AMD Vs. Marvell Technology Stock: Which Is The Better Buy?

MF3d

It has been a turbulent year for the stock market, and worse for the semiconductor sector. In the first half of the year, which saw the worst market rout in decades, the semiconductor sector led market losses, with the Philadelphia Semiconductor index down by almost 40%. Yet, the cohort led a strong rebound entering July, after key manufacturers of chips used in everything from smartphones to cars cited strong demand still, paired with easing global supply chain constraints. Positive developments regarding the proposed CHIPS Act, which includes funding of more than $50 billion towards bolstering the U.S.’ chip industry, has also improved investors’ sentiment for the sector in recent weeks.

The Philadelphia Semiconductor Index climbed close to 15% in the first three weeks of July, but pared gains on Friday’s session, suggesting that sentiment on the sector’s near-term outlook remains fragile. Investors’ concerns remain over chipmakers’ near-term performance amid waning consumer sentiment while recession risks grow. Some chipmakers have cut costs, dialed back on investment plans, and even slashed growth forecasts this year as pre-emptive measures against broader macroeconomic uncertainties ahead. Both AMD (NASDAQ:AMD) and Marvell Technology (NASDAQ:MRVL) fell as much as 4% and 6%, respectively, Friday (July 22) after Seagate Technology (STX) – core manufacturer of computer hard drives – reported signs of heightened demand slowdown for consumer electronics ahead of “weakening global economic conditions” over the next two quarters.

However, both AMD and Marvell have continued to demonstrate robust fundamental growth this year, and the trend is expected to continue as data center demand – the two chipmakers’ core end markets – remains resilient against looming recession risks. While both AMD and Marvell cater to the same core end markets (e.g. data center, consumers, automotive, telco infrastructure, etc.), they play structurally different roles by offering complementary technologies. Both companies have also been actively participating in strategic acquisitions over the past year to bolster their respective offerings and further expand their respective addressable markets, underscoring a massive growth trajectory ahead.

While we believe both stocks make a favourable long-term investment at current levels, the question over which makes a better pick will ultimately depend on an investor's risk appetite.

In our view, AMD makes a safer investment considering its market leadership in the provision of server CPUs, as well as its strong balance sheet and robust profit and free cash flow margins, which are still expanding with continued scale. Meanwhile, Marvell is still some ways from profitability, despite being cash flow positive from an operational standpoint, while also working towards deleveraging its balance sheet. Under the current market climate where investors’ sentiment remains fragile with persistent aversion towards risky assets ahead of a potential downturn, Marvell’s weaker fundamentals leave it with less cushion for impact from looming headwinds, and could potentially expose its shares to greater risks of volatility when compared to AMD.

But with both AMD and Marvell’s offerings being a critical backbone to key technologies spanning consumer electronics (e.g. smartphones, computers), connected vehicles, cloud computing, AI/ML, and 5G networks, both companies are uniquely positioned for a sustained long-term growth trajectory, underpinning promising upside potential from a valuation perspective.

How are AMD and Marvell Technology Different?

Both AMD and Marvell offer standard and semi-custom semiconductor technologies designed for data center, automotive, network carrier, and consumer electronics applications. But while both AMD and Marvell cater to the same end markets, they both play a different role.

AMD

AMD is a market leader in the provision of processors used in everything from gaming laptops to supercomputers, and has recently extended its foray into field programmable gate arrays (“FPGA”) and system-on-chips (“SoC”) via the acquisition of Xilinx, as well as software and data processing units (“DPUs”) via the acquisition of Pensando:

