Dropbox: Focusing On Value In Technology (NASDAQ:DBX)

funky-data/iStock Unreleased via Getty Images

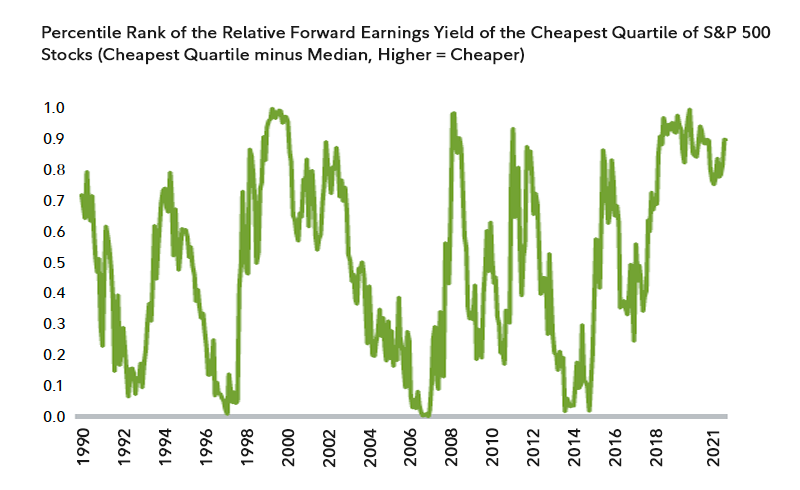

From a market strategy standpoint, I continue to favor value over growth because lower multiple stocks remain extraordinarily inexpensive compared to their very pricey counterparts on a historical basis. The chart below shows that the least expensive quartile of the S&P 500 is at a near record high discount to the median stock on the basis of earnings yield. The earnings yield is the reciprocal of the price-to-earnings ratio, which means it is calculated by dividing expected earnings (forward) by the stock price. The higher the yield, the cheaper the stock.

Fidelity

Focusing on value does not necessarily mean one must confine holdings to specific sectors, as value can be found in every sector of the S&P 500 to varying degrees. My goal is to find those values in a way that allows me to diversify my stock holdings across all sectors of the market.

