Nikola (NKLA): Lack of Proprietary Technology, Not Enough Progress

Nikola Stojadinovic/E+ via Getty Images

Over the last year, Nikola (NASDAQ:NKLA) turned around the business moving away from their fraudulent past to actually producing BEV heavy-duty trucks. The stock became interesting due to the opportunity ahead, but investors were warned to watch for positive developments on truck orders and capital raises before diving into the stock. My investment thesis remains Neutral on the stock due to the lack of progress on stated goals.

BEV Delays

Nikola reaching production on the BEV Tres was a phenomenal accomplishment after the founding CEO was found to have committed fraud. The company actually selling the trucks has been a far different story as the sector quickly became crowded with Tesla (TSLA) delivering their Semi truck to PepsiCo (PEP) at the start of the month.

The biggest question was whether Nikola had anything proprietary and the lack of orders would suggest otherwise. The hydrogen EVs have a far more compelling story, if not for the stock valuation and capital needs.

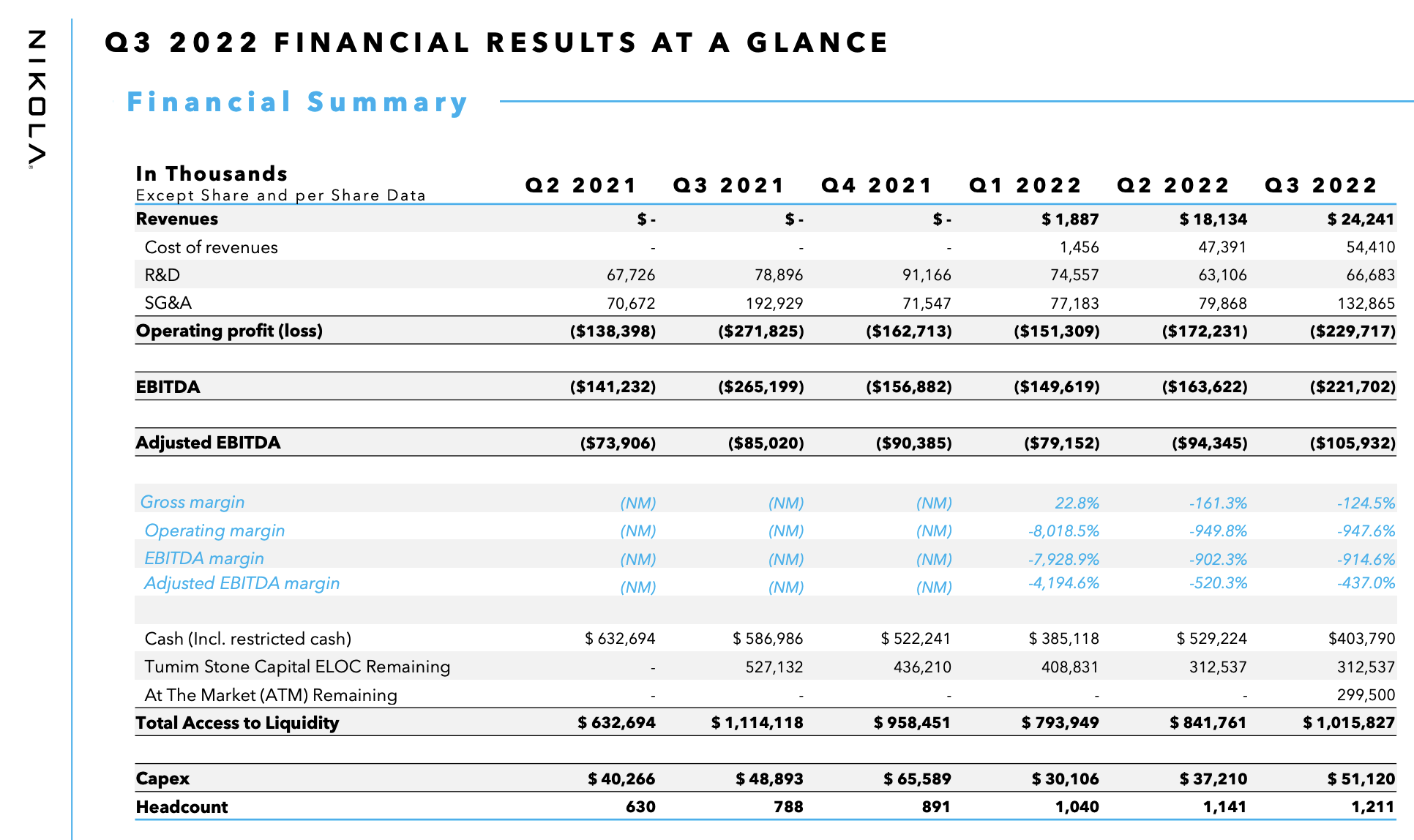

For Q3'22, Nikola reported revenues of only $24 million on the delivery of 63 BEV Tres. The company produced 75 trucks in the quarter and only discussed the 100-truck purchase order from Zeem Solutions.

The financial picture remains very murky with operating losses and EBITDA widening as the company ramps up production. Nikola lost $230 million in Q3'22 and the EITDA loss was $106 million with capex spending of $51 million.

Source: Nikola Q3'22 presentation

The large difference between the losses was $103 million in stock-based compensation. Due to the SBC and ATM, Nikola has seen the share count boosted to 438 million shares in Q3 with the diluted share count far higher at over 490 million shares at year end.

