Micron Technology: Buy A Cyclical Company Near The Trough (NASDAQ:MU)

Introduction

In this thesis, I will start by stating the obvious: that the memory industry is cyclical and that you should buy shares of a cyclical company close to the bottom of the cycle. Afterwards, I try to show that currently we’re closer to the trough than the peak of the (DRAM) cycle. Then I’ll list a few factors I see as signs for improvement in the current cycle. And lastly in a rough valuation, I show why I think Micron (NASDAQ:MU) is currently attractively valued.

Since there are numerous great articles on Seeking Alpha explaining Micron’s products, business model, etc., I’ll skip most of that and focus on what I think is a bit different (and hopefully, value adding) view on the industry and the company. While Micron produces DRAM and NAND memory, I make a few points only on DRAM specifically, as it is the main cash flow contributing business.

Don’t buy a cyclical company at the top

In theory, it is well known that the memory industry is highly cyclical and that you should never buy a company in a cyclical industry at the peak of the cycle. In practice, managements often have still very rosy outlooks at cycle peaks and therefore peaks are not recognized early enough as such. As a consequence, many investors buy at the wrong moment and get burnt as the cycle turns (e.g., energy in 2008 or memory in 2018). Having read many of the Seeking Alpha articles on Micron, I feel that many authors and commentators have had bad investment experiences with Micron, that’s why I’d like to show the industry and the company in a bit different light.

Memory as a cyclical industry with two special traits

The memory industry possesses the typical characteristics of a highly cyclical industry. Manufacturing memory chips is very capital intensive and since the product is commodity-like, the price is primarily determined by demand and supply. If we imagine a memory market in equilibrium, high demand growth pushes the market out of its equilibrium and leads to an increase in prices and margins, which encourage higher industry capex to match the higher demand. This increased capex will lead to higher (over-)supply, and as a consequence lower prices and reduced capex, only to start the next cycle.

Now the memory industry has two specific characteristics, one dampening/shortening cycles and one intensifying cycles. The dampening effect comes from high demand growth, where oversupply (a result of excess capex) is used up relatively quickly by new demand (1-2 years) if capex is kept in check. The other, opposing factor is supercharging swings in the memory cycles. Thanks to technological advancements (node transitions), leading-node manufacturers enjoy(ed) significant cost-per-bit advantages over their less advanced competitors and a node transition allowed for significant bit supply growth (at constant wafer throughput). This means that as soon as the leading manufacturer (usually Samsung (OTC:SSNLF)) could switch to a more advanced node, it had strong incentives to increase output (even as prices drop), since its cost basis would be significantly below competitors’ costs. This is in fact what happened several times over the last decade and sent the memory prices along with the memory manufacturer share prices into wild swings.

While ongoing, albeit a bit slower demand growth will continue in the coming years, the second, “cycle-accelerating” factor is likely to decline – reducing the cyclicality of the market, as described later in this thesis.

The chart below shows clearly the strong swings in margins, which are a result of strong price swings (especially in DRAM, where Micron makes most of its profits). I think what is also interesting to see, that the margins are not only very cyclical, but it seems that every cycle low is above the previous low and that the cycle highs are above the previous highs – also more on that later.

Source: Refinitiv Eikon

For Samsung, one can see similar cyclical movements, albeit with much lower volatility. The main reason is that Samsung is a huge conglomerate, where their memory business is a significant profit contributor, but blends in with all the other businesses.

Source: Refinitiv Eikon

Source: Refinitiv Eikon

Identification of position in the current cycle

So far, we established that the memory industry is very cyclical and that generally you should buy close to the bottom and far away from the peak of the cycle. The next task would be to figure out where in the cycle we are today. I believe that we’re moving towards the trough and are probably not too far away from it. This does not mean that the memory market can’t decline for another 1-2 years, I just believe that it’s more likely to turn upwards again than to continue downwards for the next 3-5 years.

