Smart Advisors Combine A Human Touch With New Technology

Automated technology has put pressure on advisors to remain relevant.

Financial advisors have faced massive disruption for more than a decade as automated tools, such as robo-advisors and passive investing, have captured the attention of a growing number of investors. Financial markets have thrived amid this explosion in robo-investing. However, smart advisors are counterpunching with technology of their own, turning the tables by making data analytics work for them to improve the client experience.

While disruptive robo-advisors and startups have a treasure trove of technology at their disposal, they haven’t mastered the market. That’s because the technology is powerful and useful, it’s much more effective when combined with the human touch. An informed advisor can use it to drive efficiency, improve decision making and help foster a deeper connection between themselves and their clients.

Automated technology has put pressure on advisors to remain relevant. Yet, an advisor with a high EQ, or emotional intelligence, is well-positioned to compete by offering something machines by themselves can’t match. That is the empathy of someone attuned to the ups and downs of financial markets and life. An advisor empowered with a strong team approach, focused on building relationships and supported by solid technology can draw on a formidable combination of EQ and IQ. Unlike a machine alone, a well-supported advisor can understand questions from young wage earners and early retirement savers seeking advice about whether to borrow against a 401k to buy a house or how to continue saving for college should a family's finances unexpectedly hit a rough patch.

The spread of COVID-19 is a good example of complicated real-world decision making where consulting with an advisor is advantageous. Many investors had to grapple with questions about 401k withdrawals during a period of extreme market volatility. How many of those investors had the benefit of an advisor that not only knew the numbers but also understood and could relate to the emotion and concerns over health and the economy?

Changing Behaviors

With all the complexities surrounding how we manage our personal finances, how did robo-advisers and other technological tools gain stature with many investors? One reason is the 2008 financial crisis occurred just as a generation of investors both familiar and comfortable with technology, such as members of Generation X and millennials, came of age.

While they have a keen interest in their financial futures, they feel the establishment has dealt them a bad hand as both the government and the generations that preceded them have accumulated debt in “bailing out” banks and supporting society during the pandemic that they will have to pay back. Add to that the risks facing the environment as well as political divides throughout the globe and they feel their financial futures are in peril. When this generation looks at the past 10 years, they see passive investments with no or low fees equaling or exceeding the performance of more expensive active products. That leaves many feeling that active management isn’t worth paying for.

During this period, financial advisors haven’t done themselves any favors. Typically, they have focused on the question of suitability, or the understanding of a client’s risk appetite balanced with the limits set by key life events, such as saving for college or planning for retirement. This approach is outdated and easily replicated by robo-advisor platforms. This work is practically formulaic—which makes it the kind of task at which robo-advisers excel. Time to change the game!

Reinvigorating Relationships with Tech

Advisors can do better for themselves and their clients if they focus on doing things robots can’t. That means understanding that people make financial decisions in the context of their hopes, ambitions or disappointments. Understanding this can give advisors the chance to play an important role in the emotional lives of their clients, one which would make the advising relationship more fulfilling.

Working to foster this connection is important because events that affect one’s financial well-being dovetail with crucial life events. Marriages, divorces, children’s college funds and the decision to retire all hold the potential to create big changes that could upend a person’s status quo. They are also the most emotional and frequently lead people to call their financial advisor to get advice (and some hand-holding) from a trusted person who has their best interests at heart.

Once you have a client’s trust, they still expect value and results in return. That’s where embracing data analytics can help with delivering their best ideas and proactive, personalized plans for clients and prospects. There is no match for the data-enabled, next-gen advisor who can blend professional experience with the insights of data analysis to revitalize and improve client interactions. They must have a conversation with their client, one that is not yes/no, if/then, programmatic, rather they must act as a fiduciary advisor, a sort of wealth doctor, prescribing uniquely appropriate investments for their clients. To do this, they need data and information.

Data can tell advisors how assets perform over time, and about the risks if economists and forecasters are wrong. It reveals behavioral patterns that can aid in discussions about building portfolios to meet a client’s needs and how to hedge against unexpected risks. Client surveys and questionnaires help advisors conduct actual conversation—which assists clients more than answering text messages from a machine.

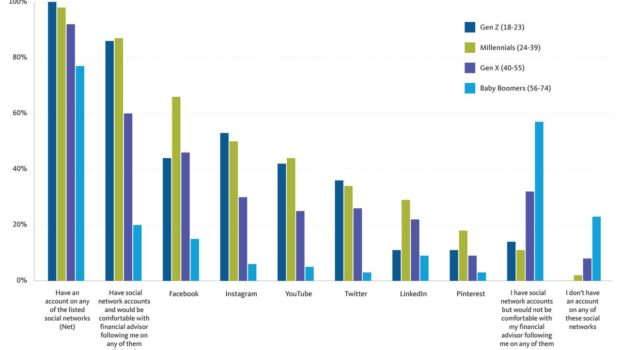

We also have some interesting stats from the new investor study around social media and FAs following clients. Over 60% of Gen X, Generation Z (87%) and millennials (87%) are comfortable having an advisor follow them on social media to offer a more customized experience.

Broadridge

Advisors should be attuned to how their clients want to communicate. A Broadridge survey showed 57% of investors said their communications with advisors had changed amid COVID-19, with people reporting varying preferences for phone calls, emails or video chats.

Successful advisors need the power of data, powerful analytics and speed of operations—so clients experience high-touch attention without all the manual manipulation that has historically been required. A robo-advisor doesn’t have an EQ and can’t tell if an investor is crying, smiling or overwhelmed. As people age and their earnings grow, there is a real need for personalized financial expertise. An advisor who has access to data and knows how to understand and present it can do better, because at its core technology is really most useful for leveraging human capabilities.

Advisors are asserting their relevancy in the middle of a crisis by embracing technology to better connect with and serve their clients. The combination of technology, understanding and empathy can deliver advice that individuals can grow with.

Improved efficiency that comes from embracing technology could help advisors grow their client base to include not just the wealthy but also new investors who may have more modest means. They too need help navigating complex financial decisions and may return to? this service now with loyalty over time should their wealth grow. These would be the best examples of how technology can help make the financial services business more human after all.

Gloss