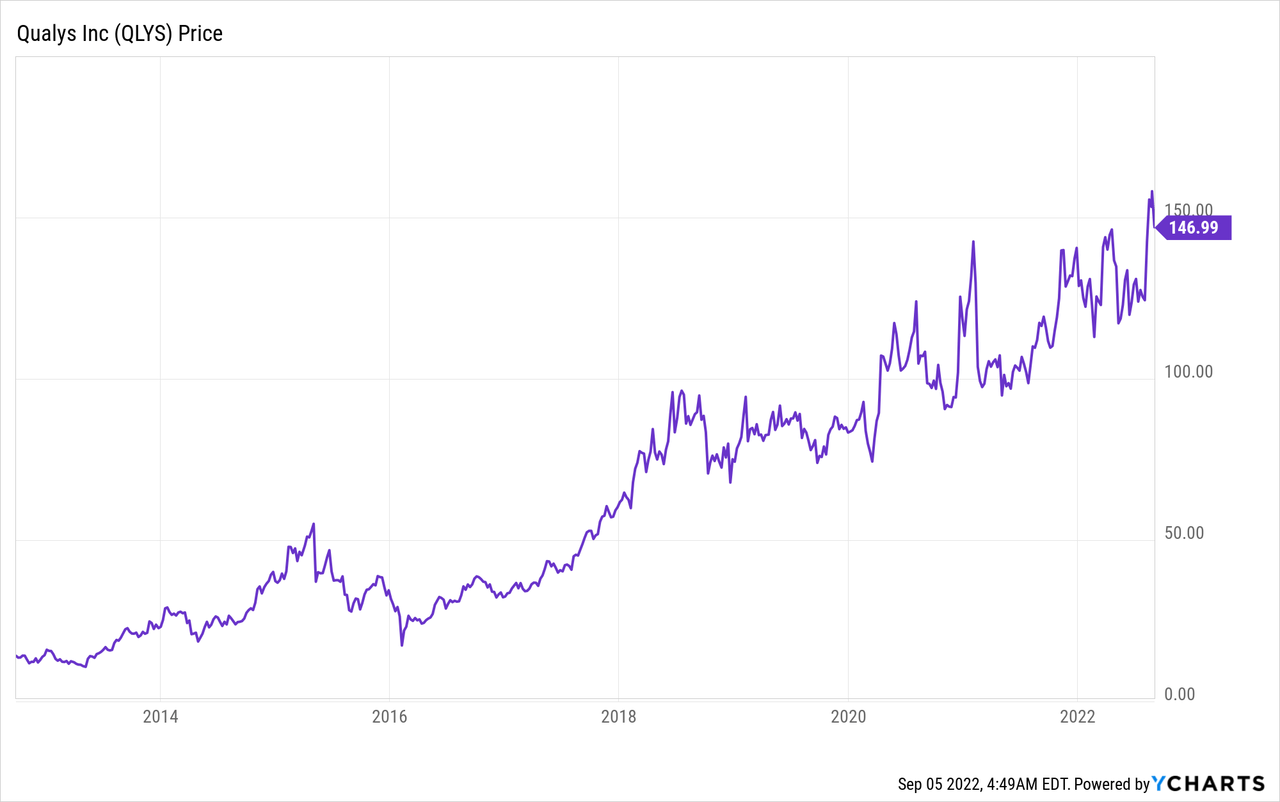

Qualys Stock: Sensationally Profitable CyberSecurity Stock (NASDAQ:QLYS)

https://www.ispeech.org/text.to.speech

Ignatiev/E+ via Getty Images

Qualys (NASDAQ:QLYS) is a leading cybersecurity platform that offers a cloud security and compliance solution. The company was founded in 1999 and had its IPO in 2012. Since then the stock price has increased by over 938% despite a rocky ride upward for investors. This is a testament to the strategy of holding quality stocks long term and benefiting from the growth in earnings. Qualys recently beat both revenue and earnings estimates for the second quarter and has a long growth runway ahead. In this post I'm going to break down the company's business model, its financials, and valuation, let's dive in.

