SentinelOne Stock: Rapidly Growing Cybersecurity Stock (NYSE:S)

Olemedia/E+ via Getty Images

SentinelOne (S) arguably reflects the kind of stock that can do very well from here. S is a high quality operator in the cybersecurity sector, which is regarded as one of the highest quality sectors in all of tech. The stock price has walloped among the rest of the tech sector, but I expect the stock to return to being one of the market leaders once the market pessimism fades. The stock trades at a premium even to other cybersecurity operators, but its faster growth rate arguably justifies the premium. I rate shares a buy for those with a long-term time horizon.

S Stock Price

After coming public with an IPO price of $35 per share in mid 2021, S now finds itself trading around $30 per share, just below that IPO price.

YCharts

The stock had previously traded up above $75 per share, which perhaps was a tad optimistic, but cybersecurity stocks have historically traded at substantial premiums even to other high-growth tech stocks due to the perception of long-lasting secular tailwinds. At these prices, investors can buy into S at below-IPO prices.

What is SentinelOne?

Let me explain how S fits in within the cybersecurity space.

SentinelOne

S offers an AI-powered extended detection and response platform - or XDR platform. This is most commonly known as endpoint protection. Endpoint protection means protecting endpoints (computers, phones, and mobile devices) from malicious attacks.

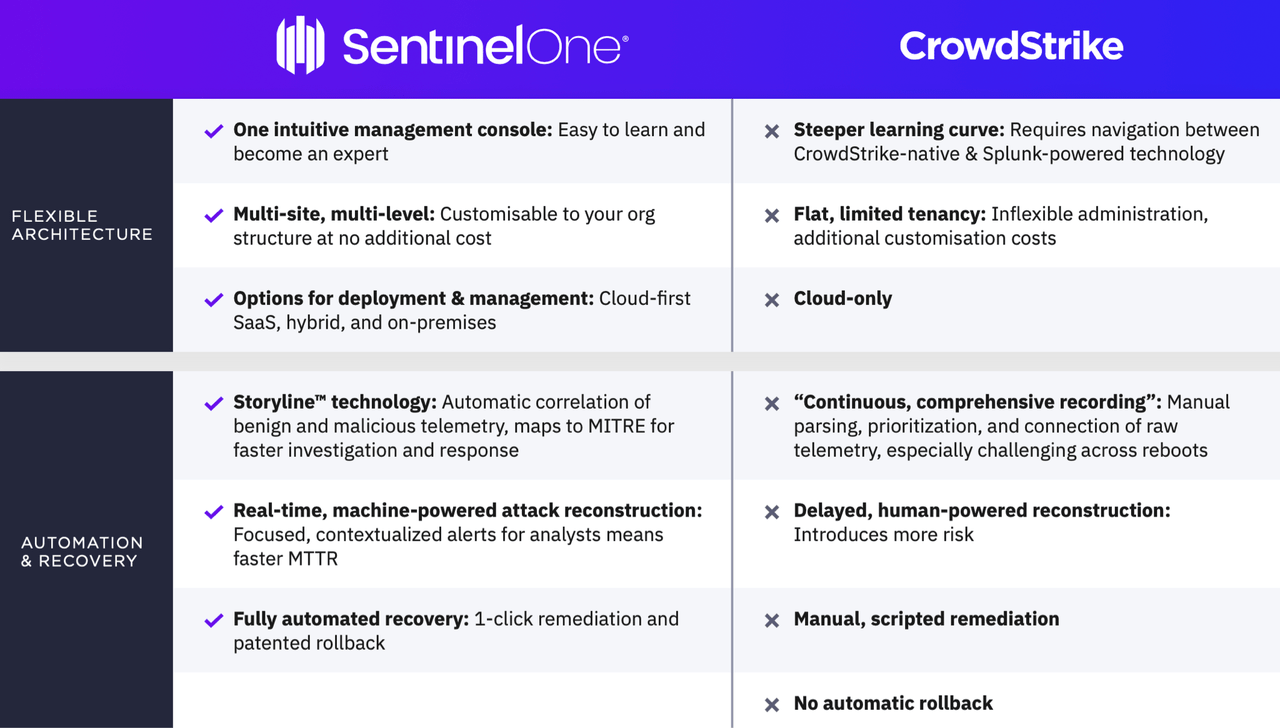

That puts the company in direct competition with CrowdStrike (CRWD). S believes that its AI-powered response gives it a better offering than that of CRWD. We can see how their products differ below:

SentinelOne

As S points out in its S-1, “popular endpoint recovery (‘EDR’) offerings are subject to the ''1- 10-60' rule which means that the best achievable cybersecurity outcome was capped at one minute to detect an attack, ten minutes to investigate, and 60 minutes to respond.” S’s artificial intelligence software instead automatically investigates and responds to the threat, removing the need for manual remediation.

