RLX Technology: Regulatory Clarity Awaits

Vershinin/iStock via Getty Images

A Quick Take On RLX Technology

RLX Technology (RLX) went public in January 2021, raising $1.4 billion in gross proceeds in a U.S. IPO that was priced at $12.00 per ADS, above the expected range of $8.00-$10.00.

The firm produces closed-system e-vapor smoking devices for sale in China.

For 'risk-on' investors willing to hold RLX for an extended period, its bargain price may be too good to pass up. My outlook on RLX is a Buy at around $3.50 per ADS.

Note: RLX is a candidate for inclusion in my personal portfolio.

Company

Beijing, China-based RLX was founded to develop closed-system e-vapor smoking products, and according to management, is the number one seller in China, achieving a market share of 62.6% in retail sales for the nine months ended September 30, 2020.

Management is headed by Co-founder, Chairperson and CEO, Ms. Ying (Kate) Wang, who was previously head of Didi Youxiang and head of Uber China at Didi Chuxing.

The firm has developed an offline distribution and 'branded store plus' retail model that uses over 100 authorized distributors covering more than 250 cities in China.

In addition, the firm leverages its RELX Branded Partner Stores to provide further reach into a variety of retail stores such as electronics, convenience and e-vapor specialty stores.

The firm counts more than 100,000 retail store locations as carrying at least one of its products, helping the firm to attain a number one ranking in brand awareness, according to a study by CIC, which was commissioned and paid for by RLX.

RLX's Market & Competition

According to a 2018 market research report by ResearchAndMarkets, the Chinese market for e-cigarettes grew from an estimated RMB1 billion to RMB4 billion from 2013 to 2017.

According to the report, 'if 10% of 30 million to 35 million of Chinese smokers (out of up to an estimated 350 million total smokers in China) turn to electronic cigarettes, the potential market size will be above $15 billion.'

The main drivers for this expected growth are government initiatives to reduce smoking as well as younger demographic smokers who wish to transition to potentially less unhealthy forms of smoking and who prefer diversified tastes.

Also, the Chinese government has a complicated relationship with smoking, as it is in the business of selling traditional tobacco products to the population.

It prohibits the importation and online sale of heat-not-burn electronic cigarettes.

The company competes against traditional cigarette sellers, which include the Chinese government and other e-cigarette firms in a fragmented industry.

In 2019, the government banned the online advertising and sale of e-cigarettes, so the firm is subject to regulatory changes that may adversely impact its ability to operate.

