Alkami Technology Grows Revenue But Operating Losses Mount (NASDAQ:ALKT)

cofotoisme/iStock via Getty Images

A Quick Take On Alkami Technology

Alkami Technology, Inc. (NASDAQ:ALKT) went public in April 2021, raising approximately $180 million in gross proceeds in an IPO that priced at $30.00 per share.

The firm provides cloud-based digital banking software to financial institutions in the United States.

Until management can show a credible path to operating breakeven, my near-term outlook for ALKT is a Hold.

Alkami Overview

Plano, Texas-based Alkami was founded to develop a platform that improves financial institution user interfaces and integrates with various banking functions and processing systems.

Management is headed by president and CEO Alex Shootman, who has been with the firm since November 2021 and was previously CEO of Workfront, an enterprise application platform and before that, was President of Apptio.

The company’s primary offerings include:

-

User experience

-

Integrations

-

Data insights

The firm pursues client relationships with community, regional, and super-regional financial institutions via a direct sales and marketing approach.

ALKT says that its typical sales cycle is from 3 to 12 months and a subsequent implementation time range of 6 to 12 months.

Alkami’s Market & Competition

According to a 2020 market research report by Grand View Research, the global market for core banking software was an estimated $9.4 billion in 2019 and is expected to reach $17 billion by 2027.

This represents a forecast CAGR of 7.5% from 2020 to 2027.

The main drivers for this expected growth are a growing demand from customers for advanced banking solutions across numerous touch points and devices.

Also, the U.S. core banking software market history and projected future growth trajectory is shown in the chart below:

U.S Core Banking Software Market (Grand View Research)

Major competitive or other industry participants include:

-

NCR Corporation

-

Q2 Holdings

-

Temenos AG

-

Fiserv

-

Jack Henry and Associates

-

Fidelity National Information Services

Alkami’s Recent Financial Performance

-

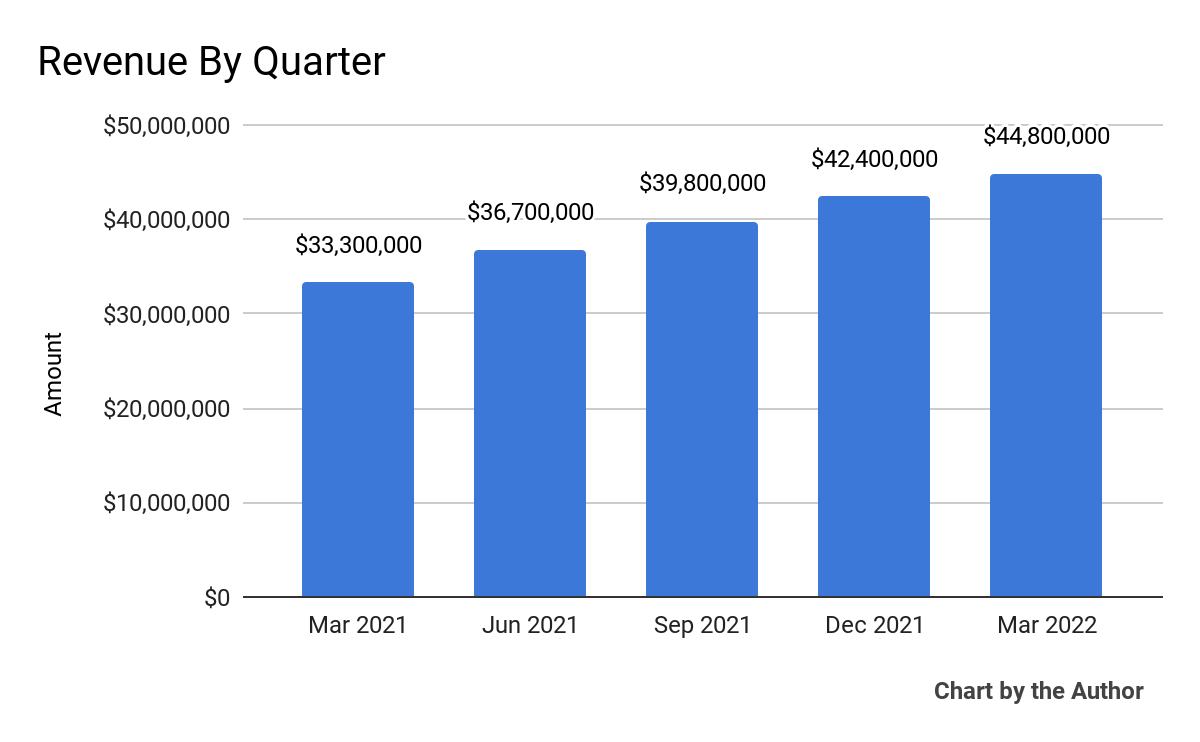

Topline revenue by quarter has grown consistently over the past 5 quarters:

