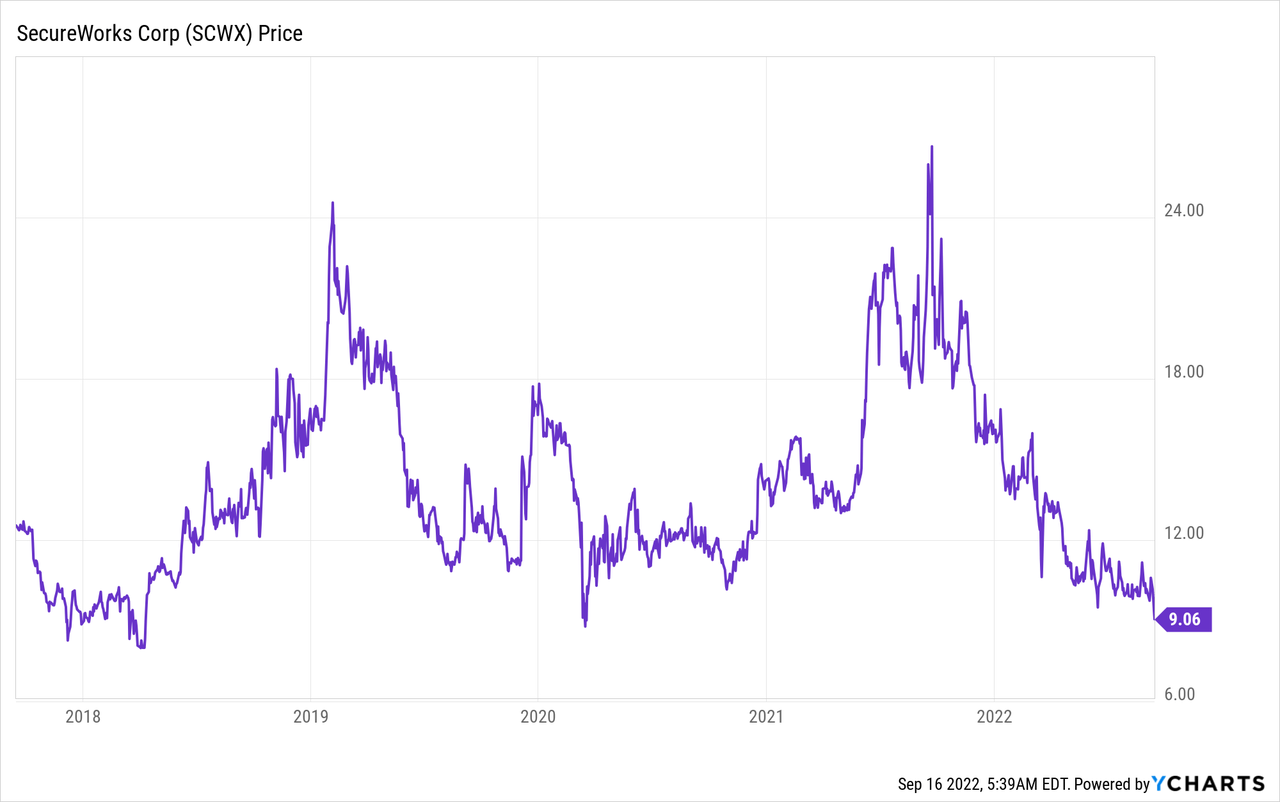

SecureWorks: Potential Turnaround With $100B Cybersecurity TAM (NASDAQ:SCWX)

xijian

Our increased connectivity has widened the attack surface for hackers and caused a major boost in cyber attacks. In fact, Cybercrime is expected to cost the world an eye-watering $10.5 trillion by 2025. With the average ransomware breach costing a company $4.54 million. Given this fact it's not a surprise, that the global cyber security market was valued at $155.8 billion in 2022. This is forecasted to grow at a rapid 13.4% compounded annual growth rate [CAGR] and reach $376.3 billion by 2029.