- Server processors: AMD’s EPYC server processors have been a flagship product in leading the company’s break-out growth and data center market share gains in recent years. The EPYC CPUs are now onto their fourth generation, featuring a family of four chips spanning “Genoa”, “Genoa-X”, “Bergamo”, and “Siena”, all of which are tailored to optimize performance across different use cases ranging from cloud-computing to communications infrastructure and telco deployments. The powerful server processors have evolved into one of the fastest and most powerful chips used in high-performance computing (“HPC”) architectures today. AMD’s EPYC processors are also now found in 73 of the world’s “Top 500 Fastest Supercomputers” list, a three-fold increase from 2020. The EPYC processors’ dominant presence on the “Green500” list, the top 500 fastest supercomputers ranked in terms of energy efficiency, is also a testament to its power efficiency for complex workloads. To date, eight of the world’s top 10 most efficient computers are also powered by AMD’s EPYC processors, putting the company’s HPC competency on par with legacy rival Intel’s (INTC). Looking further ahead will be AMD’s planned debut for its 5th Gen EPYC processor in 2024, codenamed “Turin”, which will continue to cover general to cloud-optimized applications. The 5th Gen EPYC processors are expected to feature the 4nm and 3nm manufacturing processes to unlock new performance capabilities (for those who are less familiar with the intricacies of chip technology like me, smaller nanometer processors are more powerful because it means the space between the high volume of transistors within a single chip is greatly reduced, thus lowering the “distance travelled by electrons to perform work” and reducing energy consumption while enabling faster computing). AMD has also expanded its foray in data center GPUs in recent years, with new and improved technology like the CDNA 2 Architecture bolstering its market share gains within a realm it has historically played a smaller role in.

- Gaming CPUs and GPUs: AMD also benefits from its strengths in PC and semi-custom chips, underpinned by growing momentum in gaming and other verticals like autonomous driving developments. AMD’s Ryzen and Radeon series represent its standard computing and graphics processor offerings used in powering desktop/notebooks. The company also provides semi-custom solutions, primarily via collaborations with OEMs like Microsoft (MSFT) and Sony (SONY) to co-develop tailored solutions for gaming consoles like the Xbox and PlayStation.

- Xilinx: AMD’s acquisition of Xilinx marks one of the largest transactions of its kind within the industry in recent years. Xilinx is currently a leader in the development of FPGAs and SoCs for application across a variety of technologies ranging from aerospace and automotive to cloud and communications infrastructure. Specifically, Xilinx is currently the ”leading provider of solutions in 5G” and boasts a strong pipeline of communications accounts. This accordingly complements AMD’s growing prominence within the network infrastructure sector, underscored by its recent win from Nokia to power the latter’s 5G network servers with EPYC processors. And on the data center front, Xilinx also leads fast-growing business in programmable solutions for data centers, which is poised to complement AMD’s current leadership in CPU and GPU processors for data center application as discussed in earlier sections. The XDNA Architecture is the newest addition to AMD’s family of offerings. Built on the “foundational architecture IP from Xilinx”, the XDNA Architecture “consists of key technologies including the FPGA fabric and AI engine (“AIE”) – core areas of Xilinx’s expertise – to enable optimized performance and energy efficiency for application in complex workloads such as AI and signal processing. The AMD XDNA IP is scheduled for debut in 2023, beginning with the integration into the AMD Ryzen series processors used primarily in powering desktop/notebooks.

- Pensando: AMD’s recent acquisition of Pensando also builds on its strategy to grow market share by expanding its product portfolio, and inadvertently its total addressable market (“TAM”). With customers including high-profile names like Goldman Sachs (GS), Microsoft’s Azure, HPE (HPE), and Oracle’s cloud unit (ORCL), Pensando boasts its strength in “high-performance, fully programmable [data] packet processors and [a] comprehensive software stack that accelerates networking, security, storage and other services for cloud, enterprise and edge applications”. Pensando’s DPU line-up is also complemented by a “robust software stack with zero trust security throughout”. Paired with Xilinx’s hardware-software technology offerings for cloud and telco applications, and AMD’s existing hardware engines, the recent acquisition of Pensando accelerates the chipmaker’s collective efforts in creating full-stack, hardware-software solutions aimed at “[unifying its] overall product roadmap going forward”.