RLX's Recent Financial Performance

-

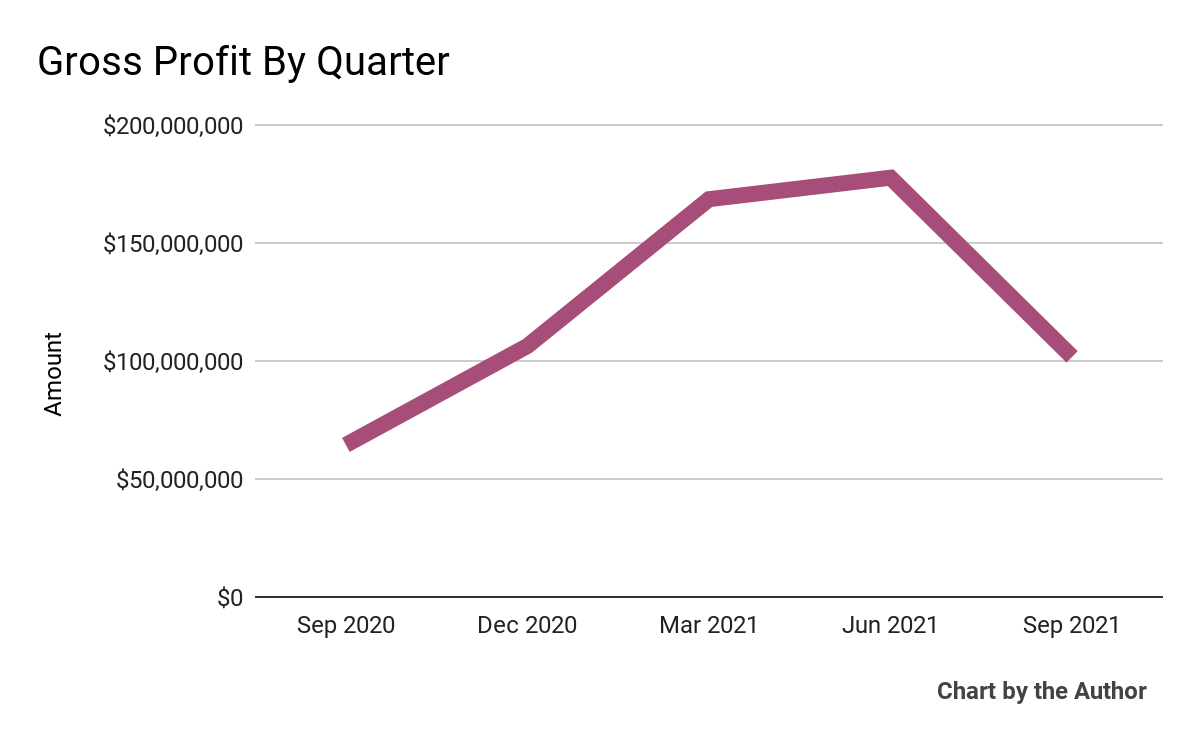

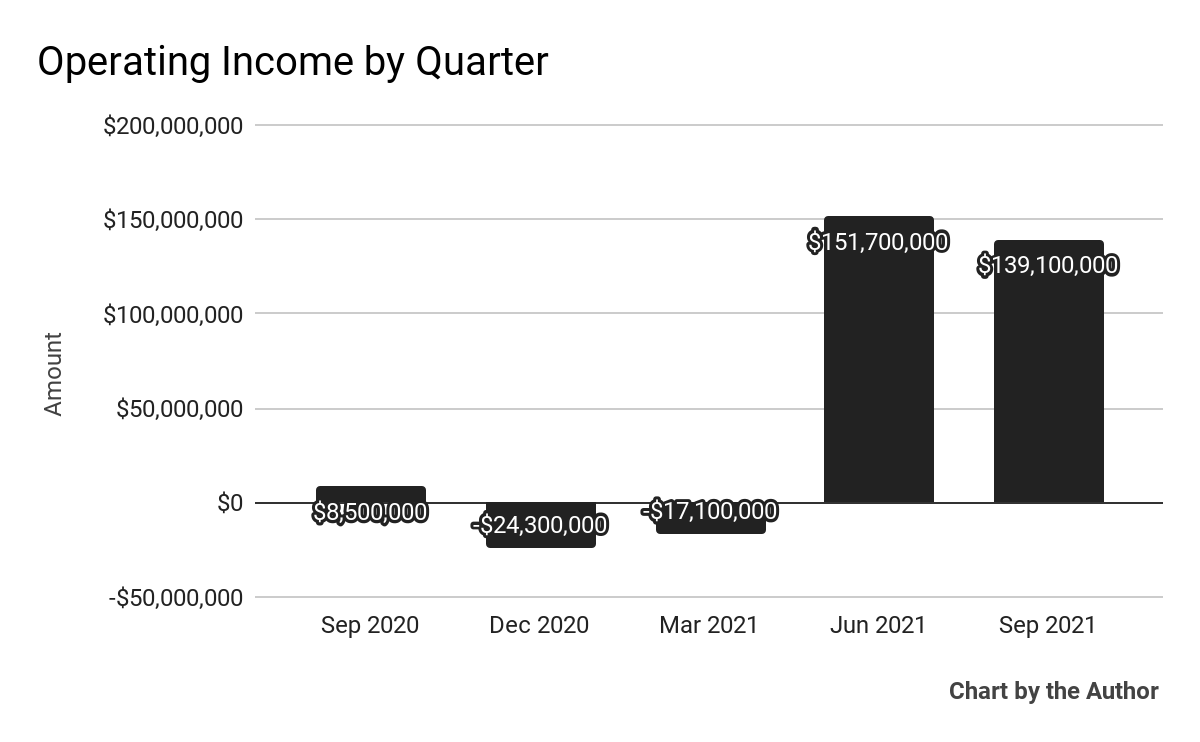

Topline revenue by quarter has grown markedly over the past 5 quarter period, with the exception of Q3 2021:

5-Quarter Total Revenue (Seeking Alpha and The Author)

5-Quarter Gross Profit (Seeking Alpha and The Author)

5-Quarter Operating Income (Seeking Alpha and The Author)