SecureWorks (NASDAQ:SCWX) is a cybersecurity company that is poised to ride the growth in this industry. The company has had an interesting history, founded in 1999, it has built a strong reputation among Fortune 100 companies for its Managed Security Services [MSS]. Then in 2011, Dell acquired the company before taking the company public again in 2016. Today, Dell still maintains a large ownership stake which gives the company a "mothership" to leverage. Since 2019, the business has been focusing on its Software as a Service [SaaS] solution which has gained strong traction in the market. However, over the past couple of years, the financials for its legacy businesses have been declining as they undergo this transition. Management believes the fiscal year 2023 is an "inflection" point and the strong growth in its SaaS product backs this up. The company has recently beat both revenue and earnings estimates, thus it has all the ingredients of a "turnaround". SecureWorks estimates its total addressable market to be worth $98 Billion by 2025, thus there is plenty of runway ahead. In this post, I'm going to break down its business model, financials, and valuation, let's dive in.

Secure Business Model

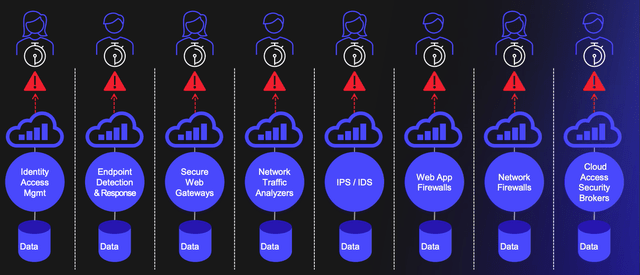

Many companies have gradually built up their cybersecurity technology stack with a series of single-point solutions. This could involve a solution for Identity Access Management (usernames/passwords) such as Okta, an endpoint protection platform, Network firewalls from Palo Alto Networks, and more. The issue with this is many of these various solutions don't "talk to each other". In addition, Security analysts can spend up 30 minutes investigating each individual alert which is labor intensive.

Siloed Solutions (SecureWorks)

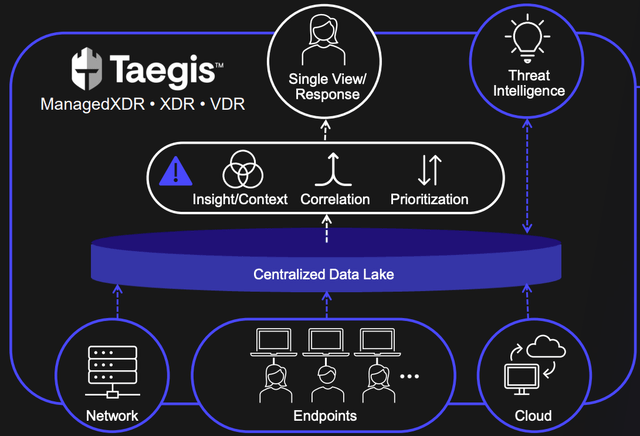

SecureWorks' solution was to create an extended detection and response platform [XDR] called "Taegis" which brings multiple tools into one platform. This provides a "single pane of glass" for security consultants and IT admins, which enables them to act faster. The platform also seamlessly brings all security data and alerts together from cloud apps, endpoints (employee PCs), and the network. It does this via a "Centralized Data Lake" which enables insights to be derived with artificial intelligence and security alerts to be prioritized.

SecureWorks Platform (Investor presentation)

Similar to CrowdStrike (CRWD), the platform also integrates with Human Intelligence via their SecureWorks Counter Threat Unit. This enables its team of IT Security experts to prioritize, "hunt" and ultimately beat the hackers. For example, the company outlines the story of a customer who contacted the Counter Threat Unit, because they detected a "Network Scan" on their system. This is usually not a major issue in itself, but can be used by a hacker who is looking for gaps in a system. In this case, that was true and the hackers had stolen every password in the entire company. Usually, these hacker groups would hold the passwords "hostage" until a sum of money is paid "ransom". In this case, SecureWorks prevented that by eliminating the hackers and all its ransomware in less than 6 hours. For Chief Financial Officers [CFOs] who are usually part of the buying committee at large organizations, SecureWorks boasts a payback period of less than 3 months. In addition, the platform is designed for automation and integrates with popular SaaS platforms such as ServiceNow, Zendesk, PagerDuty, and Jira. It also has a live chat function which gives customers direct access to security experts.