S Stock Earnings

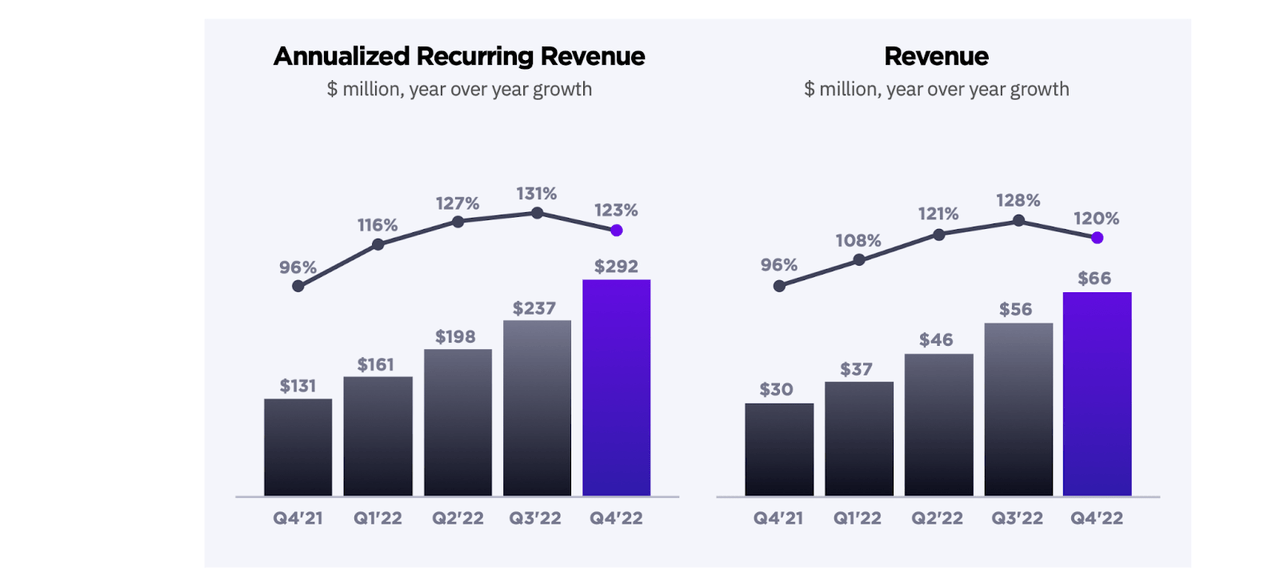

S closed out the year with strong results. The company grew revenue by 120% year over year to $66 million. The company had previously guided for $61 million in revenue.

SentinelOne Shareholder Letter

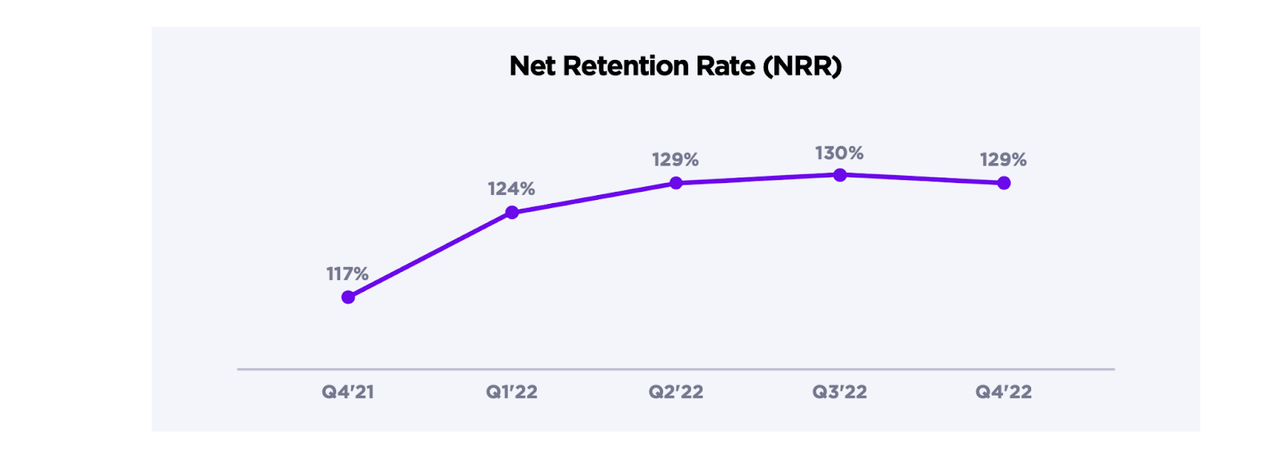

In addition to growing its customer base by more than 70% in the quarter, S also maintained a high 129% net retention rate.

