Cognizant Technology Solutions Has Solved Its Margin Worries (NASDAQ:CTSH)

JHVEPhoto/iStock Editorial via Getty Images

Recent trading weeks have been a massacre for tech companies due to valuation worries, with many undoubtedly seeing fear-driven drops. Cognizant Technology Solutions (NASDAQ:CTSH) is one of the leading organizations in the Information Technology industry and one of the companies that has witnessed a substantial decline over the past ten trading weeks. CTSH continues to have a strong competitive advantage in the market, as seen by their rising top line and supported by rising bookings and FCF.

CTSH's efforts to control its margin through currency hedging appear to be successful, since the company's Q1 2022 operating margin is almost flat to that of Q1 2021. Contrary to what many investors believe about falling margins in the current climate of rising inflation, CTSH's management provided investors with a reassuring outlook for FY22, with their operating margin expanding.

As of the time of writing, CTSH remains profitable and liquid, making it a worthwhile investment despite today's fear-driven drop.

Company Background

Cognizant is a corporation that offers a variety of digital transformation services to businesses and is included in the Fortune 500 companies. To mention a few industries they serve, it is well-known for its banking and healthcare solutions. The company has been transforming its consumers through digitalization for more than 28 years and, as of this writing, still possesses a tremendous growth potential.

One of its long-term objectives is to become the world's premier digital partner for the whole C-suite. The company boasts revenue growth through successful acquisitions, strengthening its capabilities and global delivery footprint with its growing employee count of 340,400 this Q1 2022, up from 296,500 the same quarter last year.

On the other hand, as a global service provider, CTSH should acknowledge the need of investing in its human resources. This quarter, the company's annualized attrition rate (the rate at which employees leave the company) jumped to 30.8% from 21.0% in Q4 2021, a statistic that is cause for alarm. This could result in dissatisfied customers, which could hinder the company's growing projected top line.

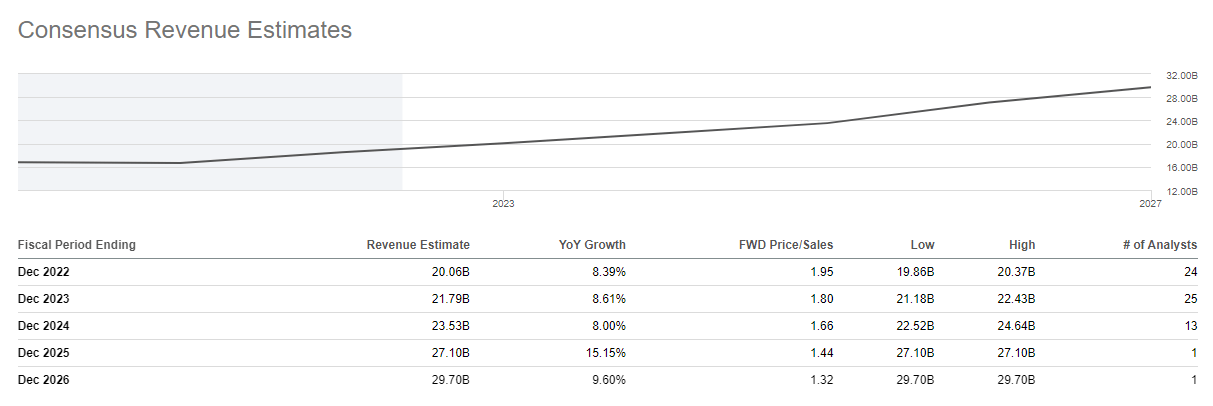

CTSH: Growing Top Line Forecast Amid Slowing Global Economy (SeekingAlpha.com)

Strong Booking And Healthy Demand Outlook

This quarter, CTSH's topline totaled $4,826 million, up from $4,401 million in the first quarter of 2021. In addition, based on the company's revenue growth trend, this quarter saw a YoY growth of 9.66%, better than the 4.17% recorded in Q1 2021. This is due to its robust digital business activities, which account for 50% of the company's overall revenue this quarter, up from 44% in the same period previous year.

