CrowdStrike: Good Cybersecurity Play, But Overvalued (NASDAQ:CRWD)

solarseven/iStock via Getty Images

Investment Thesis

CrowdStrike (CRWD) belongs on the watchlist of growth investors, but I wouldn't be buying at current prices. The company is growing revenues at a rapid pace, but with interest rate hikes expected in 2022, I would wait to buy shares as the selloff could continue. The company has impressive revenue growth which hasn't made its way to the bottom line yet but should as the company grows towards maturity. Investors should keep an eye on ballooning operating and stock-based expenses. Bullish investors should be patient and wait for a price where the risk/reward is skewed to the upside.

The Business

CrowdStrike is a cloud cybersecurity company that is known as one of the current leaders in the industry. The company has plenty of cash on the balance sheet, and the people that I have talked to that are familiar with CrowdStrike's offerings have had good things to say about it. The company is investing aggressively back into the business but is not profitable despite explosive revenue growth. They are rapidly growing the customer base, especially among large Fortune 500 companies, and have consistently had a net retention rate over 120%.

ARR (CrowdStrike)

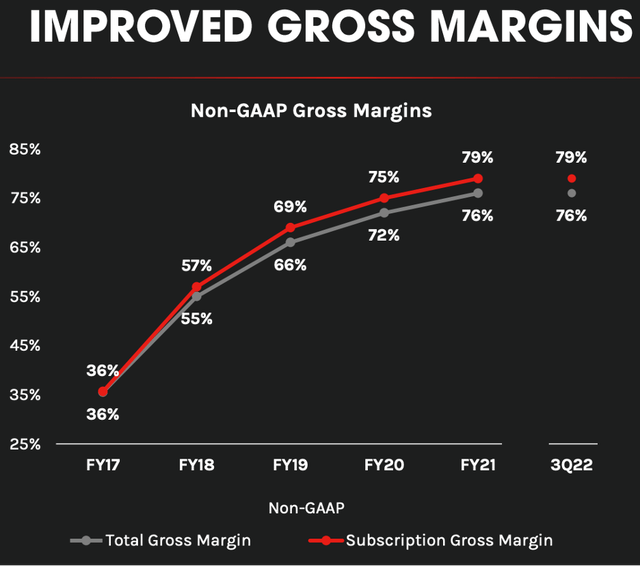

In my opinion, investors interested in the secular growth story should focus on two things primarily: revenue growth and gross margins. For the most recent quarter (the quarter ending 10/31/22), CrowdStrike grew subscription revenue from $213.5M in the prior year to $357M, a 67% increase. The company generates well over 90% of their revenues from subscription and a smaller amount from services. Their overall gross margin (GAAP) for the most recent quarter was just over 73%, which points to impressive margins at scale.

Gross Margins (CrowdStrike)

The problem is that CrowdStrike has also seen explosive growth in the operating expenses. This includes sales and marketing, R&D, and general and administrative expenses. Operating expenses grew from 195.1M to 318.7M, a 63% increase. One other thing investors should be aware of is that like many other young tech companies, CrowdStrike has a significant stock based compensation expense. The company spent $86.7M for the last quarter and $217.3M for the first nine months of the fiscal year. I like the business, despite the huge operating and stock-based compensation expenses, but the premium valuation is what is keeping me on the sidelines for now.

Valuation

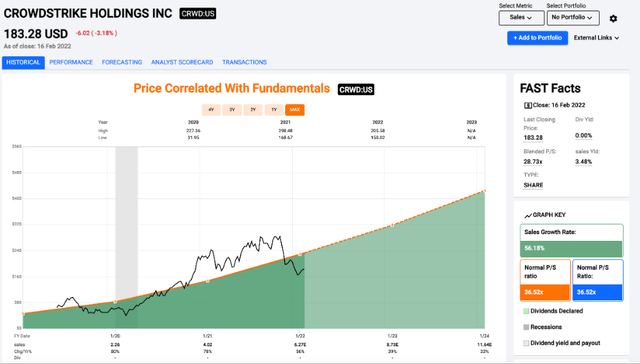

CrowdStrike isn't cheap, but the premium valuation makes sense when you consider the revenue growth. The valuation has started to come back to reality a little bit, but I'm still waiting on the sidelines just given the current market environment. I think it is highly likely that bullish investors will be able to pick up shares at a more attractive valuation in the coming months. I started a position in CrowdStrike in 2020, and I sold a couple months ago in December when it was just over $205, but I'm looking for a dip to the low $100 range before I start to get interested again.

I have a hard time using sales as a valuation metric, but it's the most logical option for a business like CrowdStrike. The valuation since going public has always been at nosebleed levels, with an average price to sales of 36.5x. The price to sales is a little below that mark and is currently trading at 27.1x (as of 2/17 close). It hurts the value investor in me to say this, but if we see CrowdStrike go to 15-20x sales at some point in the next couple months, I might pick up a couple shares.

Price/Sales (FAST Graphs)

A lot has changed with my strategy (and my positions) over the last couple years, but I was lucky enough to buy relatively early and come out ahead. I have been much more selective lately with the growth stocks I have been buying, but CrowdStrike is on my watchlist as a founder led business focused on cybersecurity. Some investors might look at the company on an adjusted basis by excluding stock-based compensation. I understand the logic behind it, but I have a hard time buying businesses that aren't profitable today.

Margins Target (CrowdStrike)

CrowdStrike certainly has the potential to be an asset light cash machine at scale, but investors should be ready for volatile swings in share price without any news. I think CrowdStrike is likely to report another solid quarter of revenue growth, but the problem is trying to decipher how much of that future growth is already priced into the shares.

Conclusion

CrowdStrike is a business that deserves a premium, and everyone from Wall Street to the retail investor knows it. Each investor has to decide how much of a valuation premium they are willing to pay, especially as interest rates are likely to increase in the coming months. The company has experienced explosive revenue growth and has all the metrics (like net retention rate for example) that software stock investors like to see. CrowdStrike is certainly on my watchlist, but that is where it will stay at the current valuation. If shares sell off into the low-100 range, I will turn bullish as CrowdStrike is likely to be a significant player in the cybersecurity space moving forward.

I would be fascinated to hear your thoughts. Feel free to leave a comment below.

Gloss