Marvell Technology

Meanwhile, Marvell specializes in the provision of infrastructure-specific semiconductor solutions, spanning electro-optical products used in facilitating data transmission, ethernet solutions used in channeling and routing data between networks, and processors:

- Custom application-specific integrated circuits (“Custom ASICs”): Similar to AMD, Marvell also offers both standard and custom/semi-custom solutions for its end markets. Specifically, Marvell leverages its expertise in infrastructure-specific semiconductor solutions and offers related products tailored to customers’ specifications for application across “next-generation carrier, networking, data center, machine learning, automotive, aerospace, and defense” use cases.

- Electro-optics: Marvell’s electro-optics products are specifically designed to enable low-power and low-latency data transmission in cloud data centers and carrier networks. Related products include “pulse amplitude modulation (“PAM”) and coherent digital signal processors (“DSPs”), laser drivers, trans-impedance amplifiers (“TIAs”), silicon photonics, and data center interconnect (“DSI”) solutions”. These are primarily applied in critical infrastructure equipment that “process, store and transport data traffic” from day-to-day routers to interconnecting servers. The company’s recent acquisition of Inphi has played a critical role in bolstering its electro-optics offerings. Inphi is an industry leader in “electro-optics interconnect platforms” specialized for application in cloud data centers and carrier networks, which complements Marvell’s existing expertise in the arena. The acquisition also comes at an opportune time, as 5G investments continue to accelerate due to demand for faster connectivity speeds and competitive economics required to support increasingly complex computing workloads in the data-driven era, as well as nascent technologies like the metaverse.

- Ethernet solutions: Marvell is one of the industry leading providers of ethernet switch semiconductor solutions used in facilitating the routing of data between networks, specifically within the enterprise and telco segments. Recognizing the growing momentum in cloud-computing, Marvell has recently acquired Innovium to bolster its ethernet switch silicon offerings for data center application. Innovium is currently a leading provider of “cloud-optimized switches”, leveraging its proprietary “TERALYNX” switching architecture to deliver “ultra-low latency, optimized power, high performance, and innovative telemetry that are critical in today’s cloud-scale data centers”. Consolidated technology from Innovium will also leverage Marvell’s 5nm manufacturing process, which enables competitive performance and accommodates the computing power of next-generation server processors like those offered by AMD as mentioned above.

- Fibre channel adapters: Fibre channel silicon are primarily used to facilitate the transmission of data “among data centers, computer servers, switches and storage”. And low-power and low-latency are two of the core performance requirements within today’s demanding data center needs, driven by increasingly complex computing workloads, as well as the accelerating migration towards “borderless” work environments in the post-pandemic era. Marvell’s proprietary “QLogic Fibre Channel” is specifically designed to optimize these two requirements and enhance productivity. QLogic Fibre Channel offers best-in-class data transmission speeds and simplified deployment within enterprise and data center applications. This means faster connectivity and data processing speeds when logging into enterprise servers while working remotely.

- Networking infrastructure processors: Marvell’s networking infrastructure processors spans four major offerings: “OCTEON multi-core infrastructure processors”, “OCTEON Fusion-M processors”, “NITROX security processors”, and “LiquidIO Server Adapters”. The OCTEON DPUs are tailored for application across “networking, security and wireless infrastructure equipment, including switches, routers, secure gateways, firewall, network monitoring, 5G base stations, and smart network interface controllers (“SmartNICs”)”. NITROX security processors are used in enterprise and cloud data center infrastructure equipment and enable delivery of industry-leading cryptographic operations. LiquidIO are programmable SmartNICs that can “enable data centers to move user-specific workloads onto highly optimized offload engines for much greater speed and efficiency, at a lower total cost of ownership”. The LiquidIO SmartNIC solutions essentially allow data center operators to deploy scalable performance by enabling efficient and flexible programmability to accommodate the fast-changing nature of modern-day technology requirements. All of Marvell’s networking infrastructure processors are accompanied by comprehensive software development kits (“SDKs”) to enable seamless and scalable end-to-end solutions to customers.