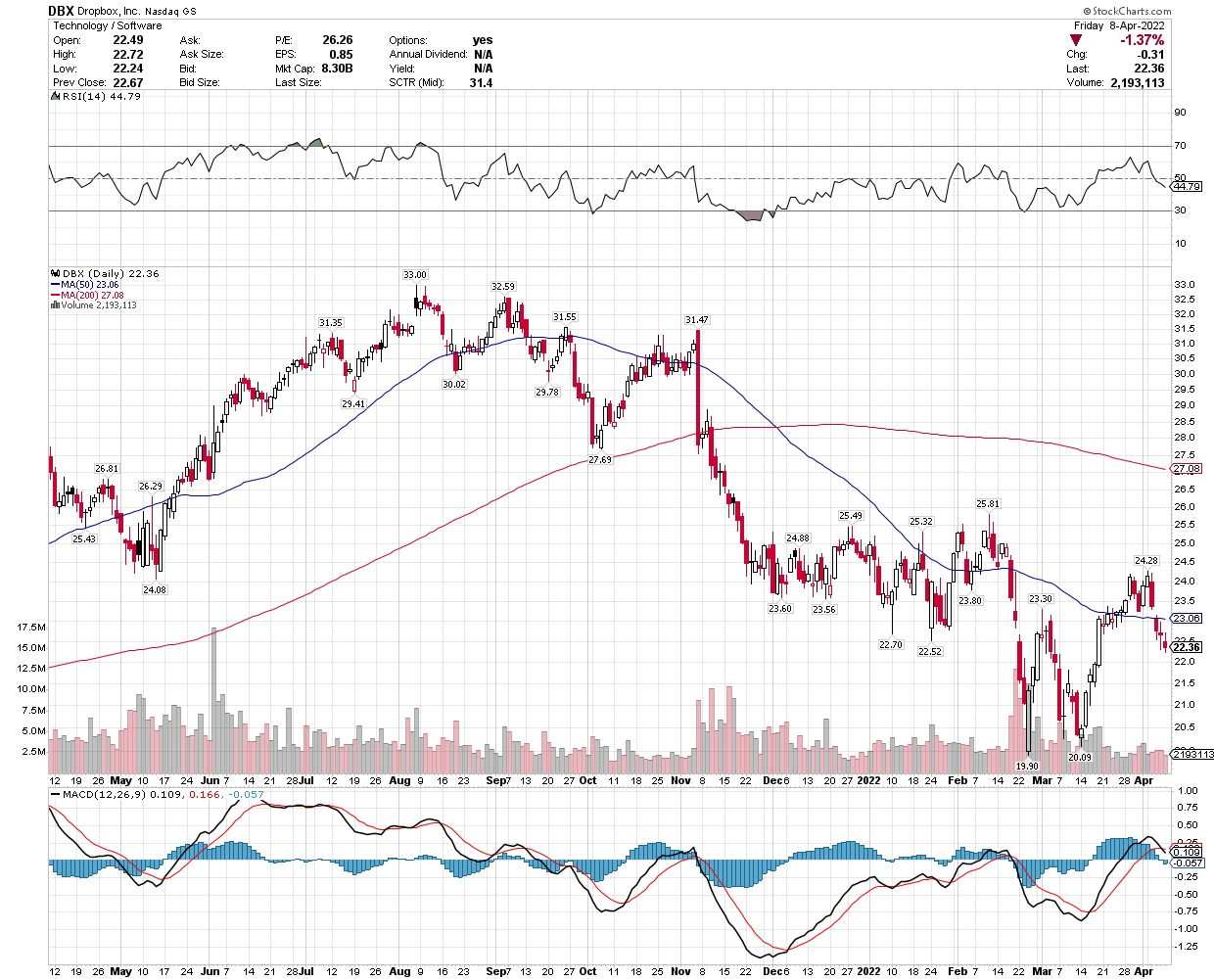

With respect to the technology sector, I view Dropbox (NASDAQ:DBX) as a prime example of a value-oriented name that still has plenty of growth potential in a very difficult macroeconomic environment. This file sharing and cloud collaboration company primarily serves business groups or teams who want to view, share, store, edit, and sign documents. It has been gradually transitioning a registered user base of more than 700 million for its free offerings to a paying subscriber platform with more features that now totals 16.8 million. The subscriber base along with annual recurring revenue is growing at approximately 10%, while average revenue per user is also showing steady incremental growth. All of these metrics are moving in the right direction for a company focused on productivity improvements for its customers.

Dropbox

The story gets better when we look at the financial metrics, as the shares trade at 4 times sales and less than 14 times this year’s consensus earnings estimate of $1.62, which is an estimate that has been increasing since the beginning of the year. That gives it an earnings yield of 7.3%, which compares favorably to the S&P 500 earnings yield of 5%.

Seeking Alpha

The balance sheet is exceptionally strong with approximately $650 million in net debt for this $8.4 billion market cap, and management has been buying back shares with what was more than $700 million in free cash flow last year, resulting in a free cash flow (FCF) yield of approximately 8%. The total common shares outstanding has declined from 414 to 381 million last year. According to its most recent quarterly results, management is targeting $1 billion in free cash flow by 2024, and I do not think there is any better metric for identifying quality and value.

The stock has suffered since last fall from guilt by association with the software-as-a-service (SaaS) sector, but it stands apart based on its operational performance to date. The outlook remains strong as it has a substantial free-user base from which it can continue to grow. Its cheap valuation, solid balance sheet, and strong free cash flow should put a floor under these shares near current levels. As the rate of economic growth slows and earnings growth for the broad market wanes, these shares should command a higher multiple, which is why Dropbox is one of my favorite value names in the technology sector.

StockCharts

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Gloss