SentinelOne Shareholder Letter

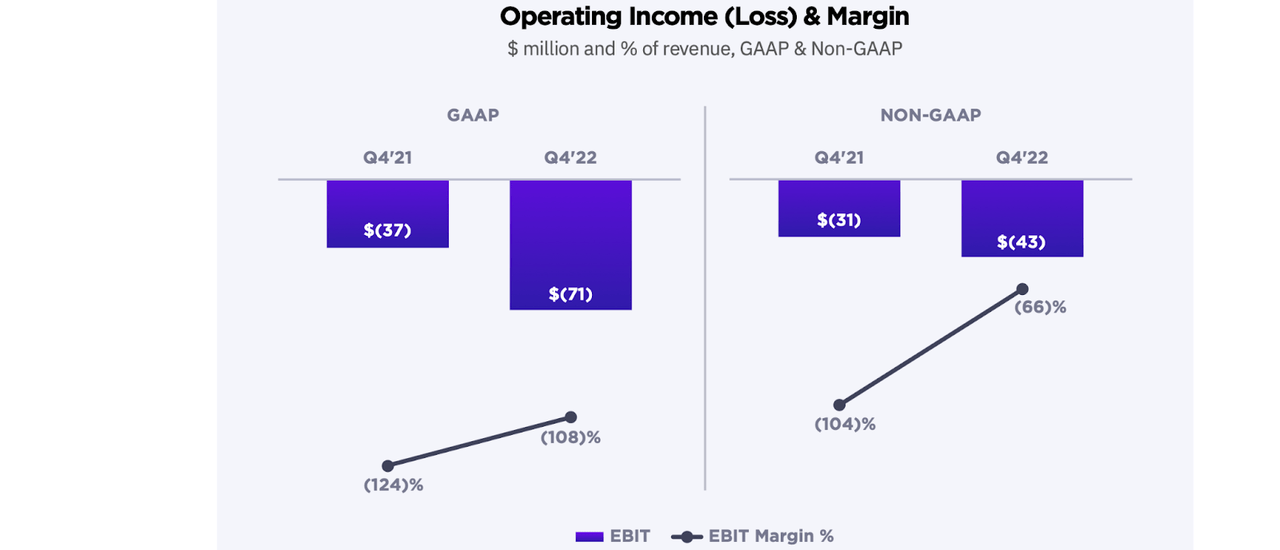

The one (though important) issue with the quarter was the 66% non-GAAP operating margin loss.

SentinelOne Shareholder Letter

Those negative cash flows differ greatly from the typically cash flow rich positions of cybersecurity peers like CRWD and Zscaler (ZS). S did issue strong guidance implying 80% year over year growth to $370 million next year.

SentinelOne Shareholder Letter

Is S Stock A Buy, Sell, or Hold?

At recent prices, S is trading at 33x annualized sales and 24x forward sales. Net cash of $1.6 billion makes up nearly 20% of the market cap, but the company is burning over $200 million of cash annually. As a result, the net cash is useful to consider for valuation purposes, but it is unlikely that S announces a share repurchase program at least in the near term. At the very least, the net cash position should help the stock sustain a premium multiple as it gives it financial strength to steadily move towards a cash flow neutral position. S trades at a notable premium to the 28x annualized sales at CRWD, but a premium makes sense considering that S is expected to grow considerably faster at 80% versus 49% at CRWD. On the flip side, the premium isn’t nearly as large as I would expect, and that is likely due to the stronger free cash flow generation at CRWD. It is worth noting that S’s valuation on a price to sales basis is very comparable to that of CRWD on a forward basis, even though I expect S to grow considerably faster thereafter. While neither S nor CRWD are the cheapest in the tech sector, they were not cheapest prior to the tech crash and thus it isn’t a surprise to see the stocks maintain some premium even today. I expect S to earn a 40% net margin over the long term. Applying a 1.5x price to earnings growth ratio (‘PEG ratio’), and a 50% growth rate after next year, I could see S trading at 30x sales in 1 year. That reflects 25% upside over the next 12 months, but my 1.5x PEG ratio and 50% projection may both prove too conservative.

There are two important risks here. First is that of valuation. Because S trades at a premium to other tech stocks, there is increased likelihood of the stock experiencing elevated volatility in the near term. Many other high quality tech stocks have seen their multiples compress to extraordinary levels - while S has seen its stock hit hard, its multiples remain quite healthy. Share price movements will not hurt its financials due to the strong balance sheet, but investors should be prepared for volatility. Another risk is that of competition. There is no guarantee that S will be able to compete effectively against CRWD. That might lead to growth slowing down considerably, which may make it difficult to achieve and sustain profits. Cybersecurity is arguably a large market, but investors should keep a close eye for any signs of competition eating into the financials. I rate S a buy due to the long growth runway and reasonable valuation, though note that better investment opportunities are readily available in the tech sector.

Gloss