SecureWorks is a leader in managed threat detection and response with a 4.6 out of 5-star rating on Gartner. In addition, they have a 4.5 out of 5 star rating on G2. This is great, but there are larger competitors which rank higher such as CrowdStrike, I will elaborate on this later in the "Risks" section.

Solid Financials

SecureWorks generated solid financial results for the second quarter of fiscal year 2023. Revenue was $116 million, which beat analyst estimates by $79,000, but did decline by 13% year over year. This decline in revenue has been a historic trend as the company transitions to a new business model, which will focus on its Taegis platform.

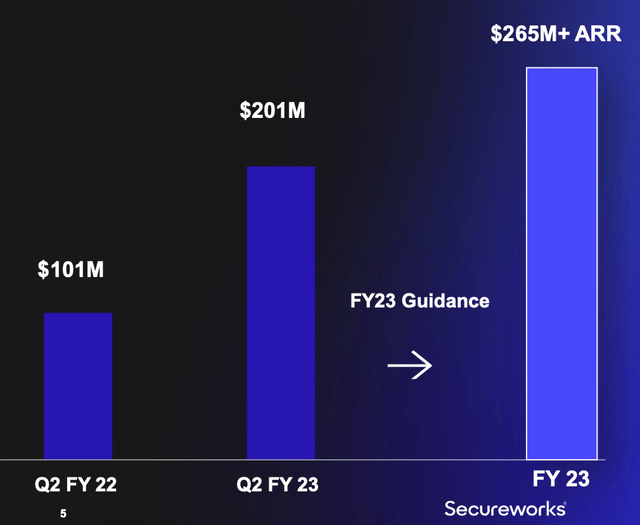

The good news is Taegis was a key revenue driver bringing in $43 million in revenue and increasing by rapid 131% year over year. Annual Recurring Revenue [ARR] which is a key metric for SaaS companies, increased to $201 million for its Taegis product alone, which now makes up 56% of total ARR. Management is also on track for Taegis to make up ~75% of ARR by the end of this fiscal year. This is great to see and means over time the previous trends in declining revenue should start to reverse.

ARR (Investor Presentation)

The Taegis product also added 800 new customers which increased by 114% year over year.

The company generated earnings per share of minus $0.39 which beat analyst expectations by $0.04. When I dive into the income statement I see that despite the losses, investment is going into the right place. For example, the business invested $39.3 million into Sales & Marketing, which was an increase of 16.8% year over year. This helped to drive the aggressive growth of its relatively new product/business line Taegis. In addition, R&D increased by 7.4% year over year to $31 million, as the company improves its product. It was great to see that General & Administrative Expenses declined by 7.8% which demonstrates improved efficiency of its operation.

Income Statement (Q323)

The company has a solid balance sheet with cash & short-term investments of $167.5 million. In addition to total debt of just $14.3 million which is great given the rising interest rate environment.

Guidance - FX Headwinds

Moving forward Taegis is facing FX headwinds from a strong dollar which is impacting international revenue. Thus, they expect lower professional services revenue than previously expected, in the $458 million to $465 million range. The good news is ARR guidance for its Taegis product is still the same and they expect over $265 million for the FY 2023. Management is expecting sales to accelerate into the second half of the year as the business benefits from its investments.