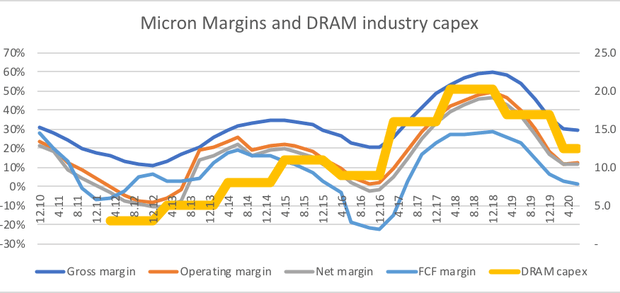

The key factors supporting my belief are the prices and margins which have come down significantly and started to stabilize as well as the industry DRAM capex (Samsung, SK Hynix (OTC:HXSCF) and Micron) which is expected to be 26% below 2019 and 38% below 2018. In my view, industry capex is the decisive factor driving the cycle. In the chart below one can see a strong capex increase between 2012 and 2015, which led to the margin erosion of 2015/16. After a lower capex year in 2016, the margins recovered in the following year and peaked in 2018. So generally, excessive capex leads to oversupply which leads to a slump in margins, which again has a correcting factor on capex.

I’d also like to mention two specific observations: One is that the capex required for the same percentage increase in bit output (let’s say +20%) increases as node transitions become more complex. One reason is that in more advanced nodes, you often etch through more layers, which takes more time and consequently you need more equipment to maintain the same wafer throughput as before. The same is true when multi-patterning (to achieve smaller line widths) which requires more process steps and consequently more equipment and more clean room space. The implication of this is that if memory manufacturers stop increasing capex, the output growth will decline, which has again a stabilizing effect on margins and profits.

The other (and potentially more important) observation is that in the last up-cycle, industry participants reduced their capex already earlier in the cycle compared to 2015/16. An earlier correction (speak reduction) of capex should lead to shorter down-cycles and smaller swings in margins. While it’s too early to see how long the current down-cycle will last, one can clearly see the muted swings in profitability/shallower troughs when comparing the trough margins of 2020 vs. 2016 or vs. 2012. The relatively early reaction (some still argue it was too late) on cutting capex in the current cycle is also an indicator that industry participants are behaving more rationally, preferring more stable margins over possible market share gains.

Source: Refinitiv EIKON for margins, IC Insights for DRAM capex estimate

Source: Refinitiv EIKON for margins, IC Insights for DRAM capex estimate

Industry capex numbers show a clear decline between 2018 and 2019 with a further decline projected for 2020.

Source: Company annual reports and IC Insights for capex estimates

Indicators for an emerging cycle recovery

As I mentioned above, I think industry capex is the single most important factor that decides whether the industry as a whole and Micron in specific will be profitable in the coming years. While there can’t be a guarantee that the industry participants won’t boost their capex, there are still some indicators that rational (= no excessive capex) behavior will prevail.

Micron publicly stated in many occasions that they aim at growing supply in line with market demand and to focus on profitability rather than market share. In addition, Micron’s CEO Sanjay Mehrotra receives 76% of his remuneration as long-term incentives, split into one half performance RSUs and the other half time-based RSUs. The performance RSUs focus on percentage of sales as high value solutions (35%), FCF (40%), valuation (25%). The time RSUs vest ratably over 3 years. I believe that these incentives, focusing on FCF and share price align Mehrotra’s interests with those of his shareholders – which is increasing cash flows and value and not to engage in a war for market share. Mehrotra also holds ca. $25mn worth of Micron stock and hasn’t sold any stocks since he joined the firm.

Samsung could also behave more rationally as they have also changed their rhetoric from aiming to “outgrow the market” up until 2015 to “bit growth aligned with the market“ ever since 2016 and “strengthening the sustainable profit base rather than focusing on increasing market share” as mentioned in the 2019 Q3 transcript. Additionally, the three Samsung CEOs have all their long-term (3-year) incentives based on ROE, EBIT margin and stock price development as well as qualitative criteria, which are not defined in the annual report. Focus on ROE and margin should theoretically foster rational capex behaviour from Samsung (which is the biggest threat to DRAM industry profitability).