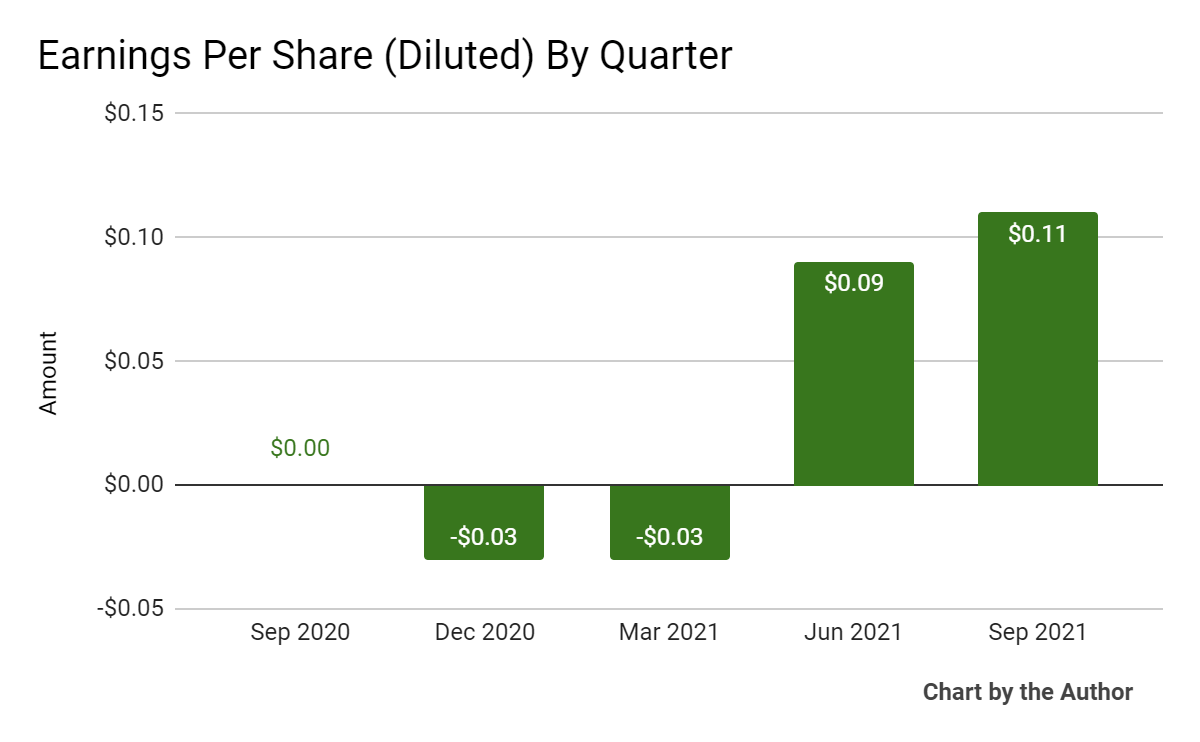

- Earnings per share (Diluted) have followed a roughly similar trajectory as operating income:

5-Quarter Earnings Per Share (Seeking Alpha and The Author)

(Source data for above GAAP financial charts)

