A10 Networks Stock: Undervalued Growth With Cybersecurity Tailwind (NYSE:ATEN)

Olemedia/E+ via Getty Images

A10 Networks, Inc. (NYSE:ATEN) was founded in 2004 by Lee Chen (Co-Founder of Foundry Network). The company originally focused on the identity management market, before becoming a leader in the Application Delivery Controller (ADC) industry. An ADC is basically an advanced load balancer, which helps to optimize traffic flow to servers and thus improves performance. Internet traffic has exploded in recent years due to the increasing number of internet-enabled smartphones, cloud applications, and IoT (internet of things) devices. With all this traffic, bottlenecks can occur and security risks are created.

Rising Cybersecurity threats such as distributed denial of service ((DDoS)) attacks aim to overload enterprise servers. Thus, the use of a smart Application Delivery Controllers can "control" the flow of traffic and set limits on requests. According to one study, 5.4 million DDoS attacks were reported in the first half of 2021, this was an 11% jump from the prior year. The average DDoS attack costs a company $20,000-$40,000 per hour (Cox BLUE). Thus it's no surprise the Application Delivery Controllers industry is forecasted to grow at a CAGR of 9.63% until 2026, reaching a $3.78 billion market value.

5G infrastructure is also growing at a meteoric rate of 49.8%, and is expected to reach $80.5 billion by 2028. These high speed networks also create a further need for Application Delivery Controllers to optimize performance for users. A10 Networks was recently named by Gartner as a sample vendor for 5G Network Security. The company also helped to secure the world's first commercial 5G network with South Korea's largest Telecom provider SK Telecom.

Gartner states that

Securing 5G networks is a priority for CSPs and enterprises as the rise of private deployments, vertical applications, cloud architecture and massive IoT connections in 5G creates new vulnerabilities and challenges, such as potential DDoS attack vectors and entry points.

Thus A10 Networks is poised to ride the growth trends in this industry. They have recently beat earnings estimates for Q1 2022, have high gross margins, and the stock is undervalued intrinsically. The "small" size of the company $1.1 billion market cap and earnings growth makes this company a prime candidate for being a "multi bagger." In addition, they pay a dividend of 1.15% and have recently been buying back shares.

Let's dive into the business model, financials, valuation and risks to find out the juicy details.

A10 share price (ycharts)

Secure Business Model

A10 Networks business is divided into three segments:

1. Application Delivery Controllers (ADC)

2. Network Address Translation (NAT)

3. Distributed Denial of Service ((DDoS)) Security

As mentioned prior the company primarily focuses on Application Delivery Controller Products such as their Thunder ADC. This offers advanced server load balancing, web application firewall (WAF), domain name server (DNS) application firewall (DAF), and much more.

A10 Networks (Company Website)

The company's Lightning ADC is a cloud native solution which helps to optimize cloud applications on public, private and hybrid clouds. Products such as these improve security, increase performance and ultimate reduce cost for customers.

High Profile Customers

Despite being a small company ($1 billion market cap), they have an envious list of over 6,800 customers. This includes high profile names such as Uber Technologies (UBER), UCLA, Yahoo Japan, NEC, and major telecom providers such Deutsche Telekom (OTCQX:DTEGY) (OTCQX:DTEGY) (which is the largest telecoms provider in Europe by Revenue and owns T-Mobile).

A popular part of the A10 Networks company is helping companies with Carrier Grade NAT (CGNAT). Basically, every internet-connected device must have an IP address (like a home address) but there is a limited number of IPv4 addresses and thus Network address translation must be done until IPv6 is rolled out. A10 networks helped Uber with a project in this area.

5G Security

In the 5G arena, A10 Networks helped SK telecom (SKM), the largest telecom provider in South Korea, with the rollout and security of the world's first commercial 5G network.

The company was also recognized by Gartner as a Sample Vendor for Transport Layer Security [TLS] decryption. TLS is the successor to SSL (Secure Sockets Layer) - this is the little padlock you see at the top of this website URL to let you know the connection is secure. TLS and SSL both encrypt the data being transmitted, but if data is encrypted, it is very difficult to inspect. That is why we need a decryption tool.

According to Gartner:

As an ever-greater percentage of inbound and outbound traffic is encrypted, security and risk management leaders must consider how to gain visibility into potentially malicious traffic.

Smart Management

A10 Networks founder Lee Chen was replaced by Dhrupad Trivedi in 2019. Trivedi has a Ph.D. in electrical engineering and an MBA from Duke University. He has previously served as executive vice president at Belden and Trapeze Networks.

Growing Financials

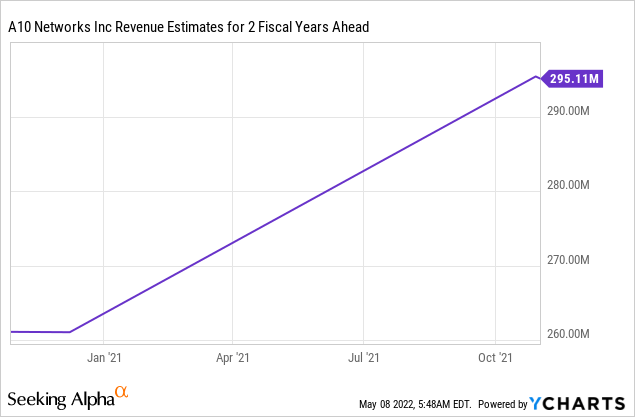

A10 Networks recently beat financial expectations for Q1 2022, they announced revenue of $62.7 million, up 14.3% year over year. Security led product revenue growth was up by 20.1% and the America's grew by 25.5% year over year. The company announced quarterly earnings per share (EPS) of $0.13, which beat consensus estimates of $0.11 per share. In the last four quarters, they beat consensus EPS estimates.

