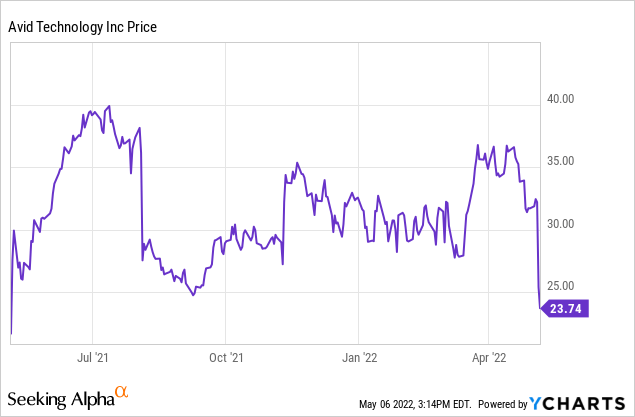

Avid Technology Stock: Sell Off After Earnings Is Unjustified (NASDAQ:AVID)

wundervisuals/E+ via Getty Images

Investment Thesis

Avid (NASDAQ:AVID) is a US-based company that provides audio and video technology from editing software and composing hardware. In 2018, The company started changing its pricing model from a perpetual-based model to a subscription-based model ((SaaS)). This has resulted in a huge success which significantly increased its gross margin and EPS (earnings per share). The company recently reported its Q1 2022 earnings and the stock plummeted 20% as Q2 guidance came below analysts' estimates. However, subscription revenue still increased by over 30%, and full-year guidance remained unchanged. I believe this is an overreaction and creates a good buying opportunity for investors.

Introduction

Avid’s main product includes Pro Tools and Media Composer. Pro Tools is a music and audio production software. On the music end, it allows artists to make beats, write songs, record vocals and instruments, and mix studio-quality music. On the audio end, it allows production teams to record, edit, mix and deliver sound for film, TV, video games, and more. Media Composer is a video editing software with features such as remote collaboration. It allows video professionals to create movies and tv series much more efficiently. Avid also sells hardware that supports the software such as sound mixers, storage platforms, etc.

The demand for these products has increased substantially in the past few years and I believe the trend will continue. This is due to the ongoing increase in production for tv-series, films, and music. The streaming war continues to heat up with Disney, HBO, Peacock, Paramount, and more joining. This resulted in a huge boost in demand as all these companies are trying to produce more content to contend with each other. I believe this will continue to provide tailwinds for Avid. According to Statista, The SVoD (subscription video on demand) market is projected to grow from $82.43 billion this year to $115.90 billion in 2026, representing a CAGR of 8.9%.

Demand for music production software has also ramped up a lot in recent years. This is due to the increasing popularity of music streaming platforms such as Spotify and Soundcloud. These platforms allow independent and less famous musicians to upload their music easily and earn royalties, which resulted in a huge increase in music production as more musicians are looking to enter the industry with entry barriers lowering.

First Quarter Earnings

In the first quarter of 2022, the company reported a revenue of $100.6 million, a 6% increase compared to $94.4 million a year ago. Subscription revenue increased 32.5% year over year while Integrated Solutions, Perpetual and P/S Revenue declined 0.7%. Gross margins remain flat at 66.3%. Adjusted EBITDA was $19.3 million, an increase of 9.0% year-over-year. Adjusted EBITDA Margin was 19.2%, an increase of 50 basis points year-over-year. Non-GAAP EPS was $0.33 compared to $0.28 a year ago, representing a 17.9% growth. It reported a positive operating and free cash flow of $7.9 million and $4.7 million respectively. The company guided Q2 revenue to be at $92.0 -$104 million, with Adjusted EBITDA of $13.5-$19.5 million, and Non-GAAP EPS of $0.19-$0.32. For FY22 the company guided revenue of $430 -$450 million, with Adjusted EBITDA of $84 -$94, free cash flow of $60-$67 million, and Non-GAAP EPS of $1.40 -$1.51. The soft revenue growth is partly due to global supply chain issues which caused a tightening of supply for several components, which impacted their ability to meet customer orders. I believe this is a temporary issue that will ease over time.

Jeff Rosica, CEO, in the press release

The global supply chain continues to present challenges, which could cause some uneven quarterly performance in the near term. We currently believe these challenges to be temporary, and remain confident in our growing subscription and healthy maintenance business and in our ability to meet our 2022 targets. We’ve recently introduced several exciting new product enhancements for Pro Tools, Media Composer and MediaCentral, and in April, we added new pricing tiers for Pro Tools entry-level and high-end users, as we continue to execute on our subscription growth strategy.”

The company’s balance sheet also remains healthy with a $41M cash balance and $111M available liquidity including an undrawn revolver. Net Leverage ratio (Net Debt / LTM Adjusted EBITDA) improved from 2.6 to 2.2 this year. It is also worth noting that the company has a share repurchase authorization in place announced back in September last year that allows them to buy back $100 million worth of shares. They bought back $10.8 million in the first quarter therefore $102.4 million is still in place.