Advanced Valuation

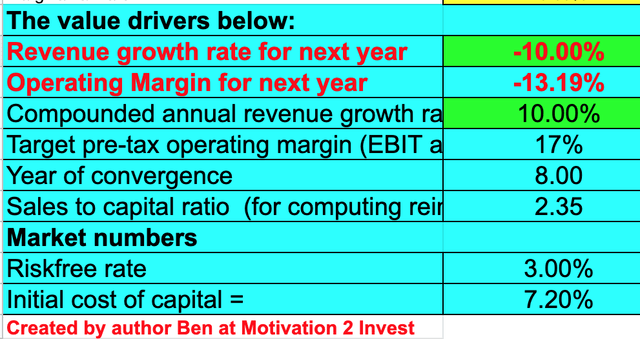

In order to value SecureWorks, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow method of valuation. I have forecasted revenues to continue to decline by 10% for next year as the company transforms its business model. However, for years 2 to 5 I am forecasting revenue to turnaround as the rapidly growing Taegis product makes up a greater portion of the total. I have forecasted a steady 10% growth rate per year between years 2 to 5.

SecureWorks (created by author Ben at Motivation 2 Invest)

I have forecasted the company's operating margin to increase to 17% over 8 years, which is still below the 23% average for the software industry. I expect this to be driven by the SaaS platform making up a greater percentage of revenue and declining G&A costs as per the current trend. In addition, I expect FX headwinds to improve and thus this will allow the margins to breathe. In addition, I have capitalized R&D expenses to increase the accuracy of the valuation.

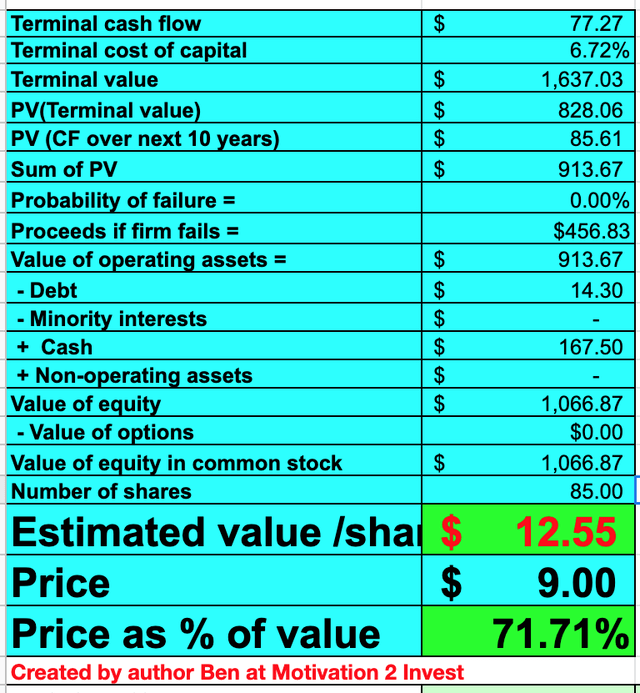

SecureWorks stock valuation (created by author Ben at Motivation 2 Invest)

Given these factors I get a fair value of $12.55 per share, the stock is trading at $9 per share at the time of writing and thus is 28% undervalued.