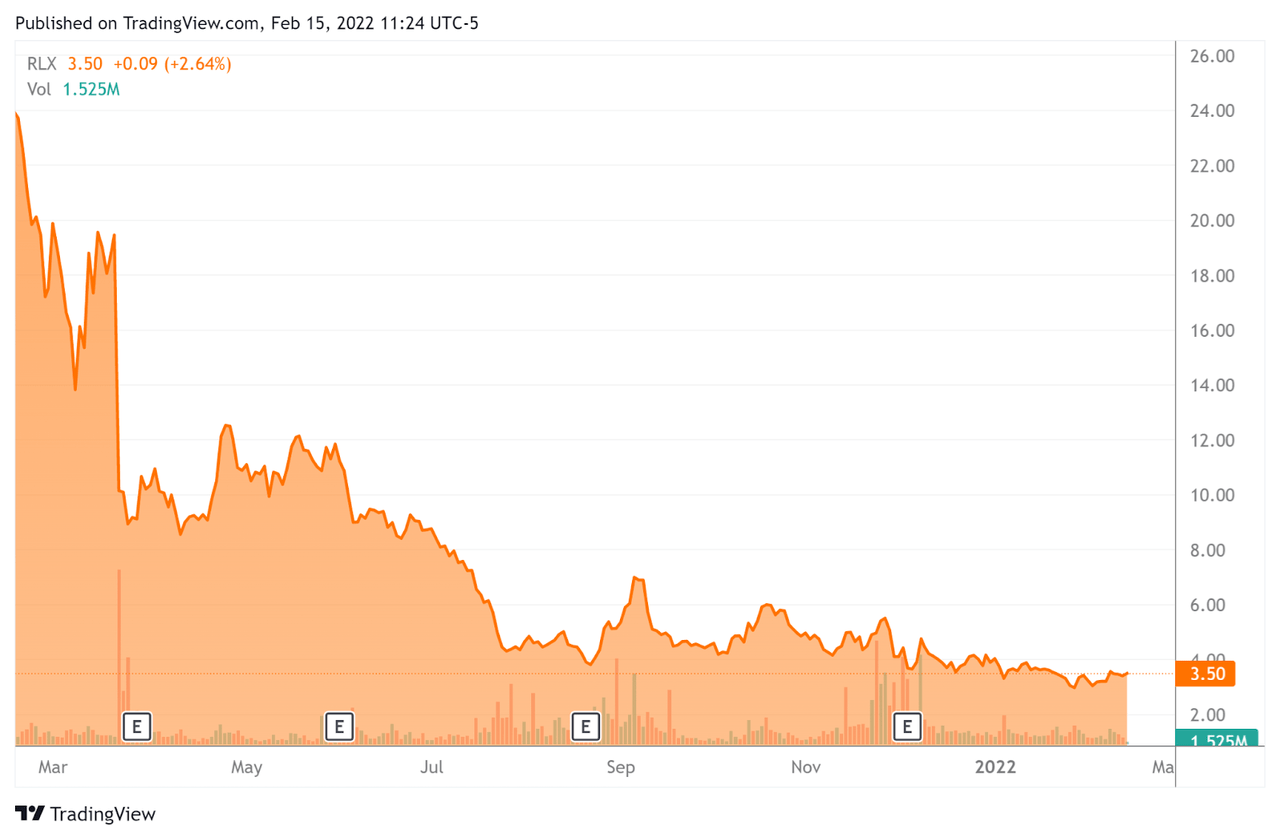

In the past 12 months, RLX's stock price has dropped 86 percent vs. the U.S. S&P 500 Index's rise of 11.9 percent, as the chart below indicates:

52-Week Stock Price (Seeking Alpha)

(Source)

Valuation Metrics For RLX

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure |

Amount |

|

Market Capitalization |

$4,670,000,000 |

|

Enterprise Value |

$2,840,000,000 |

|

Price/Sales |

3.87 |

|

Enterprise Value/Sales |

2.22 |

|

Enterprise Value/EBITDA |

11.23 |

|

Free Cash Flow (TTM) |

$207,700,000 |

|

Revenue Growth Rate (TTM) |

215.31% |

|

Earnings Per Share |

$0.14 |

(Source)

As a reference, a relevant public comparable would be Smoore International Holdings (OTCPK:SMORF); shown below is a comparison of their primary valuation metrics:

|

Metric |

Smoore International (OTCPK:SMORF) |

RLX Technology (RLX) |

Variance |

|

Price/Sales |

12.65 |

3.87 |

-69.4% |

|

Enterprise Value/Sales |

12.00 |

2.22 |

-81.5% |

|

Enterprise Value/EBITDA |

26.41 |

11.23 |

-57.5% |

|

Free Cash Flow (TTM) |

$314,180,000 |

$207,700,000 |

-33.9% |

|

Revenue Growth Rate |

59.2% |

215.3% |

263.6% |

(Source)

Commentary On RLX

In its last earnings call, covering Q3 2021's results, management highlighted that it believes that recent government regulatory communications 'will pave the way for long-term and sustainable growth in this sector.'

Founder and CEO Wang also mentioned its corporate social responsibility, with its focus on age verification efforts to prevent under-18 use of its products.

Also, the company launched a new brand targeting adult smokers with a long history of smoking. The product features 8 tobacco flavored cartridges aimed at this large segment.

As to its financial results, Q3 marked a significant drop in revenue due to negative publicity in China, teen restrictions by Walgreens and COVID-19-related outbreaks in China.

However, management views this revenue decline as temporary and continues to make strong efforts across its sales, supply chain and R&D categories.

The company spent the quarter focusing on its existing distribution chains with improvement suggestions or changes, rather than adding new distribution.

Looking ahead, management believes the electronic cigarette industry is now in the 'second half of the game' from a regulatory standpoint with greater regulatory clarity, enhanced product safety and quality, authentic social responsibility, and improved intellectual property protection.

Regarding valuation, compared to much larger Smoore International, RLX is trading at a large discount on various valuation metrics.

The primary risk to the company's outlook is the remaining uncertainty with regards to regulatory developments.

For example, new standards could reduce the maximum nicotine content down to 2%, which would reduce some user satisfaction aspects.

However, RLX presents a potentially interesting opportunity as a beaten-down stock that may be coming closer to the end of the road for regulatory uncertainty.

Preliminary Q4 results as described by management show 'sequential improvements in retail sale, and also channel inventory managements.'

For 'risk-on' investors willing to hold RLX for an extended period, its bargain price may be too good to pass up. My outlook on RLX is a Buy at around $3.50 per ADS.

Gloss