5 Quarter Total Revenue (Seeking Alpha and The Author)

-

Gross profit by quarter has also grown in a similar manner as total revenue:

5 Quarter Gross Profit (Seeking Alpha and The Author)

-

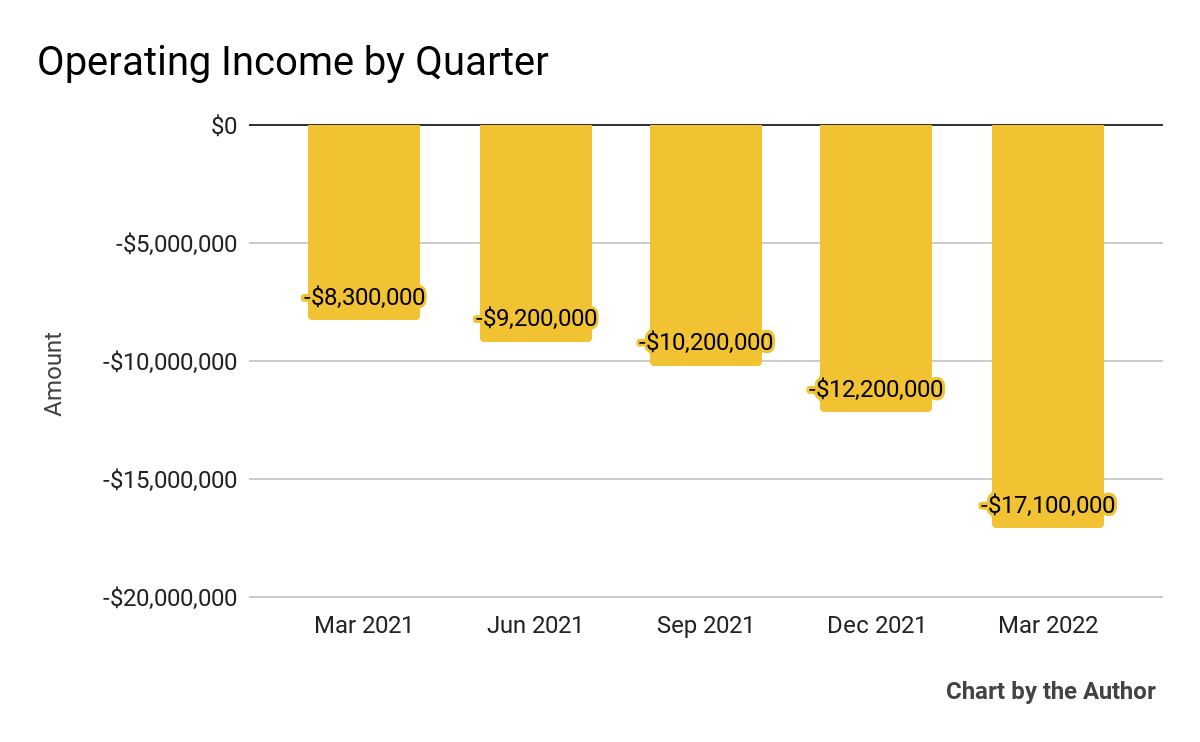

Operating losses by quarter have worsened dramatically, with no apparent path to operating breakeven any time soon:

5 Quarter Operating Income (Seeking Alpha and The Author)

-

Earnings per share (Diluted) have remained negative:

5 Quarter Earnings Per Share (Seeking Alpha and The Author)

(Source data for above GAAP financial charts)

