Marvell Technology: Overvalued Now (NASDAQ:MRVL)

Marvell Technology Group (NASDAQ:MRVL) has reached an all-time high at $36.60 per share, along with overall stock market bullish momentum. With high goodwill and intangibles, rising debt level, and high valuation, we think Marvell is overvalued now.

High level of goodwill and intangibles from acquisitions

Marvell Technology is the provider of infrastructure semiconductor solutions, with two main business components, including Storage and Networking, in a single operating segment. Previously, Marvell has a relatively concentrated customer base. In 2018, three most significant customers, Western Digital (NASDAQ:WDC), Toshiba (OTCPK:TOSBF), and Seagate (NASDAQ:STX), accounted for 33% of total revenue. In 2019, the customer concentration issue has improved, as each of those three customers accounted for less than 10% of the entire company's sales. There was only one distributor, Wintech, which contributed 12% of total revenue in 2019.

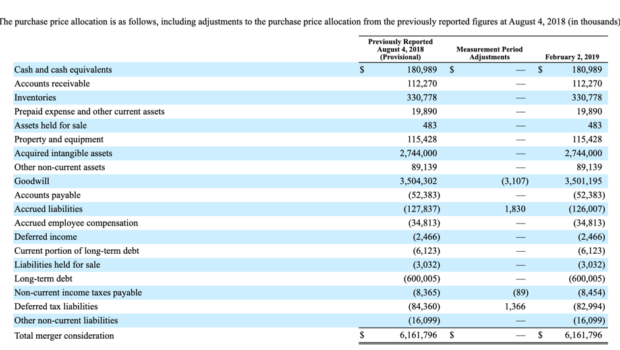

What makes us worry is the company's high level of goodwill and intangibles. As of May 2020, Marvell had roughly $8 billion in goodwill and intangibles, accounting for 72.8% of its total assets. The goodwill of $5.3 billion resulted from acquisitions over the years. In 2018, Marvell purchased Cavium, the supplier of highly integrated semiconductor processors, with a total consideration of more than $6.16 billion, including $3.5 billion in goodwill and $2.7 billion in intangible assets.

Source: Marvell's 10-K filing

While this business combination seemed to be strategic and beneficial for both companies regarding products & R&D synergies, the valuation seemed to be quite stretched. Cavium had been generating losses consistently. In 2017, it posted only $984 million in revenue, while operating losses came in at nearly $56.7 million. Thus, a $6.16 billion price tag valued Cavium at as much as 6.26x revenue. In 2019, Marvell also spent roughly $1 billion to acquire Aquantia, the high-speed transceiver manufacturer, and Avera, the ASIC semiconductor solutions provider.

In the first quarter of 2020, Marvell's revenue increased by 4.7% to $639.6 million, driven by the acquisitions of Avera and Aquantia. The cost of goods sold, however, jumped by 21.8% year over year to $366.7 million, due to the amortization of intangible assets and inventory fair value from those two acquisitions. The operating losses have expanded from $21.1 million in the first quarter last year to nearly $96 million in the first quarter this year. The operating results were expected to improve in the second quarter, with a revenue estimate of $684 million-$756 million and an EPS estimate of $0.17-$0.23. However, if any of these acquired businesses turns out not to be as previously expected, goodwill would need to be impaired, hurting the bottom line.

Increasing debt level to finance acquisitions

Because some of the acquisitions were financed through debt, Marvell's debt level has been rising over time. Marvell has gone from a debt-free company in 2017 to a net-debt company at the time of writing. As of May 2020, Marvell had $667.5 million in cash and $1.44 billion in long-term debt. Thus, the net debt came in at $772.5 million. However, the debt maturities spread out from 2022 to 2028.

Source: Marvell's 10-Q filing

The earliest debt due was in 2022, with $450 million in principal. With a three-year average operating cash flow of $509 million, we believe that Marvell can comfortably pay down the current debt outstanding.

It is overvalued now

Because of the overall bullish market sentiment, Marvell's share price has reached an all-time high at $36.60 per share, with an enterprise value of $25.4 billion. Compared to its competitors, including Xilinx (NASDAQ:XLNX) and STMicroelectronics (NYSE:STM), Marvell is the most expensive.

Source: YCharts

Source: YCharts

Marvell's forward EV/EBITDA is the highest at 32x, while Xilinx and STMicroelectronics are trading at much lower valuations at 27x and 15.6x forward EV/EBITDA respectively.

In 2021, it is estimated that Marvell could generate $3.5 billion in revenue and nearly $1.17 billion in EBITDA. If we expect the company is valued at a five-year average EV/EBITDA of 16.7x, Marvell should be worth only $19.5 billion in enterprise value, 23% lower from the current trading price.

The high valuation does not mean Marvell's share price could not go higher. The rising demand for 5G and data center solutions could have positive market momentum on Marvell's share price. However, the higher the price its stock reaches, the riskier it is for investors.

Conclusions

Marvell has taken more debt to finance its high-priced acquisitions. With a high level of goodwill, increasing debt level, and high valuation, we expect short-term pressure in its current high stock price.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Gloss