Since SK Hynix does not publish any transcripts, information about the company is relatively scarce. It can however be observed that the estimated 2020 capex reduction from SK Hynix is the largest in the DRAM industry (-47% vs. 2018 and -38% vs. 2019).

So it seems that there would be several “nudges” pointing towards a more rational capex behavior in the DRAM industry. Next to the more rational capex behavior, there are also a few additional points, which support the thesis that the memory industry has a brighter future ahead.

I mentioned that new node transitions are becoming more complex and therefore the cost reduction and bit growth per node transition are becoming smaller. This dynamic should also lead to reduced cyclicality as previously a memory manufacturer could potentially increase the output by 20% by transitioning over to a new node, while today it might be only 10%. This means that new node transitions will likely have a limiting impact on excess supply and also mute the cyclicality of the industry.

Another supporting factor is the very slow, but steady move away from a pure commodity to more specialized products. All three DRAM players are promoting their value-add solutions, e.g., through pre-packaging NAND with DRAM into fixed modules or to tailor their products to specific needs of different end-customer groups such as mobile with low-energy needs or cloud with highest data integrity. While this process might take time, it is also a (small) driver towards a less cyclical memory industry.

All these factors do not guarantee a turning of the cycle, however, they all point in the same direction – towards recovery. Combine these “supply-constraining” tendencies with the here not discussed demand growth from 5G, cloud, AI, IoT and autonomous driving and you get (at least in my opinion) a very attractive industry dynamic.

Valuation

Many investors try to consider industry cycles in their investment decisions – this is the reason why an industry low does not always coincide with a stock price low. Therefore, only identifying the current situation and anticipating further stages in the cycle is not enough. One needs also to consider the current market price in order to arrive at an investment decision.

Personally, I think valuing cyclical industries is very challenging and you can only get very rough approximations to the real value of a company. That’s why I’ll also use a rough valuation approach for Micron.

Taking today’s market cap of $48.6bn and using the average of 2017 and 2019 (as a proxy for mid-cycle earnings power) net income or FCF results in a P/E of 8.3 or P/FCF of 14.3. Since in the memory market capex usually exceeds depreciation I think P/E is a too optimistic measure, while P/FCF is probably too pessimistic as it does not account for growth capex in such a high-growth industry.

So the true earnings power might lie somewhere between net income and FCF and consequently the current multiple for mid-cycle earnings might be somewhere between 8.3 and 14.3. If we take the midpoint of 11.3, I believe that this is a very attractive valuation for a company with high returns on capital and a long runway for growth. I do also believe that the market usually overreacts to peaks and troughs, which makes it even more attractive to buy close to the current trough since the next peak will most likely come and chances are that the market will also overreact then on the upside.

Risks

In my perspective, excessive industry capex is the biggest threat to this investment thesis in the coming 3 years. While China is attempting to build a domestic memory industry, they are in DRAM still around 2 years technologically behind and very small (<7% of Micron's total wafer capacity). Additional risks could be of political nature (US vs. China conflict), technological nature (failure in node progression) or legal nature (lawsuit on price-fixing). While these risks all need to be monitored closely, I don’t see them as a current threat to this investment thesis.

Summary

I am very aware that there are numerous additional points to discuss on Micron, my key goal was however to show it primarily from a “more rational capex scenario” perspective and not to illuminate all available topics on the company or industry.

This investment thesis is based on the belief that we’re currently close to a cycle low and that in the next 3-5 years the likelihood of an upswing is more likely than a further industry decline. The main supporting arguments for this belief are rational capex behavior from the 3 large DRAM competitors. While it is impossible to make an exact forecast of the memory cycle, there are several factors pointing towards a recovery. Lastly, Micron seems attractively valued at mid-cycle margins and potentially has a long growth runway ahead.

Disclosure: I am/we are long MU. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Gloss