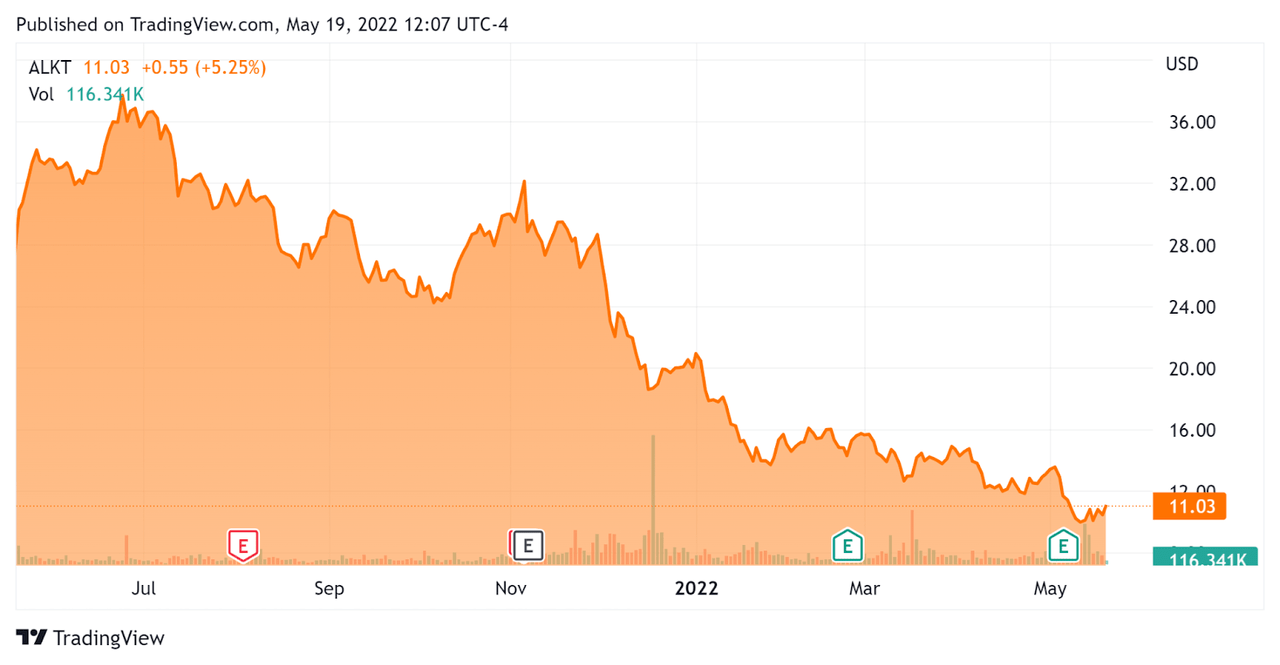

In the past 12 months, ALKT’s stock price has dropped 59 percent vs. the U.S. S&P 500 index’s fall of 4.6 percent, as the chart below indicates:

52 Week Stock Price (Seeking Alpha)

Valuation Metrics For Alkami

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure |

Amount |

|

Market Capitalization |

$914,650,000 |

|

Enterprise Value |

$673,160,000 |

|

Price / Sales |

5.48 |

|

Enterprise Value / Sales |

4.11 |

|

Enterprise Value / EBITDA |

-15.21 |

|

Operating Cash Flow [TTM] |

-$35,300,000 |

|

Revenue Growth Rate [TTM] |

33.96% |

|

Earnings Per Share |

-$0.58 |

(Source)

Commentary On Alkami

In its last earnings call (transcript), covering Q1 2022’s results, management highlighted the pending release of a new mobile platform that provides its customers with better customization and expansion opportunities.

Additionally, the acquisition of Segmint will enable the firm to provide data-driven marketing strategy and analytics capabilities.

With this and other recent deals, Alkami CEO Shootman believes the company "can now offer a complete solution for every stage of the end customer life cycle, from account opening to servicing and engagement to cross-sell and back to account opening."

The potential from these additions promises to open up its total addressable market ("TAM") by another $1 billion, according to management.

As to its financial results, Q1 2022 revenue grew by 35% year-over-year, beating previous revenue guidance.

Non-GAAP gross margin rose to 58% from 55% a year ago, based on scaling and cost efficiencies.

Sales and marketing expenses rose somewhat, while R&D dropped as a percentage of revenue, though R&D remains a high revenue percentage at 27%.

The firm ended Q1 with $209 million of cash and marketable securities against a $9 million net use of cash during the quarter, so ALKT has plenty of runway based on existing cash burn metrics.

Looking ahead, management expects to bring institutions online representing 1.4 million users in 2022.

Regarding valuation, the market is generally hammering SaaS stocks that aren’t at operating breakeven, with ALKT’s EV/Revenue multiple at a very low 4.1x compared to a more typical med-teens multiple.

The primary risk to the company’s outlook is its worsening operating losses with no obvious path to GAAP operating breakeven.

For long-term, patient investors seeking to scoop up a growing SaaS company in the financial institution space, ALKT could be a candidate due to its low valuation.

However, its worsening operating losses are a concern, as the stock market has severely penalized such firms in the current environment.

Accordingly, until management can show a credible path to operating breakeven, my near-term outlook for ALKT is Neutral.

Gloss