- Storage controllers: Marvell currently offers hard disk drive (“HDD”) controllers, as well as solid state drive (“SSD”) controllers. The HDD controllers are essentially an SoC that controls and manages the hard disk storage, while SSD controllers are the equivalent for solid state drives that are increasingly replacing HDDs due to their improved speed and performance. With the transition from HDDs to SSDs in PC application well underway, Marvell’s HDD controllers currently account for only a nominal amount of its consolidated sales mix. Meanwhile, the company continues to bolster the performance of its SSD controllers, which features proprietary “NANDEdge programmable error correction coding IP” for application in next-generation NAND flash technology. The NANDEdge-equipped SSD controllers are designed to be power efficient, thus lowering total ownership costs, without compromising on performance, making it a scalable and efficient option for application across “client, edge, enterprise, and cloud data center markets”.

- Brightlane Solutions: Brightlane Solutions represent Marvell’s portfolio of offerings for the automotive sector, spanning “Ethernet PHY transceivers, bridges and switches supporting speeds from 100Mbps to 10Gbps with enhanced safety and security features required for in-vehicle networks”.

- Acquisition of Tanzanite: In addition to Marvell’s acquisition of Inphi and Innovium last year, which was discussed in earlier sections, the company has also recently entered into an agreement to acquire Tanzanite Silicon Solutions, an industry-leading developer of advanced “Compute Express Link” (“CXL”) technologies. The consolidation of CXL solutions via the Tanzanite acquisition is expected to complement Marvell’s comprehensive portfolio of infrastructure-specific semiconductor solutions for data center application. CXL is essentially the next generation of existing peripheral component interconnect express (“PCIe”) interface chips used for “connecting processors, accelerators and memory” and enabling the transfer and processing of data within a computing device. CXL will be critical in next-generation cloud data centers, considering the increasing demand for “memory performance and composability in the cloud” to facilitate next-generation technologies spanning complex AI/ML workloads, data analytics, and immersive experiences / metaverse.

Key Driving Opportunities

Both AMD and Marvell are well-positioned to take advantage of the burgeoning market opportunities stemming from burgeoning data center, enterprise, automotive, and carrier network demand in coming years. And both have been diligently engaged in strategic complementary acquisitions in recent years to expand their respective addressable markets, and maximize returns from end markets that they already have a leading presence in. Both companies’ technology stack reinforces the outlook for sustained long-term growth trajectory over coming years, underpinning promising valuation prospects ahead.

1. Data Center / Enterprise Network

Data center and enterprise network end markets are core drivers of AMD and Marvell’s growth in coming years. With only 11% of the corporate landscape feeling confident that their legacy business models will be "economically viable through 2023" and another 64% raising the need to step up on digitization plans, corporate spending on digital transformation is expected to remain resilient despite a looming economic downturn. More than half of corporations are expecting cloud adoption to account for a significant portion of investments in the next two years, driving the global cloud-computing market towards a projected value of more than $800 billion by 2025. Meanwhile, the market for supporting AI hardware, such as data center processors, is expected to expand at a CAGR of 43% towards $1.7 trillion by the end of the decade. These statistics continue to corroborate a robust demand environment for both cloud service providers and supporting chipmakers like AMD and Marvell.

Specifically, demand for ethernet switch silicon from the data center market is expected to advance at a five-year CAGR of 15% towards a $2 billion opportunity, making favourable trends for Marvell, which recently acquired Innovium to extend its foray in this area. For AMD, its recent acquisition of Xilinx puts the company in a unique position for TAM expansion as well by enabling new technologies such as the XDNA Architecture as discussed above – the global FPGA market is forecasted to grow at a CAGR of 8.5% through 2025, as rising adoption of emerging technologies continues to bolster demand.

2. 5G

Data consumption rates are expected to surge at a CAGR of 26.9% through to 2025, buoying global demand for 5G-enabled devices, which is expected to grow at a CAGR of 38% over the same period as users continue to transition to the new and faster network. This has accordingly accelerated 5G investments in recent years, driving significant demand for related semiconductor solutions offered by both Marvell and AMD. The market for 5G-specific solutions is expected to advance rapidly at a five-year CAGR of 28.5% towards a $10 billion opportunity, which underscores a massive growth trajectory ahead stemming from just the carrier network end market for both chipmakers.