Secure Business Model

Qualys is a leading cloud security and compliance platform. The company offers a cloud-native SaaS solution that enables enterprises to consolidate the use of multiple security vendors. For example, an enterprise may use SentinelOne for IT security, Tenable for Compliance, Invicti for Web app security, ServiceNow for asset management, and then Palo Alto networks for cloud/container security. Whereas Qualys covers all these products in one single solution, which lowers cost and reduces platform management overhead.

Single Platform (Qualys)

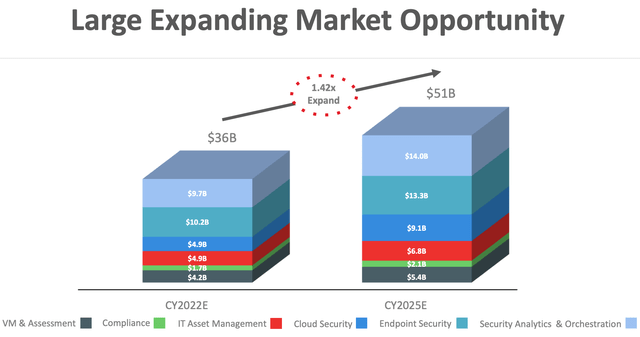

The Total addressable market across these different security segments is expected to expand by 1.42x by 2025 and reach a staggering $51 billion. Thus if Qualys could capture just 5% of this market that would be worth over $2.5 billion in revenue, which would be substantially higher than the $600 million in revenue generated today.

TAM (Gartner, Qualys data)

The digital transformation industry is forecasted to grow at over a 19% Compounded Annual Growth Rate up until 2026. Therefore many companies will require a new cloud-based security and compliance solution, which also works well with hybrid IT setups, Qualys is poised to fill this gap.

The company aims to accomplish this by producing a best-in-class product that includes over 20 integrated IT, Security, and compliance Apps. Its flagship Vulnerability Management Detection and Response [VMDR] platform enables users to manage cybersecurity risk, get pre-emptive alerts on potential attacks and even automate "remediation" which enables threats to be contained rapidly.

VMDR 1 (investor presentation)

Its VMDR platform has 4.4 out of 5 stars on Gartner reviews. Positive comments include "vulnerability scanning in the blink of an eye". But there are some negative comments about long wait times for technical support.

The company has already achieved strong traction for its product with it being adopted by 66% of the Forbes Global 50, 46% of the Global 500, and 25% of the Global 2000. Over 10,000 of these customers are on a subscription, which means predictable recurring revenue is standard. Its customers include big-name brands like Apple, Amazon, Alphabet/Google, Ford, McDonald's, Costco, Cisco, Microsoft, Netflix, Mastercard, Visa, and many more. The high-grade quality of its customer base is a key testament to the quality of its product.

Customers (Qualys Investor Presentation Q2)

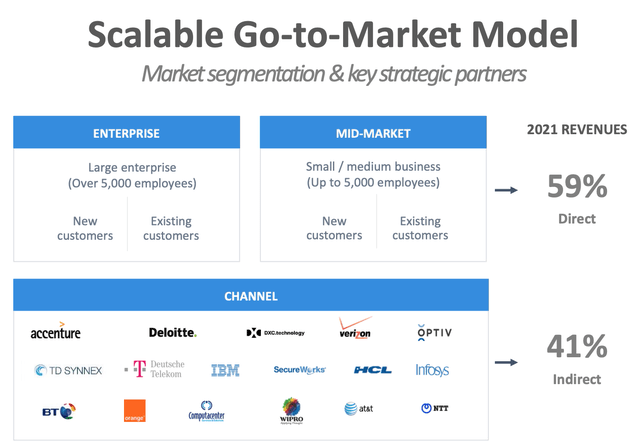

The company has grown its customer base through a two-pronged Go to Market strategy. This includes 59% of sales coming direct from Enterprises and mid-market businesses. In addition, to 41% of sales being generated through partnerships with leading consultancies such as Accenture, Deloitte, BT, Verizon, AT&T and many more. This is a brilliant strategy as many enterprises will reach out to a consultancy, when undergoing a digital transformation and thus Qualys is one step ahead.