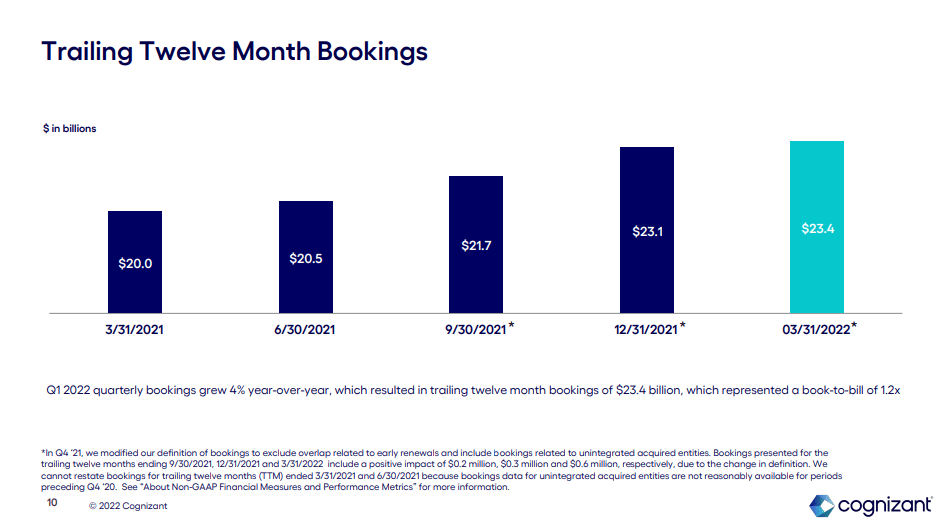

CTSH: Growing Booking and Improving Book to bill ratio (Q1 2022 Investor Presentation)

This resulted in a more efficient CTSH, as seen by their rising bookings and improved book-to-bill ratio of 1.2x, up from 1.1x in the same quarter of the previous year. In addition to this catalyst, the management presented a positive outlook for the company's demand environment.

…I remain optimistic about IT services industry demand for the foreseeable future. Clients are making the shift to digital operating models to become more agile, automated and innovative. They know that it is the only way to deliver customer-centric user experience and hyper personalization, to simplify complex workflows and to build a modern operating infrastructure that's

Our strategic repositioning enables us to engage more deeply with clients, helping them to succeed and supports our growth trajectory. Our capabilities are in strong demand as digital becomes mainstream. Source: Q1 2022 Earnings Call Transcript

Strong Guidance

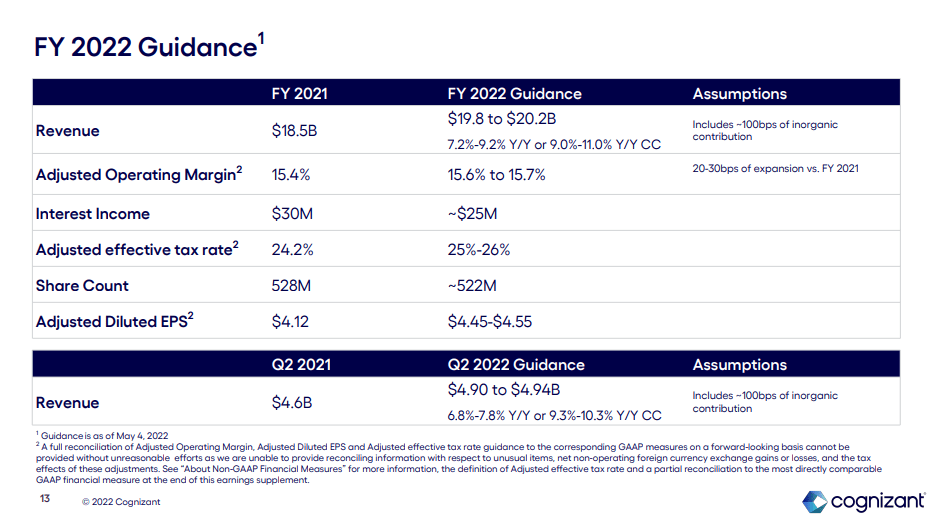

CTSH: Positive Outlook at Today's Uncertainties (Q1 2022 Investor Presentation)

CTSH's management has successfully allayed my apprehensions about investing in the company, thanks to its expanding operating margin outlook and lack of a meaningful impact on its top line from the present Russia and Ukraine crisis.

