MIND Technology: Outlook Still Uncertain Despite Improved Order Levels

donvictorio/iStock via Getty Images

MIND Technology (NASDAQ:MIND, NASDAQ:MINDP) or "MIND", formerly known as Mitcham Industries is a micro-cap provider of technology and solutions for exploration, survey and defense applications in oceanographic, hydrographic, defense, seismic and security industries.

Strategic transformation and ambitious growth targets

The company recently exited its seismic land leasing business as a result of the strategic decision to focus on the marine industry with its Seamap subsidiary providing the lion's share of the segment's revenues.

Company Presentation

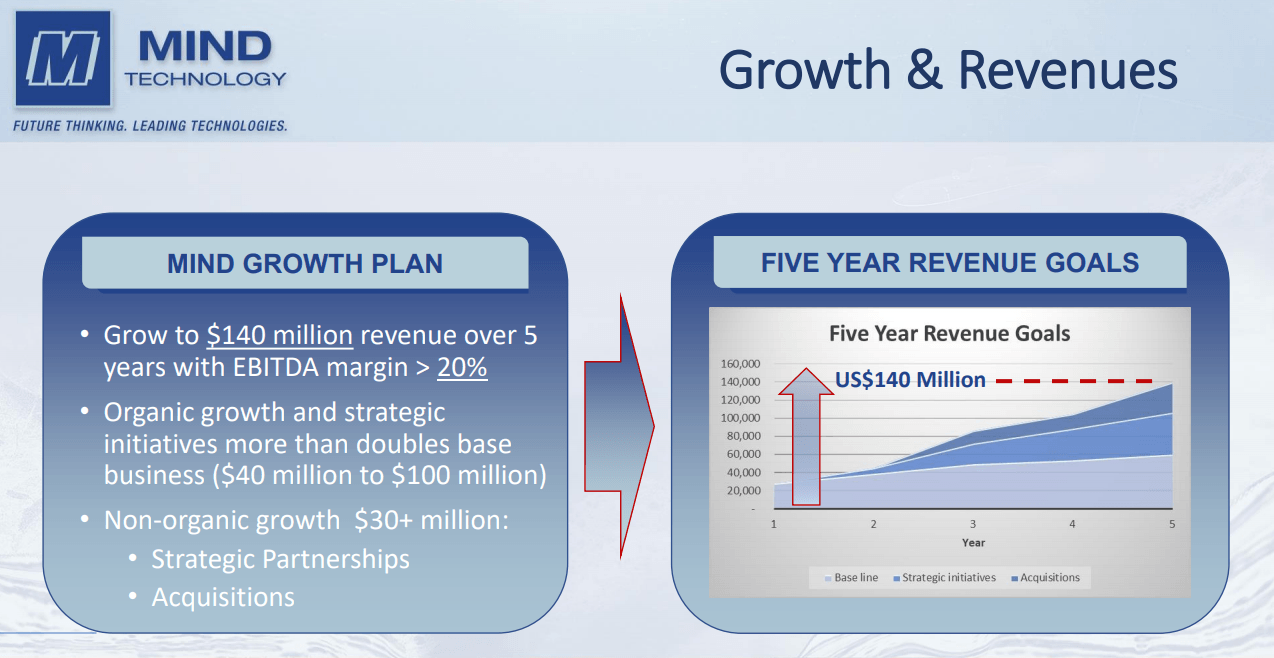

Last year, MIND Technology embarked on an ambitious growth plan with revenues expected to increase sevenfold over the next five years to $140 million with EBITDA margin to exceed 20%:

Company Presentation

Unfortunately, the company hasn't made much progress in FY2022 with sales increasing just 9% to $23.1 million while backlog was down 8% to $13.1 million. In addition, cash used in operating activities almost tripled to a whopping $17.1 million.

Cash outflows were partially offset by $6.2 million in proceeds from lease equipment and business unit sales.

In addition, the company raised $14.7 million from the sale of additional 9.0% Preferred Stock.

The fourth quarter was particularly weak as the company experienced additional supply chain bottlenecks and delivery delays.

On the flip side, management pointed to solid business activity and recently increased backlog levels:

Inquiry and bidding activity remain robust. As we announced last week, we have recently received significant new orders and have other pending orders that we are highly confident in receiving. Coupled with our backlog of approximately $13.1 million as of January 31, we believe our current book of business is in excess of $23 million. This is significantly higher than we have seen historically and of course does not include numerous other prospects that we are actively pursuing. Based on these factors, we expect revenues from continuing operations in fiscal 2023 to exceed those of fiscal 2022 and we think that improvement will be seen beginning in the first quarter.

At this point, there appears to be just one analyst estimate for FY2023 with sales expected to almost double year-over-year to $45 million which, at least in my opinion, looks unrealistic given ongoing supply chain and logistical challenges.

On the conference call, management nevertheless provided a rather upbeat outlook for this fiscal year:

While it’s evident that supply chain challenges and inflationary pressures remain a factor, we’re encouraged by what we’re seeing in terms of orders across our business. There will always be some level of micro economic uncertainty, we feel that with the robust interest, customer optimism and quote requests we’ve received to-date, we’re positioned to meaningfully grow revenue in fiscal 2023.

Given the possibility of supply chain disruptions, the timing of orders may be pushed. But it’s important to note these orders are not disappearing. We have a strong backlog and we’re seeing increased customer engagement. After taking all of this into consideration, we are confident that fiscal 2023 will be much improved over fiscal 2022.

We will always remain vigilant when it comes to our cost management and we’ll navigate any supply chain and logistical challenges to the best of our ability if they should arise. We’re optimistic about the upcoming opportunities for MIND throughout the year and we look forward to achieving our long-term goals and generating meaningful shareholder value.

In addition, management remained optimistic to self-fund projected growth, but with just $5.1 million in cash on hand at the end of January and no further sales proceeds from former lease pool equipment, I would expect MIND requiring up to $10 million in additional capital this year.

While the company has at-the-market offering programs for both its common and preferred stock in place, selling more equity won't be an easy task with the preferreds currently yielding 13.5% and the common shares changing hands around $1.25 with an average trading volume of just 136K shares.

Bottom Line

After a disappointing FY2022, management expects "meaningful" growth and "much improved" results this year.

Despite the positive outlook, I am hesitant to keep my "buy" rating on the shares given management's less-than-stellar execution record, sky-high analyst expectations and the likely requirement to raise additional capital this year.

With shares down more than 50% from my coverage initiation 14 months ago, it's time to apologize for a bad call.

Gloss