Go to Market (Investor Presentation)

Qualys also runs a series of events such as its 10-city roadshow the Qualys Security Conference [QSC] which covers London, Chicago, New York and San Francisco.

Growing Financials

Qualys generated strong financials for the second quarter of 2022. Revenues were $119.9 million which increased by 20% year over year and beat analyst expectations by $2.36 million. With $233 million in year-to-date revenue as seen on the chart below. This is fantastic considering in the entire year of 2018 revenue was just $279 million.

Qualys Revenue (Q2 Earnings Report)

Its revenue was boosted by a strong number of larger customers with 139 enterprises now spending $500,000 or more with the company, which is up 23% over the past 4 years. Its Patch Management solution achieved blistering growth of 50% Y/Y and contributed towards 5% of bookings for the first time ever and 9% for new customers.

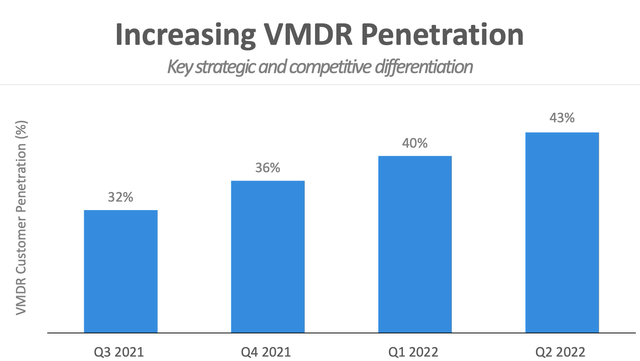

Qualys average deal size increased by 17% year over year, as customers used the platform to secure the Internet of Things (IoT) devices and applications across cloud, containers, and on-prem. Total VMDR customer penetration also expanded to 43%, up from 28% in the equivalent period last year.

VMDR Penetration (Q2 Earnings Report)

Qualys generated a solid gross profit of $94.8 million, which popped by 21% year over year. As a SaaS company, it has a super high Gross Margin of 79%, which ticked up 1% year over year.

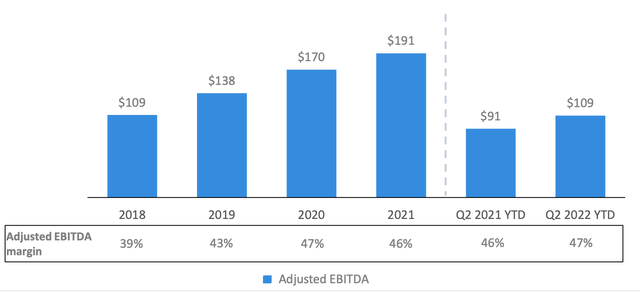

Earnings Per Share came in at $0.67 which beat analyst estimates by $0.20. Operating Income also expanded to $33 million, up 12% year over year. Adjusted EBITDA also popped by 16% year over year to $54.4 million, and a 45% margin. From the chart below you can see Adjusted EBITDA [year to date] was $109 million, which was the same as the entire year of 2018, which is great to see.

Adjusted EBITDA (Q2 Earnings Report)

Operating Cash flow did decline by 38% year over to year $33.8 million. The company invested $3.5 million into capital expenditures and bought back $71.2 million worth of shares, which is a positive sign.

Qualys has a fortress balance sheet with $419.1 million in cash and short-term investments, with just $42.9 million in debt.