A10 Networks revenue (ycharts)

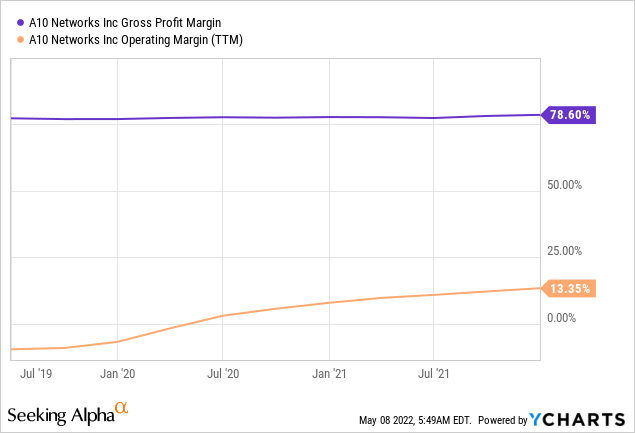

As a software company, they operate with a high gross margin of 79.5% and GAAP net income of $6.3 million, up a meteoric 133% from $2.7 million.

A10 Networks Margins (Ycharts)

The company delivers strong recurring revenue and commands a high 118% retention rate, which was declining prior to the new CEO Trivedi taking over in 2019. Management has a goal to achieve a 120% to 125% retention rate and to add 500 customers each year. If they can pull this off, that leads to some favorable economics.

A10 Networks also has started to pay a dividend of 1.54% which is surprising for a company which is growing but achievable due to their high recurring revenue (80% coming from existing customers). They have a strong balance sheet, with $185 million in cash, $109 million in current liabilities, but virtually no interest bearing debt. Management showed increased confidence with a share buyback of 2.1 million shares ($28.3 million), and the CEO expects full year revenue growth of between 10 and 12% and EBITDA to expand to 26% to 28%.

Valuation

In order to value A10 Networks, I have plugged the latest financial numbers into my discounted cash flow model. I have forecasted revenue to grow at 10% per year for the next 5 years, which is inline with the company's own estimates, but conservative given the growing industry.

A10 Networks Stock Valuation (created by author Ben at Motivation 2 Invest)

As the company's guidance is bullish on increasing profitability. I have predicted the operating margin to expand substantially, to 30% in the next 3 years. I have also capitalized the firm's R&D spend of approximately $54 million in 2021.

A10 Networks Stock Valuation (created by author Ben at Motivation 2 Invest)

Given these figures, I get a fair value of $16 per share. The stock is currently trading at $14.93, and thus is ~8% undervalued.

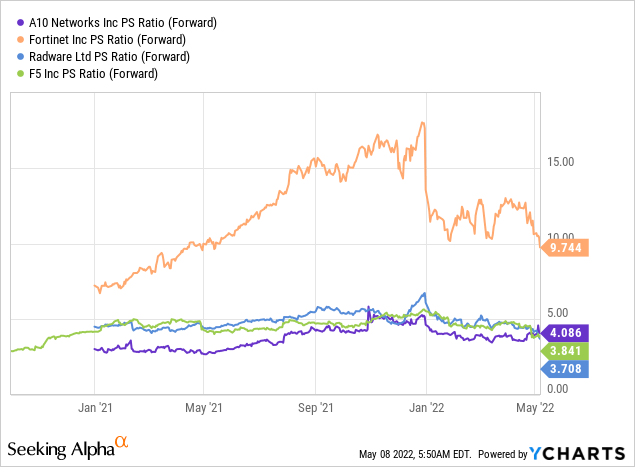

For a relative valuation, I have compared the company's Price to Sales (forward) to other competitors in the ADC industry. The stock currently trades at a PS ratio of 4, which is inline with most competitors. Thus, I would say the stock is "fairly valued" relatively.

Price to Sales Cybersecurity (ycharts)

Risks

Competition

A10 Networks is not the only provider of application delivery controllers. There is immense competition in this industry from established players such as F5, Inc. (FFIV), Barracuda Networks, Citrix Systems (CTXS), Array Networks Inc, Fortinet (FTNT), Radware Ltd (RDWR), and more. Many of these players are much larger and more dominant in the IT industry. Therefore, A10 Networks may find themselves in a David vs Goliath situation, although their product focus could be an advantage.

Insider Selling

A recent review of the most recent insider trades shows a swath of insider selling. CEO Dhrupad Trivedi sold $268,804 in March 2022 at an average price of $12/share (below where the stock trades today. He also sold $81,875 in February 2021, and $219,242 in January 2022. Given his annual compensation is $3.14 million, these are significant sums. Overall, in the past 12 months there have been 46 insider sells and just 4 insider buys. Insiders can sell for a multitude of reasons but still it is not a positive signal overall.

Rising Interest Rates

High Inflation numbers on the CPI (Consumer Price Index) has forced the Fed to raise interest rates. Morgan Stanley predicts at least 6 more rate hikes in the year. Higher interest rates increase the discount rate for stock valuations and compress the valuation multiples of growth stocks especially. As A10 networks is profitable and focused on improving profitability, this may not impact them as severely, but it is still a potential headwind.

Final Thoughts

A10 Networks is a fantastic company with high margins and rapidly growing earnings. Their products have solved many high profile clients' problems, from Uber to Deutsche Telekom. The trends of an increasing number of DDoS attacks, increasing internet usage and the rollout of 5G are key tailwinds for the company. Their help in securing the world's first commercial 5G network with SK telecom is a signal this company has a leading offering in the market.

The company is currently undervalued intrinsically, and thus this could be a great buying opportunity for the long term. The small cap size ($1 billion market cap) makes the company a candidate for a "multi-bagger" in the future. However, there are some risks such as high competition in the market, rising interest rates, and the insider selling.

Gloss