Better At A Lower Price

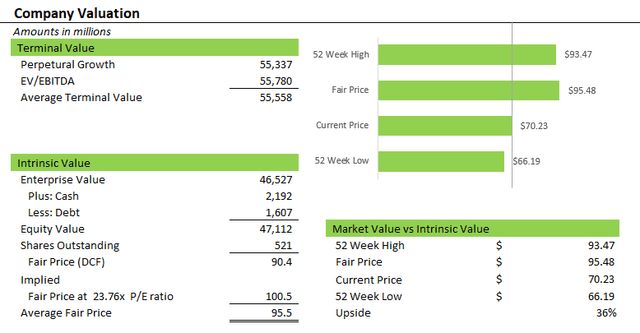

CTSH: Company Valuation (Prepared by InvestOhTrader)

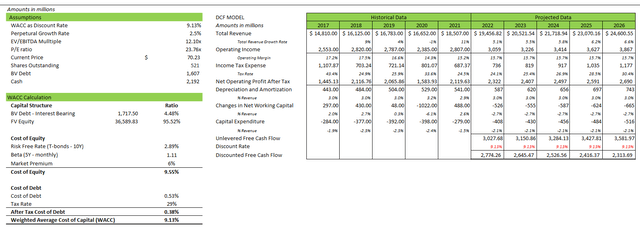

The drop resets its valuation, but not its fundamentals. Using a WACC of 9.13% as our discount rate, I determined a fair price of $95.5 with an upside potential of 36%. Nonetheless, I believe CTSH will surpass the analysts' high-range price forecast of $103 within the next five years, especially considering its forward P/E of 16.64x, which is significantly cheaper than its trailing P/E of 18.01x and its 5-year average of 23.76x.

CTSH: DCF Model (Data from Seeking Alpha and Yahoo! Finance. Prepared by InvestOhTrader)

I used the analysts' projection to complete my DCF model. I maintained a 15.7% operating margin all throughout the projected years. I believe this model is quite conservative especially with CTSH's growing digital presence and its strong acquisition record potentially resulting in a positive growth, which is not included in our assumption today.

Q1 2022 Financial Performance Update

-

Not only did CTSH post strong quarterly results, but based on its growing trailing total revenue of $18,932 million, which is up from $18,502 million recorded in FY2021 and higher than the $16,652 million recorded in the previous two fiscal years, it is evident that CTSH is capitalizing on its vast addressable market.

-

CTSH had a larger gross profit in the first quarter of 2022, totaling $1,729.00 million compared to $1,637.00 million in the first quarter of 2021. However, the company's gross margin decreased to 35.83% in Q1 2022, from 37.20% in Q4 2021. This is a result of the company's increasing human resource capital resulting in a growing compensation expense.

-

Comparable to the previous bullet point, the company's operational income increased from $666 million in the previous quarter last year to $727 million this quarter. However, looking at a percentage basis, this resulted in a declining operating margin of 15.06%, compared to 15.13% in the same quarter the previous year.

-

CTSH's net income grew to $563 million from $505 million in the first quarter of 2021, which is where things get interesting. This resulted in an increase in its net margin from 11.47% in Q1 2021 to 11.67% this quarter.

-

This snowballed to a growing EPS of $1.07 this quarter, up from $0.95 in the same quarter last year. Furthermore, the company's trailing EPS generated $4.18 and is up compared to its $4.06 last fiscal year and $2.58 recorded in FY2020.

Weekly Chart Looks Good: Buy The Dip

CTSH: Weekly Chart (TradingView.com)

Based on today's price action, we can conclude that CTSH is trading near its swing low in July 2021 and near its 200-day simple moving average. Before retesting its 52-week high of $93.47, I foresee a continuation of consolidation in the current area. Considering the stock's 20-day and 50-day simple moving averages, it appears to be extending its bearish trend, which could cause its price to breach its initial trend line support depicted in the preceding chart. If so, I feel that $66 will serve as our next support, and I am willing to average down to $60. This simulates the 30% drop that occurred during the peak of the pandemic owing to panic selling.

Key Takeaways

Before I forget to mention it, CTSH has increased its dividend for four years in a row and has a dividend yield of 1.44% at today's pricing, giving investors more reason to hold or rather add to its potential drop. With its increasing free cash flow of $2,309 million and FCF margin of 12.2%, as well as its improving liquidity, I believe CTSH will be able to sustain its expanding dividend payments.

Upon further investigation of its liquidity, I discovered that its debt/EBITDA ratio of 0.47x is an improvement above the 0.49x and 0.61x ratios recorded in FY2021 and FY2020, respectively. Additionally, its debt-to-equity ratio reflects the same trend and improved to 0.13x in the most recent quarter. This is a result of its declining total debt of $1,607 million, which precipitated an improvement in its interest coverage ratio to 318.67x.

CTSH is one of the companies currently repurchasing their own shares, and the reauthorization of its $1.7 billion share repurchase program might be a favorable event for investors to track.

Cognizant has a controlled margin, remains liquid, generates a substantial amount of cash flow, and trades with growing addressable industries. This makes the stock valuable at its current price and even more so at its potential drop.

Thank you for reading and good luck!

Gloss