Bullish Guidance

Moving forward management has raised its revenue guidance for the full year to be between $488 million and $489.5 million, which would be an increase of 19% year over year.

Management also raised its guidance on profitability with full-year earnings per share expected to be between $3.50 and $3.55.

Advanced Valuation

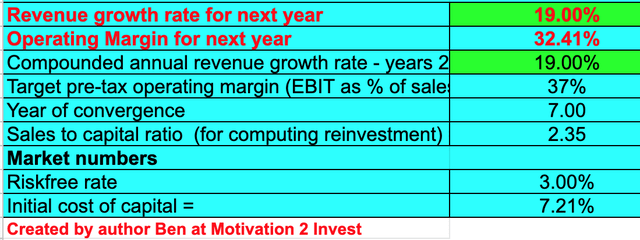

In order to value Qualys, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow method of valuation. I have forecasted 19% revenue growth per year over the next 5 years. This is based on industry growth rates and analyst estimates.

Qualys stock valuation 1 (created by author Ben at Motivation 2 Invest)

I have forecasted the company's operating margin to increase from ~32% to 37% over the next 7 years. As the company benefits from cross-sells and continues to grow its larger customer base. For additional accuracy I have capitalized the company's R&D expenses, this has caused the operating margin to adjust higher on my model.

Qualys stock valuation (created by author Ben at Motivation 2 Invest)

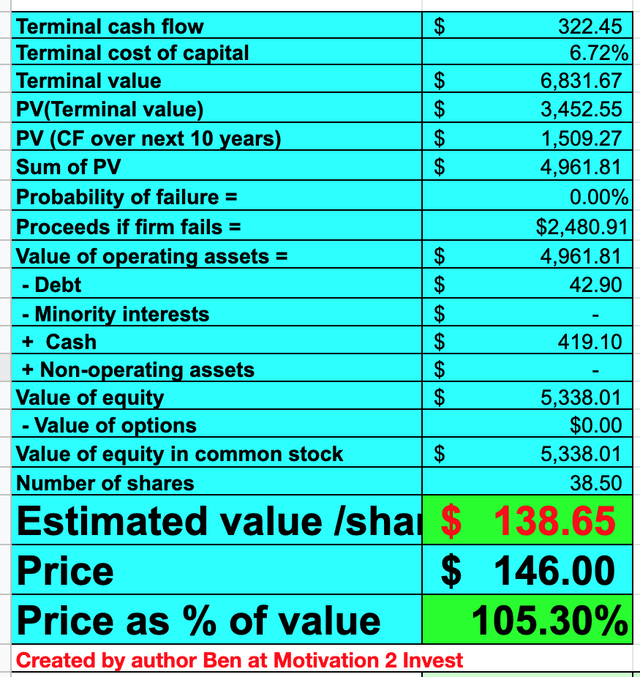

Given these financial inputs I get a fair value of $138/share, the stock is trading at $146/share at the time of writing and thus is slightly overvalued.

As an extra datapoint, Qualys is trading at a PE Ratio [forward] = 41.61 which is 5% cheaper than its 5-year average.

Risks

Competition

The cybersecurity industry has many competitors which include SentinelOne (S), CrowdStrike (CRWD), Palo Alto Networks (PANW), Okta (OKTA) and many more. I believe Qualys does have a solid offering in the enterprise space as it acts as a vendor consolidator which vastly simplifies the managing process for companies.

Recession

Many analysts are forecasting a recession and thus even if they are wrong the expectation of a recession could cause a temporary pullback in IT spending.

Final Thoughts

Qualys is a rare cybersecurity company as it is both growing rapidly and highly profitable. I believe the profitability of the company and the quality of customers means it deserves to trade at a premium to the market. Therefore I will label this stock as a "Buy". However, prudent investors may wish to set up buy alerts and wait for a pullback before entering. The stock price has been notoriously volatile and was trading at just $122 per share with strong support in July, thus that buy point could offer a greater margin of safety.

Gloss