Micron Technology’s Troubles: It’s The Company, Not The Economy (NASDAQ:MU)

Micron Technology's (MU) stock has dropped 14% since the start of August 2020. However, I will show in this article that the problems with MU started back in 2018, have still not been reconciled, and continue to this day.

What's responsible for the poor stock performance for MU, when other semiconductor peers have skyrocketed? For example, Nvidia (NVDA) is up 115% year-to-date and 150% since January 2018. AMD (AMD) is up 83% year-to-date and 660% since January 2018. Again, MU is up just 3% YTD.

These three companies sell different products, and MU has a synergy with both NVDA and AMD. The CPU or GPU processors the latter companies put into PCs, servers, and games all need memory chips. And even more problematic is that the more advanced electronic gadgets these processors go into, the more memory is required, but MU stock continues to drop.

IDM vs. Foundry Supply/Demand Factors

All chips are built with supply/demand dynamics in mind. Too much supply leads to excess inventory and lower ASPs (average selling prices). Astute management monitor product market demand internally and often using third-party analysts. For supply, it’s a numbers game – build just enough chips to meet calculated demand so operating margins aren't impacted.

That works well for fabless chip companies that use foundries to make chips, such as NVDA and AMD. Based on calculated demand, they place an order to a foundry such as TSMC (TSM) to make the chips and wait for the chips to be drop shipped to their warehouses.

Companies that make their own chips, IDMs such as MU, face a more complicated process. They need to calculate when to build a new fab or expand an existing one, and purchase equipment to fit the expansion. In the case of MU and other DRAM companies Samsung Electronics (OTC:SSNLF) and SK Hynix (OTC:HXSCL), their fabs house equipment can be used to make different chips, and calculated demand need could entail converting a line from one type of DRAM to another, say mobile to server DRAM, or even DRAM to NAND. These actions necessitate the fab be shut down for a period of time, and this too plays into the juggling memory DRAM manufacturers need to address.

Micron is Poor at Recognizing Supply/Demand Dynamics

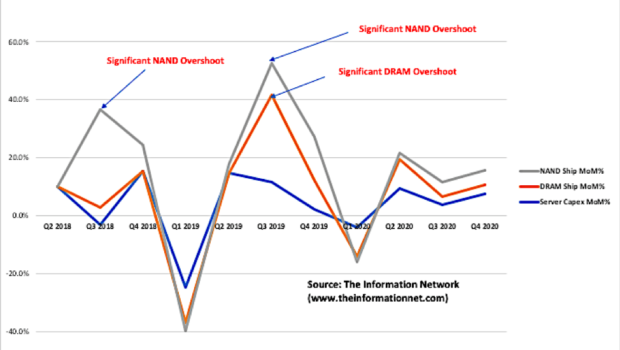

Chart 1 shows Micron’s DRAM (orange line) and NAND (grey line) MoM change in bit shipments between CY Q2 2018 and Q2 2020 and forecast to Q4 2020. It also shows server capex (blue line) over the same period for the following companies:

The definition of capex as it applies to these datacenter companies involves complex real estate designations, but the common denominator are spending on servers containing memory chips and processors that are used to store and disseminate data.

Chart 1

In Chart 1, MU significantly overestimated server NAND demand in mid-2018 and mid-2019 and DRAM demand in mid-2019. As a result, MU overshot production of NAND and DRAM, which resulted in inventory overhang and a drop in ASPs during this period.

On May 30, 2018, MU stock reached a high of $62.57 and has retreated since. DRAM and NAND bit shipments and server capex demand dropped precipitously in CY Q4 2018, reaching a low point in Q1 2019.

Thus, MU’s stock can be correlated with bit shipment overshoots, which resulted in ASP drops. In a series of Seeking Alpha articles in early 2018, I attempted to alert readers that a downturn in MU stock was eminent due to a drop in ASPs that I foresaw due to oversupply in DRAMs and NAND. I refer readers to a March 14, 2018 Seeking Alpha article entitled “More Headwinds Ahead For Mobile DRAMs.”