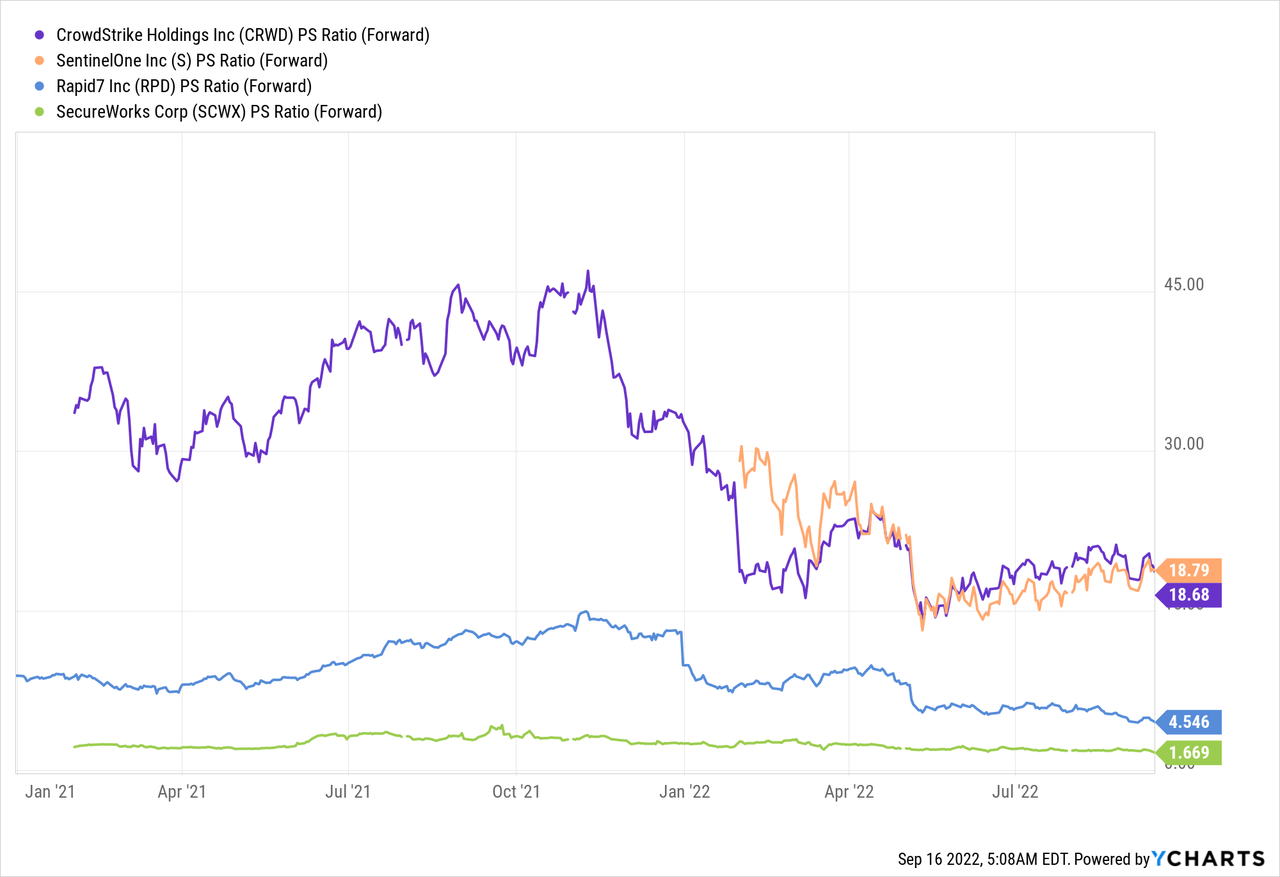

As an extra data point, SecureWorks trades at a forward Price to Sales ratio = 1.67. This is significantly cheaper than competitors such as SentinelOne (S) which trades at a PS = 18.79, CrowdStrike PS = 18.68 and even Rapid7 (RPD) which trades at PS = 4.5.

Risks

Competition

I believe SecureWorks is doing the right thing in transforming its business model and the market agrees with its product gaining major traction. However, it should be noted there are much larger and more established players in the extended detection and response market such as the market leader CrowdStrike, Rapid7 and even SentinelOne. Thus the company doesn't really have a moat or competitive advantage which could be an issue long-term.

Recession/IT Spending Slowdown

The high inflation and rising interest rate environment has caused many analysts to forecast a recession. This may cause enterprises to delay IT spending until more economic certainty is provided. The good news is I believe this is just a temporary issue and the long-term trend in security spending is up.

Final Thoughts

SecureWorks has a great product and is undergoing a business model transformation. Its revenue is still declining but is still coming in above analyst expectations. Management is forecasting the majority of the transition to be complete by the end of FY23 and thus given the stock's cheap valuation, a turnaround looks likely in the long term.

Gloss