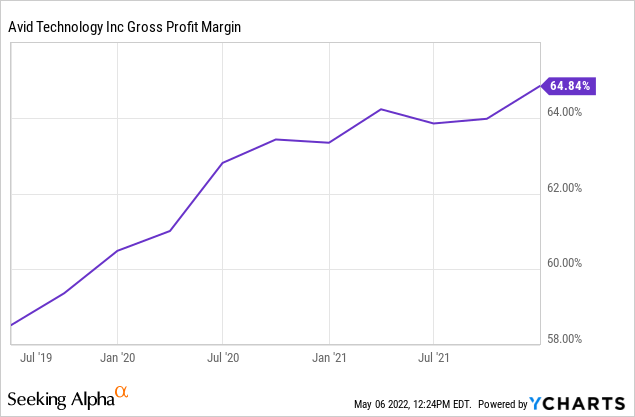

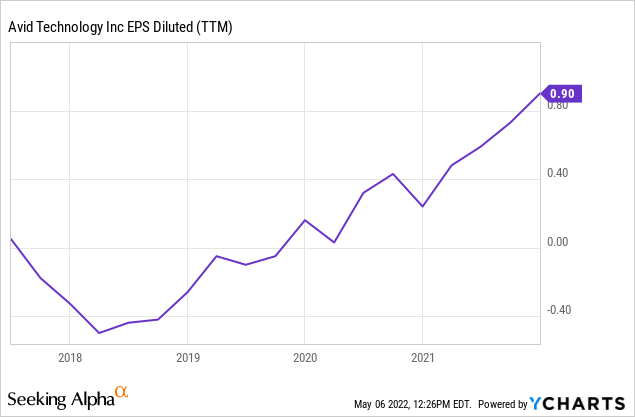

Despite the market’s reaction, the results are definitely not bad in my opinion. If you look deeper, subscription revenue actually increased 32.5% year over year to $33 million, now representing around 33% of total revenue. Cloud-enabled software subscriptions (Pro Tools + Media Composer + Sibelius + MediaCentral) also saw a nice increase, subscribers are now standing at 432,000 compared to 348,000 last year, representing a 24.1% growth. Profitability is increasing with adjusted EBITDA margin now at 19.2% and is forecasted to keep growing as the SaaS transition continues. In the graph below, you can see that since its transition to the SaaS model, its gross profit margin and EPS have been improving quickly. Non-GAAP EPS is forecasted to increase to $1.40-$1.51 this year according to management guidance.

Valuation

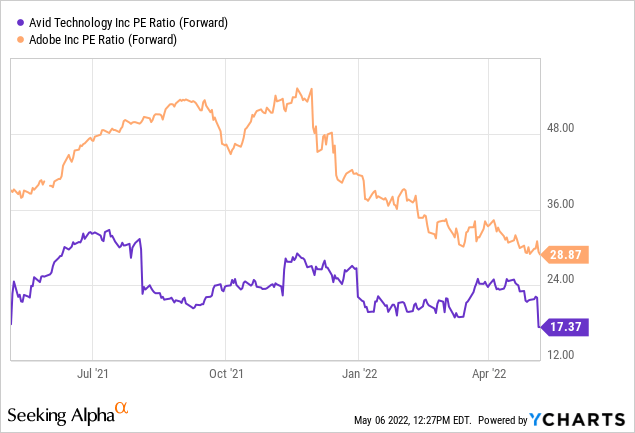

After the drop, the company is trading at a FWD PE ratio of 17.4. This is definitely a compelling valuation for a company growing bottom line in the mid-teens and subscription revenue at 30+%. Not to mention subscription revenue only accounts for around 33% of its revenue so growth should be able to continue looking ahead. Another company that focuses on editing and creation software is Adobe (ADBE). As you can see from the chart below, Adobe is currently trading at an FWD PE ratio of 28.9, which represents a 66% premium. Both companies have a similar bottom-line growth rate as well. A premium should be given to Adobe as it is a lot more established with much wider product offerings, however, I believe the premium should be lower. XLK (Technology Select Sector SPDR ETF) consists of most tech companies and is a good benchmark for technology stocks. It currently has a PE ratio of 25.4 with an estimated 3–5 year EPS growth of 15.5%, which is similar to Avid’s growth rate. If we use XLK as a benchmark and apply its PE ratio to Avid, it gives Avid’s stock a 46% upside from current levels.

Supply Chain and Inflation

The current biggest risk in my opinion is the supply chain blockage. As management mentioned, the company has been seeing a tightening of supply for several components for its audio integrated solutions at the end of the first quarter. Which impacted its ability to meet customer orders, resulting in first-quarter revenue being at the lower end of the guidance. However, I am optimistic that supply chain conditions will start to ease throughout the year as China’s COVID condition improves. Inflation is less of a problem for the company as its solutions are very essential to production teams and musicians. Streaming companies are going to continue to ramp up their video production as competition increases. In Netflix’s latest earnings call, the company said that they will be doubling down on content creation.

Conclusion

In conclusion, I believe this drop is overblown and it is now trading at a discounted valuation when compared to similar companies like Adobe. The guidance for the second quarter missed analyst expectations but this is largely due to temporary supply chain issues which I believe will be resolved through the year. Full-year guidance remains intact which shows that the management team believes the company will have a stronger performance in 2H despite a soft 1H. The transition to a SaaS model is still going full steam ahead with subscription revenue increasing 32.5% year over year and subscribers increasing 24.1%. Cash flow and margins are expected to improve as subscription revenues start to account for a larger portion of total revenue. SVOD continues to provide a strong tailwind as more and more companies enter the streaming war, which fuels the demand for content creation software. I believe there is still a long growth trajectory ahead for Avid and the current valuation is compelling which presents a good buying opportunity for investors.

Gloss