I also refer readers to notice the comments by MU longs, who were waiting for the stock to reach $100. As I result, I was the most hated writer in Seeking Alpha. At that time, MU stock was trading at $58. Two months later, the stock reached $62 and started plummeting practically on a daily basis, until it reached $29 on Dec. 24, 2018.

Bottom line - readers blamed me in disbelief for pointing out MU's woes, the same people who reverently called MU's CEO Metrotra by his first name Sanjay, and who genuflected on every SA article written by EPhred or William T. Yet MU didn't do anything to rectify the situation, and it continues today.

I bring this up not to gloat or illustrate my analytical prowess, but to question why Micron commenced strong bit shipments of DRAMs and NAND in Q1 2019 (see Chart 1) to such an extent that DRAM bit shipments increased 30% in Q3 2019 and NAND bit shipments increased 11%!

The result – DRAM and NAND inventory overhang and ASPs that started dropping and STILL haven’t recovered. Chart 2 shows that DRAM ASPs started plummeting in CY 3Q 2018 and NAND ASPs started dropping in 2Q 2018, although it can be argued that the drop started in 3Q 2017.

I discussed this very topic of inventory and ASPs in a July 2, 2019, Seeking Alpha article entitled “Micron: Comparing Inventory, Shipments And ASPs With Competitors.”

Chart 2

Chart 2

Chart 3

Chart 3

Servers and Smartphones

This article focuses on server demand for DRAM and NAND because of WDC’s guidance that shipments and prices in 3Q20 are expected to weaken due to inventory cuts by cloud customers. Smartphones are the biggest consumer, and I may discuss MU's miscues on that topic in a later article.

In 2019, servers represented 47.9% of DRAM demand, second to smartphones at 57.9%, according to our report entitled “The Hard Disk Drive (HDD) and Solid State Drive (NYSE:SSD) Industries: Market Analysis And Processing Trends.”

NAND demand is similar. Smartphones represented 30.5% of demand while servers were again second with 15.5% of demand.

Shipments of smartphones have been in decline for the past several years, declining 2.4% in 2018 and 2.2% in 2019 but projected to drop 12% in 2020. Yet, memory demand per smartphone, as I briefly discussed above, has increased from 2.9 GB/phone in 2018 to 3.9 in 2019. That’s a growth of 34%, exceeding global DRAM supply, which increased 23% in 2019.

However, NAND has increased from 57 GB in 2018 to 80 GB in 2019. That’s a growth of 11%, yet global NAND supply increased 42% in 2019.

Investor Takeaway

Micron stock continues to drop because of the company’s poor ability to balance supply and demand in a timely manner to avoid ASP drop and inventory overhang. Today, nearly every article about memory chips is centered on ASPs, and as ASPs continue to drop, Micron stock follows.

Since CY 3Q 2018 when DRAM memory prices started plummeting, Micron’s bit shipments have increased from 6,457 Gb to 8,527 Gb, an increase of 32%. NAND bit shipments increased from 4,270 (16Gb equivalents) to 7,951, an increase of 86%.

In the same time period, DRAM ASPs decreased 55%, and NAND ASPs decreased 44%.

This begs the question. How could a ham-and-egger analyst like me recognize and write about a drop in Micron stock based on changes in supply/demand dynamics just two months before the stock price started plummeting in concert with ASPs? Yet Micron, with all its high-paid analysts, did not direct the company to take action? And let’s not forget about high-paid supply side analysts directing investors, which I tried to do in a Seeking Alpha article at a penny a click?

And how could MU management miss on server supply/demand when servers represent 15 to 50% of NAND and DRAM demand for a company?

MU, and the rest of its peers, need to make drastic cuts in capex spending on advanced equipment from companies like Applied Materials (AMAT) and Lam Research (LRCX).

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Gloss