3. Auto

While auto semiconductor sales have slowed this year due to amplified supply constraints, demand from the automotive end market remains robust. This makes strong tailwinds for Marvell’s Brightlane Solutions, as well as AMD’s improved auto offerings via Xilinx.

The automotive sector has not seen any material signs of demand destruction despite surging MSRP prices and looming recession risks. While general semiconductor demand within the automotive sector is expected to gradually expand at a CAGR of more than 12% towards a $94 billion market opportunity by 2028, much of the related growth will be driven by the sector’s accelerating transition to electric, connected and autonomous mobility. Specifically, AI processor demand arising from the autonomous vehicle end market are expected to expand at a five-year CAGR of 36% into a $60 billion opportunity by mid-decade.

4. Consumer

Global PC shipments have shown accelerating declines in the first half of the year - first quarter volumes dropped by 6.8% compared to the prior year to 78 million units, while second quarter volumes dropped by more than 15% to 71 million units, as consumer discretionary spending power weakens due to rising inflationary pressures. Global PC shipments are on track towards a 9.5% decline this year, led by an estimated 13.1% drop in consumer PCs and 7.2% drop in enterprise PCs.

Despite signs of a slowing PC market as consumers cut back on discretionary spending due to near-term economic uncertainties, both AMD and Marvell’s growth in this segment are expected to remain resilient. This is because both AMD and Marvell’s direct exposure to consumer spending is limited.

At AMD, the company sees the current PC market shifting to “higher end [and] more premium segments”, buoyed by corporate purchases to accommodate the idea that “hybrid and remote work is the new reality”. Digital transformation trends have enabled many corporate environments to adopt a “location-agnostic” work arrangement, giving employees full autonomy on deciding where they want to work. Although AMD has opted to stay on the conservative side with regards to PC opportunities for the current year, guiding a year-on-year decrease in “negative high single digits” for related sales, the company is expected to recoup some market share by selling its premium, more expensive models. AMD also has a “number of commercial systems” in the pipeline this year, including the recent launch of the “Ryzen 6000 Series” processors for premium laptop application, which underpins solid PC performance for 2022 despite a broad slowdown in the market.

As for Marvell, its consumer end market represents only a nominal portion of its consolidated performance. The continued ramp-up of Marvell’s SSD controller shipments used primarily in enterprise and cloud data center market applications is also replacing legacy HDD controllers for PC application, which provides insulation from current consumer headwinds. Marvell’s reduced exposure in consumer end markets is also corroborated by its limited notebook HDD controller sales during the April quarter, which represented less than 1% of its consolidated revenues.

Financial and Valuation Prospects

Both AMD and Marvell are expected to post robust double-digit growth over the next three years, buoyed by increasing demand across their core end markets (i.e. data center, carrier network, enterprise networking, and auto), as well as their diligent expansion of addressable markets through the acquisition and integration of complementary semiconductor technologies.

AMD

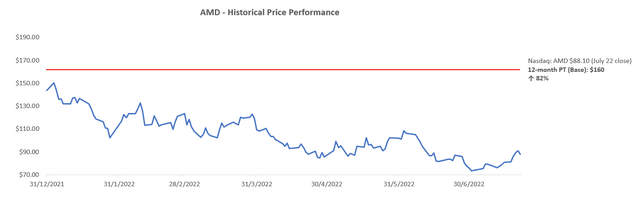

At AMD, we are maintaining our near-term base case price target at $160, which represents upside potential of more than 80% based on its shares’ last traded price of $88.10 apiece (July 22). The PT is derived by equally weighing results from the discounted cash flow (“DCF”) and multiple-based valuation analysis.

