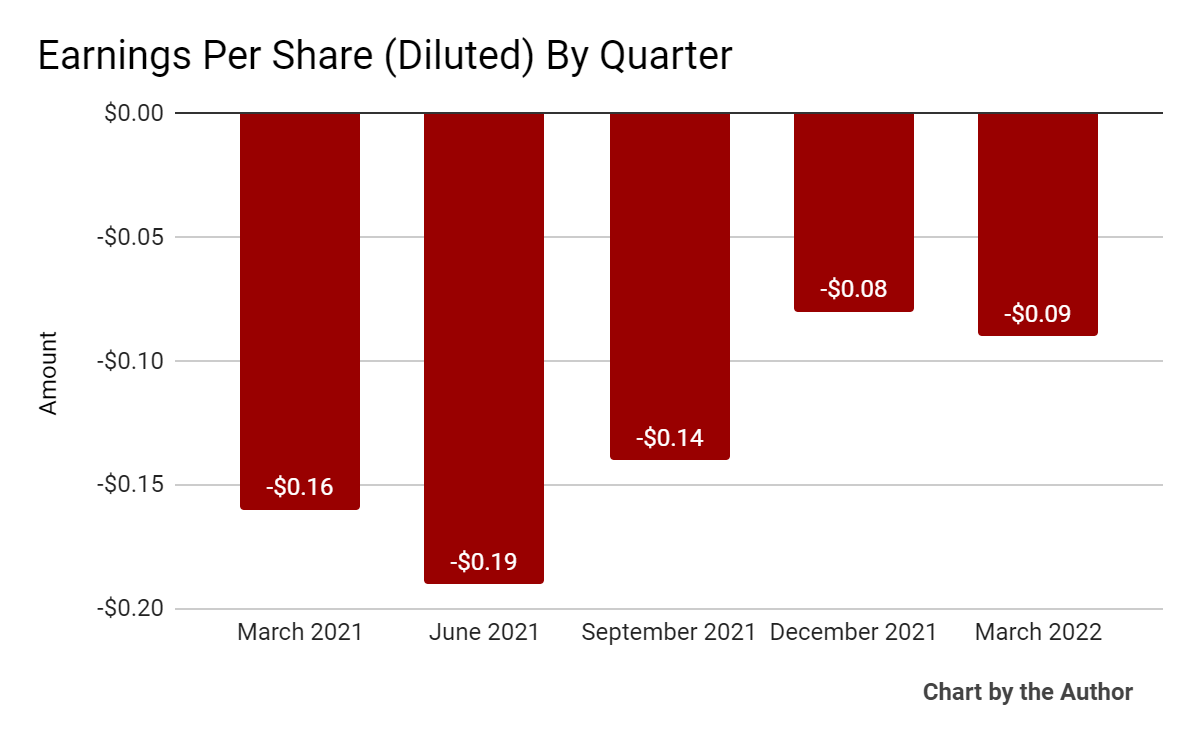

Earnings per share (Diluted) have also remained negative over the past 5 quarters:

5 Quarter Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

In the past 12 months, VERB's stock price has fallen 75.6 percent vs. the U.S. S&P 500 Index's drop of around 8.8 percent, as the chart below indicates:

52 Week Stock Price (Seeking Alpha)

Valuation And Other Metrics For Verb

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure |

Amount |

|

Enterprise Value |

$70,670,000 |

|

Market Capitalization |

$63,400,000 |

|

Enterprise Value/Sales (TTM) |

6.61 |

|

Price/Sales (TTM) |

4.06 |

|

Revenue Growth Rate (TTM) |

5.45% |

|

Operating Cash Flow (TTM) |

-$24,840,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.50 |

(Source - Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

VERB's most recent GAAP Rule of 40 calculation was negative (275%) as of Q1 2022, so the firm needs significant improvement in this regard, per the table below:

|

Rule of 40 - GAAP |

Calculation |

|

Recent Rev. Growth % |

5% |

|

GAAP EBITDA % |

-281% |

|

Total |

-275% |

(Source - Seeking Alpha)

Commentary On Verb Technology

In its last earnings call (Source - Seeking Alpha), covering Q1 2022's results, management highlighted the growth in vendor adoption of its Market system, which enables brands to 'create livestream shows that entertain and educate your audience while interacting with them in real-time.'

Verb added 100 vendors to this platform in Q1 and another 90 in the 40 days after the end of the quarter, with minimum annual sales size per vendor being $5 million to qualify for the platform.

CEO Cutaia noted extremely high sales close rates on the new system, which is launching via its Shopfest interactive festival happening July 26-28, as retail brands look for a new distribution channel for their products.

As to its financial results, total revenue grew only moderately while the SaaS revenue component grew by 37% year-over-year and represented 93% of its total revenue.

Gross margin was higher, but operating expenses remained elevated due to still-high R&D expenses related to its Market and other project development. G&A expenses dropped only slightly.

For the balance sheet, the firm finished the quarter with $3.7 million in cash and equivalents and total liabilities of $22.3 million, of which short-term borrowings and long-term debt were $8.8 million.

Looking ahead, management has 'begun implementing a top grading strict ROI approach to' its marketing efforts and expects to see material savings over time.

The firm did not provide any forward guidance expectations.

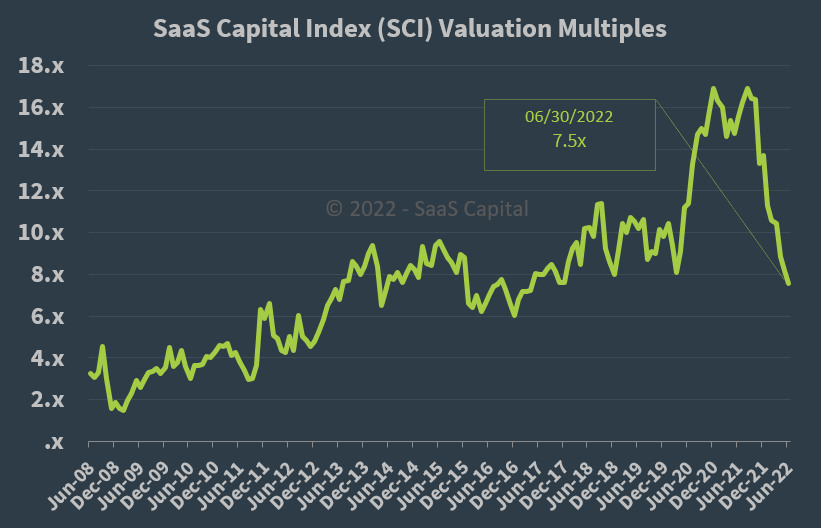

Regarding valuation, the market is valuing VERB at an EV/Sales multiple of around 6.6x.

The SaaS Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 7.5x at June 30, 2022, as the chart shows here:

SaaS Capital Index (SaaS Capital)

So, by comparison, VERB is currently valued by the market at a slight discount to the SaaS Capital Index, at least as of June 30, 2022.

The primary risk to the company's outlook is a potential macroeconomic slowdown or recession, which may slow sales cycles and reduce its potential revenue growth trajectory.

An upside catalyst would be strong adoption of its new Market platform as vendors seek alternative distribution channels that 'remove the middleman' from their cost structures.

In my view, the firm has the potential to spark growth from its Market service, which is officially launching now.

Interested investors should look at results from that launch in generating revenue and in management comments while remaining mindful of the firm's significant work to do in reducing operating losses while stimulating growth.

I'm on Hold for Verb until we see initial progress from its Market service and in reducing its operating burn.

Gloss