Nikola needs far more orders and plans to produce beyond 3 BEV Tres over one daily shift with the capacity for 5 trucks per shift. The company expects to complete Phase 2 construction soon pushing capacity to 20,000 units per year, but Nikola is only producing what amounts to ~750 units a year.

Investors should've noticed how the earnings release quickly shifted to discussing the energy business with only a minor update on the Tre BEV vehicle in actual production. On the Q3'22 earnings call, the new CEO discussed some of the issues with the truck market leading to the deferring of the Phase 3 expansion until at least 2024:

Where we can improve is on the commercial side of the business. It's clear that there are macro headwinds right now that at some point will turn into macro tailwinds. We must take proactive steps to make sure that we have a commercial program in place that will allow us to fully benefit when the market dynamics become more favorable. I believe we can achieve this by increasing our dedicated sales efforts to better understand our customers and their needs. We need to become less dependent on dealers and instead lead them in our commercial management.

Our prior research had highlighted this risk as a prime reason to remain on the sidelines. Nikola made impressive progress getting the truck produced, but selling trucks for a profit is a whole different story and the company had failed to announce any meaningful orders.

The CFO didn't even guide to Tre BEV deliveries in Q4 despite expectations for production of anywhere from 120 to 170 units. At the time, Nikola should be ramping up sales expectations and full speed ahead on selling BEVs, but the company is already headed to the next big opportunity due to charging infrastructure issues limiting orders and high costs limiting the internal desire to sell more trucks.