AMD Valuation Analysis (Author)

AMD Valuation Analysis (Author)

For the DCF analysis, we have applied an exit multiple of 25x and WACC of 12.2%, which bumps AMD’s valuation back in line with peers that exhibit a similar long-term high-growth profile. The company is currently trading at a discount to peers despite boasting leading growth prospects, alongside a technological advantage as well as a strong balance sheet. As such, we believe a slight premium multiple is reasonable given AMD’s rising exposure to high-demand segments.

AMD DCF Analysis (Author)

For the multiple-based analysis, we have applied a forward EV/sales multiple of 9.5x, which is derived with the same intention as our DCF analysis to gauge the company’s valuation prospects if traded more in line with peers in the immediate- to near-term (high-growth mean 5.9x).

AMD EV/Sales Valuation Analysis (Author)

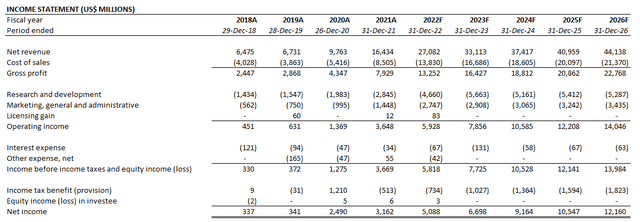

AMD Financial Forecast (Author)

AMD_-_Forecasted_Financial_Information.pdf

Marvell Technology

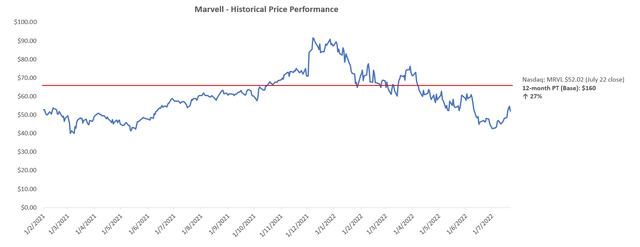

At Marvell, we have set a near-term PT of $66, which represents upside potential of close to 30% based on its shares’ last traded share price of $52.02 apiece (July 22). The PT is derived using the same valuation method above.

Marvell Technology Valuation Analysis (Author)

Marvell Technology Valuation Analysis (Author)

We equally weighed the results of a DCF analysis where an exit multiple of 21x and WACC of 12.4% is applied, and a multiple-based analysis where a forward EV/sales multiple of 9.6x is applied, in order to reflect Marvell’s near- and longer-term high-growth nature, offset by a smaller addressable market value compared to AMD’s and relatively weaker balance sheet.

Marvell Technology DCF Analysis (Author)

Marvell Technology EV/Sales Valuation Analysis (Author)

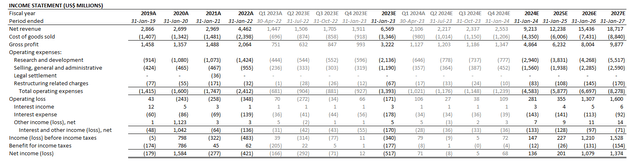

Marvell Technology Financial Forecast (Author)

Is AMD or MRVL Stock a Better Buy?

Both AMD and Marvell are expected to benefit from a robust demand environment buoyed by favourable secular tailwinds. Despite rising investors’ concerns of slowing semiconductor cycle following a multi-year boom, and added impact from softening consumer demand, AMD and Marvell’s near- and long-term fundamental prospects are expected to remain resilient. Global digital transformation trends are boding favourably for both AMD and Marvell’s fundamental performance, and inadvertently, its market share and valuation prospects.

As mentioned in earlier parts of the analysis, whether AMD or Marvell is the better pick would ultimately depend on investors’ risk appetite. Both companies exhibit high growth potential in coming years. However, AMD boasts a stronger balance sheet in net cash position, larger addressable market, and proven leadership in server CPUs, making it a comparatively safer trade in times of high volatility. Meanwhile, the latter remains in a net debt position within a capital-intensive business and is currently non-profitable despite being operationally cash positive. But from a long-term investment perspective, we believe the market has created an attractive entry opportunity for exposure in both chipmakers at current levels.

Gloss