Aspen Technology: Overvalued Or Will This Winner Keep Winning? (NASDAQ:AZPN)

B4LLS

Most tech names of almost any size are still going through an agonizing bear market, but SAAS company Aspen Technology is hitting all-time highs. The company IPO'd amid the late 90’s tech boom, and naturally crashed with everything else. During the carnage of the dotcom bust, it was possible to buy shares in NASDAQ:AZPN that would today be worth 400x if you had timed the bottom perfectly.

The key question is whether this new all-time high means overvaluation or is this a winner that keeps on winning?

The Story

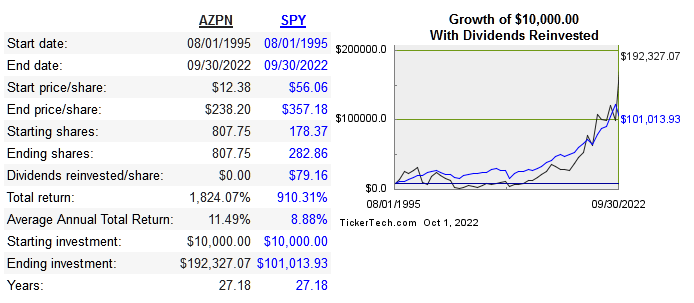

AZPN is one of the best SAAS growth stories over the past twenty years. Born out of an MIT lab about forty years ago, the company IPO’d in 1994 and has become a powerhouse in industrial software. Virtually all tangible industrial processes require intricate software to maintain operations safely and efficiently. The industry is estimated to grow around 7% CAGR until the end of the decade. AZPN has about 10% market share in the enterprise asset management software industry. Below is the long-term share price CAGR:

Dividend Channel

They’ve been profitable most years as a public company and averaged a 40% free cash flow margin in the past decade. Gross margins impressively grew as revenue has grown. This isn’t a story of top line growth with profitability a faraway goal in the future.

Below are the returns on capital metrics versus peers:

|

Company |

10-Year Median ROE |

10-Year Median ROIC |

EPS 10-Year CAGR |

FCF 10-Year CAGR |

|

AZPN |

53% |

42.5% |

45.5% |

16.3% |

|

ANSS |

11.7% |

11.7% |

10.4% |

6.3% |

|

SPSC |

2.1% |

2.1% |

8.4% |

44.6% |

|

BSY |

31.1% |

14.3% |

-9.3% |

7.3% |

Capital Allocation

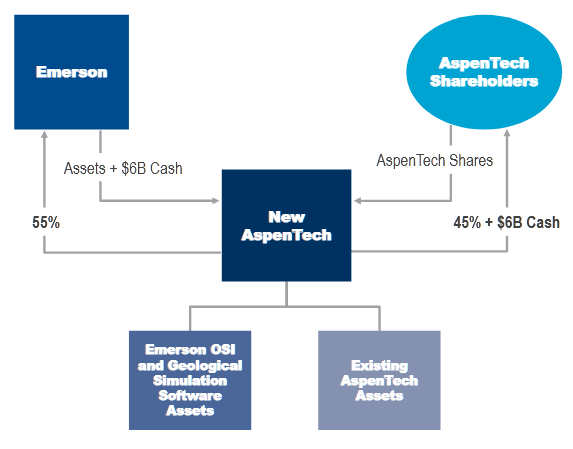

AZPN has an extremely impressive median FCF margin of 40%. They’ve made over 20 acquisitions, with the largest being the purchase of Micromine earlier this year for $640 million. The biggest M&A event so far has obviously been the merger with EMR’s software units. EMR has a 55% controlling stake, but the new entity kept the Aspen name and the current CEO, who started in 2013, will remain in place.

As far as returning capital to shareholders, no dividends have ever been paid, but in 2013, they began repurchasing shares and total share count has been reduced 56% since then. Total debt is at a very manageable $107 million and the current cash balance is $450 million.

Risk

The company clearly has a strong moat at the moment, but the biggest fundamental risk is competition driving down their margins and returns on capital or slowing growth. This risk is partially offset by currently being controlled by a large cap industrial company. They can synergize and bring new business and help with funding of bigger investments and acquisitions. This is noted in a figure showing the transaction structure from the presentation on this merger:

investor presentation document

Fundamental risk at the company level is low, so the real risk for you as a potential investor will come from paying too much for the growth as opposed to being wrong about the growth and quality. This leads us right to valuation.

Valuation

Below is a comparison of price multiples:

|

Company |

EV/Sales |

EV/EBITDA |

EV/FCF |

P/B |

|

AZPN |

20.8 |

47.2 |

56.2 |

18.7 |

|

ANSS |

10.2 |

30.7 |

36.1 |

4.5 |

|

SPSC |

10.4 |

50 |

56.9 |

9.2 |

|

BSY |

10.1 |

57.1 |

37 |

18.1 |

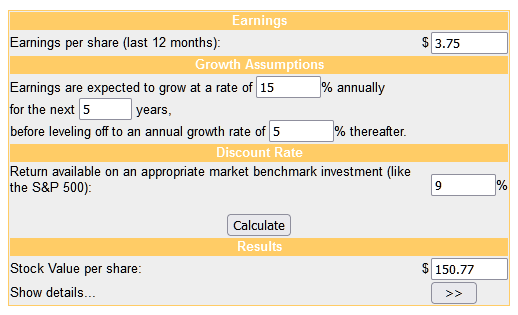

On a relative basis things are looking expensive but remember that the quality of this company is obvious at this point, so some sort of premium will be reflected. Next is the DCF model:

Moneychimp

I’m bullish on the fundamentals of the company and the fact that shares have been hitting all-time highs is a good sign. The current price is just too high for me at this stage. On one hand I firmly believe in the concept of using the quality of the business as your margin of safety, on the other hand you can’t ignore valuation and bet entirely on getting the growth and quality right long term.

Conclusion

I am absolutely not an advocate of ignoring valuation and buying the best growth companies no matter the price. My ideal situation is to find a great growth company that trades at a modest discount. I also have to be honest with reality, most of the best returning growth companies will always have a premium multiple attached. This is especially true for capital-light business models like SAAS. The winners will be worth the premium if you hold on for the long run, but the number of investors who actually held onto MSFT, for example, during its lost decade and never sold is small.

Once it's clear to the world that you have a great growth story that is extremely profitable, the quality will always be baked into the price to some extent. Shares can of course drop a bit when guidance is missed, but a quality growth company will never see huge drawdowns outside of an overall market crash or extreme short-term turmoil/controversy.

With AZPN, you have a high growth company with incredible profitability and good potential for top line growth and EPS growth accelerated via repurchases. Right now the price is too high for me on a relative basis and intrinsically as well. This stock will never trade in the single-digit PEs or anything close to it. You will have to pay up for the quality, but this price is still too high today.

Gloss