Hydrogen Promise Isn't Enough

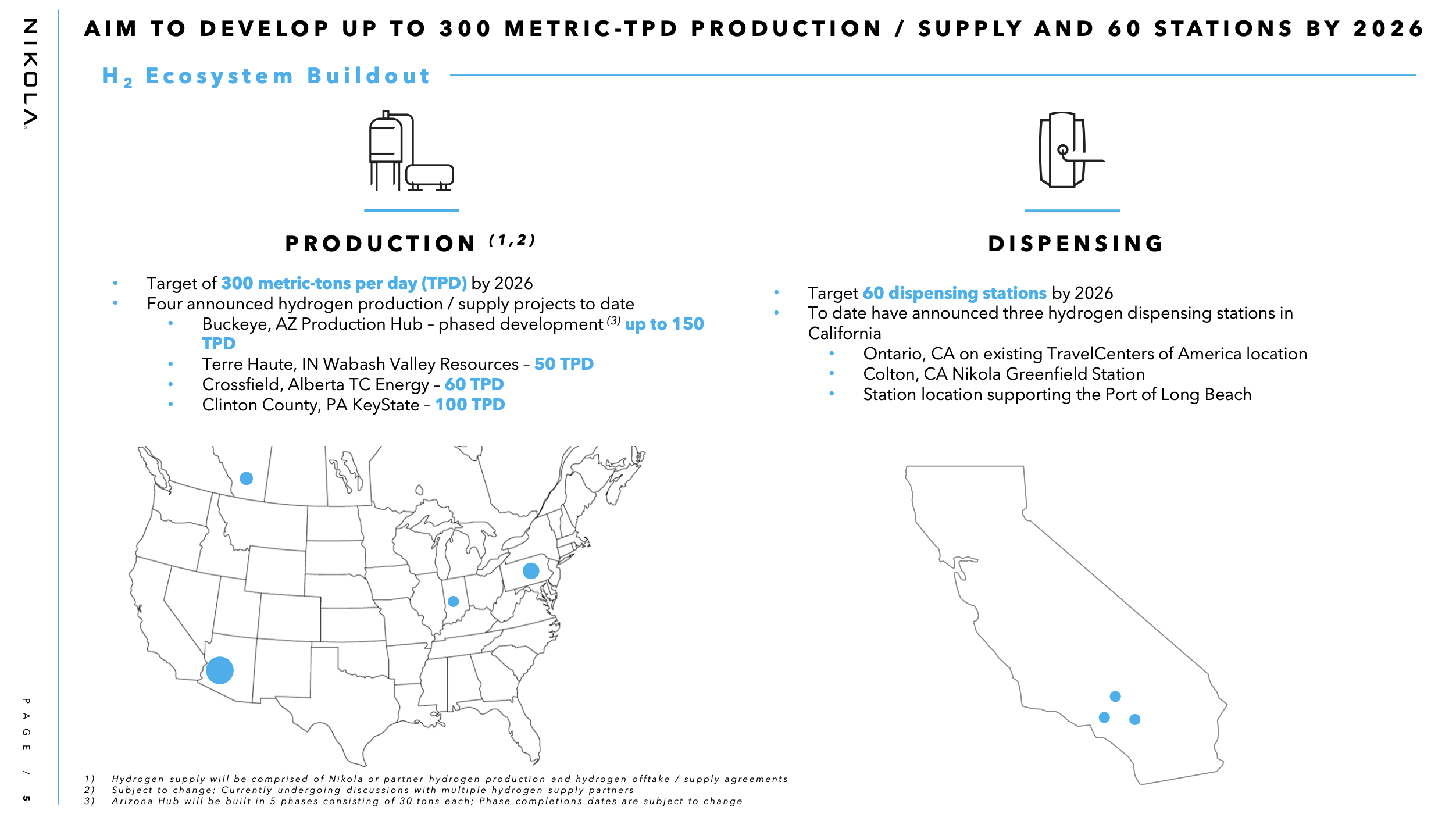

The odd part of the Q3'22 earnings presentation and a lot of the news items recently is that Nikola appears to have shifted to an energy company from one focused on producing heavy-duty trucks and needing energy supplies for customers to fuel the trucks. Nikola now aims to develop a large network of hydrogen dispensing stations with up to 300 metric-bpd of production via 4 facilities around North America.

Source: Nikola Q3'22 presentation

The company is working on a loan form the government for the Phoenix Hydrogen Hub project providing the capital to fully develop the 150 metric-tpd production facility. Once final investment decisions and customary regulatory approvals are finalized, construction of the first phase is anticipated to be completed in 2024.

Nikola even announced a deal with Plug Power (PLUG) for a 30-tpd liquefaction system at the Arizona hub and up to 125-tpd of hydrogen by 2026, with 80% under a take-or-pay contract. The one interesting aspect of the deal is the purchase by Plug of 75 Nikola Tre fuel cell electric vehicles to bring green hydrogen to Plug customers with the first delivery in 2023.

Even with the excitement around using hydrogen as a fuel source and the supposed demand around the Tre FCEVs is that Nikola remains at the bleeding edge. The company burned ~$180 million in cash during Q3 and the company has another year before the new trucks are even launched under the best scenario. In addition, our research has already identified Plug Power as a company big on making announcements and low on delivering results.

Nikola ended the last quarter with a cash balance of only $404 million with the other sources for liquidity causing massive dilution with the stock down to only $2. A large government loan might provide a solid source of liquidity for the hydrogen ecosystem, but the company has to show how the business transitions from the bleeding edge and ever makes a profit after the BEV failure.

Takeaway

The key investor takeaway is that investors should continue watching Nikola from the sidelines. The company has transitioned to being able to build trucks, but the executive team hasn't shown any ability to transition to selling trucks and operating a growing company. The biggest concern now is the lack of proprietary technology in an increasingly crowded space.

Gloss