Akamai Stock: Long Term Technology Value Opportunity (NASDAQ:AKAM)

https://www.ispeech.org/text.to.speech

Sundry Photography/iStock Editorial via Getty Images

Like many other technology stocks of late, Akamai Technologies (NASDAQ:AKAM) has made a full round trip back to its pre-pandemic level. However, unlike many of the other technology stocks to see huge drawdowns, AKAM actually trades at a value stock valuation. AKAM is trading at 25x trailing earnings with a significant amount of cash on the balance sheet to buy back stock. While the company does not pay a dividend yet, it does provide a stable growing business that allows you to benefit from technology rebounding in the near future. In the past 10 years, the company has also consistently bought back stock with cash flows which should pick up in 2022 and provide support for the shares. The company is expanding its edge computing business nicely, with over $200m in annual run rate and adding security capabilities over time.

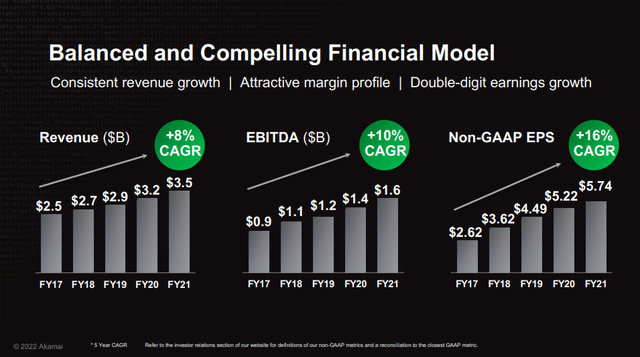

Revenue and earnings growth is impressive (Investor day presentation)

First Quarter Results

The company had 7% growth on the year in 2021 but started 2022 nicely with 9% growth adjusted for FX in Q1. The growing parts of the business Security and Compute both grew nicely and are more than 50% of the business now. As these continue to scale, AKAM may get more credit for these segments and earn a higher multiple again rather than being valued as 'legacy' technology based on the content delivery business. These parts of the business also have structurally higher gross margins, allowing for increasing profitability over the next bunch of years. Over the last 5 years revenue increased on average 8% per year, but EPS increased 16% as scale benefits grow. In Q1 2022, legacy content delivery revenue was down 4% over last year adjusted after foreign exchange fluctuations, showing relative stability with high profitability. The company is seeing some slowing in traffic as OTT streaming and gaming both weakened in recent months. This is to be expected and is more of a return to a longer-term slow growth trajectory than any fundamental change. People are getting out of their homes more but after what may be a slower summer than the past few years the fall should see improvement. The company generated $119 in GAAP income in the quarter with a significant headwind coming from foreign exchange. Businesses with heavy international presence like Akamai will see headwinds this year with a flight to safety in the US dollar and volatility in many currencies.

Profits Leading to Acquisitions

AKAM is utilizing a good portion of cash on hand on acquisitions to bolster the business in the computer and security segments. While the company looks to keep its core Delivery revenue flat, they are focusing on growth elsewhere. The company currently has $1.3 Billion US in cash giving the ability to continue to buy smaller high-growth companies to bolster the business. Akamai is seeing early returns from its Guardicore acquisition from late 2021 as well. After paying $600m and expecting 50 million in revenue in 2022 the price paid was a hefty 20x sales. However, utilizing the large cash position to grow their capabilities in the Zero Trust area is essential for AKAM to continue growth. It will allow AKAM to increase strategic value with customers in mission-critical areas. Being able to prevent malware from spreading once it's in an organization is essential for security. These micro-segmentation capabilities are becoming more important as ransomware and similar attacks have ramped steadily since 2020. The company already signed the biggest deal in history since acquiring the business with a $10m deal over 3 years in Q1. This security deal was followed by another interesting deal in the compute segment.

Linode was added recently in Q1 2022 for 900 million to boost the compute group which includes edge applications, developer tools and infrastructure as a service. 179,000 used it in April due to many wanting a multi-cloud approach with reduced cost outside of the hyperscaler options. Linode will immediately add $100m to revenue this year with growth potential for the long term. Over time it will add $125M in tax benefit giving a reason 7.8x sales multiple. It offers developers a powerful platform to build and scale applications where users will be in the cloud and on devices. Major customers have already moved to Linode and raved about its ease of use. AKAM has a good opportunity to cross-sell and increase the growth rate going forward. The plan is to use their current sales team for Linode, preventing the need for much additional sales expense to increase that growth over the coming years. CEO Tom Leighton describes it as,

"You can just take your container, your app and the container and move it over to Akamai, and have the whole thing end-to-end from the core of the cloud to the edge. You can build your app on Akamai. You can run it on Akamai. You could deliver it on Akamai. You can do the compute you need at the real edge in thousands of places. And of course, we'll wrap it all in security for you."

The real vision there is to be able to offer everything from content delivery networking to edge cloud solutions.

Price Action

The stock has held up much better than many of its technology peers but it still took a significant hit in recent months down around 20%. At 19x forward earnings at the bottom of its valuation range in recent years. Cash flow has continued to increase up to $865 million over the past year to support buybacks - to the tune of $103m in Q1. The company said it would be opportunistic buying back shares, providing support to the stock anytime it drops below its 50d. Anywhere below that level would be a good point to begin building a position.

Conclusion

When looking for value in this market you need to look at strong generators of cash flow, potential for growth in new segments and compelling valuation. Akamai fits the bill for all three of those areas with 2 purchases increasing growth potential in the medium term along with very stable earnings. AKAM is mission-critical for many customers and the core business will continue to generate cash over a long period and provide a great value for investors.

Gloss