NortonLifeLock Stock: Put This Cybersecurity Play On Your Radar

Galeanu Mihai/iStock via Getty Images

Enterprises get most of the attention when one thinks of cybersecurity, but it's just as important for retail customers, given the growth of identity theft and financial fraud. This brings me to NortonLifeLock (NASDAQ:NLOK), whose stock has traded rather sideways over few months, remaining virtually flat since the start of the year. This article explores whether NLOK is a buy at the current price, so let's get started.

NLOK: Put This Stock On Your Radar

When you hear the name Norton, the first thing that likely comes to mind is antivirus software. Indeed, Norton has been in the business of cybersecurity for over 30 years and is a well-known player in this space. However, NortonLifeLock is much more than just an antivirus company. It's a comprehensive provider of consumer security products, services, and solutions.

The company has a portfolio of security products for consumers, including Identity Safe, which helps protect users' identities and personal information, Norton Security, which provides protection for devices from malware and other online threats, and LifeLock, which helps guard against identity theft. NLOK also offers Norton WiFi Privacy, which helps protect users' online privacy.

NLOK is seeing respectable growth, with revenue growing by 10% (12% on a constant currency basis) YoY during the fiscal third quarter (ended December 31st). This was driven in large part by robust direct customer growth of 2.4 million, bringing the total number of customers to 23.4 million. This marks the ninth consecutive quarter of sequential customer growth.

Also encouraging, NLOK is seeing positive operating leverage through its scale, as reflected by op margin increasing by 180 bps over the prior year period to 52.8%. This resulted in free cash flow growth of 13%, which is higher than the aforementioned revenue growth.

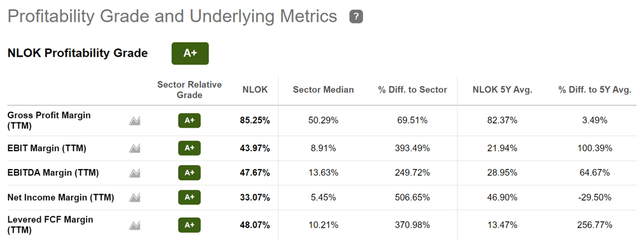

NLOK maintains relatively strong margins, which helps it to score an A+ rating for Profitability. As shown below, NLOK posts sector leading EBITDA and Net Income margins of 48% and 33%, respectively.

NLOK Profitability (Seeking Alpha)

Looking forward, NLOK is well-positioned for continued growth, as management expects to close on its pending acquisition of Avast, a Czech company, in the middle of this year. This should help to accelerate NLOK's international expansion as well as upsell opportunities on existing customers at Avast, which has found success with its freemium model.

Risks to the thesis include recent concerns from UK's anti-trust regulator, which launched a deeper investigation into the merger following competition concerns. In addition, NLOK must contend with competition from free antivirus providers, and LifeLock must contend with competitive offerings from the big 3 consumer credit agencies, Experian (OTCQX:EXPGF), TransUnion (TRU), and Equifax (EFX).

Meanwhile, NLOK pays a 1.9% dividend yield that's supported by a low 30% payout ratio. While dividend growth has been lacking over the past couple of years, I would expect to see future growth as management continues to deleverage the balance sheet. Since April 2020 (end of fiscal year 2020), NLOK's debt has been reduced by $962 million, to $2.76 billion at present, and currently carries a BB credit rating, sitting 2 notches below investment grade.

NLOK doesn't appear to be particularly cheap nor expensive at the current price of $26.55, with a forward PE of 15.3, sitting just above its normal PE of 15.2 over the past decade. Analysts estimate 6.5% to 12% EPS growth over the next 4 quarters, and have a consensus Buy rating with an average price target of $26.57.

Investor Takeaway

NortonLifeLock is a leader in the consumer security space, with a comprehensive suite of products and services. The company is seeing strong growth, driven by robust customer acquisition, and is benefiting from positive operating leverage. NLOK is also well-positioned for continued growth through its pending acquisition of Avast.

Risks to the thesis include regulatory concerns surrounding the merger, competition, and the company's high debt levels. Meanwhile, NLOK pays a modest dividend yield that is supported by its free cash flow generation. The stock doesn't appear to be particularly cheap or expensive at the current price. Considering all the above, I view the stock as being a Hold at the moment, with a target PE valuation of 14.0 or below.

Gloss