A10 Networks: Bullish Cybersecurity Momentum, Dividend Growth (NYSE:ATEN)

Laurence Dutton

A10 Networks Inc (NYSE:ATEN) offers networking solutions with a focus on infrastructure security across cloud, on-premise, and hybrid environments. Customers including telecom service providers, government agencies, and enterprises integrate the tools from A10 Networks to enhance the safety and efficiency of critical applications.

The setup here is impressive growth with the company expanding its service offerings. Indeed, A10 recently reported its latest quarterly results highlighted by a record operating income and firming margins despite the more challenging macro backdrop. It's also notable that the company also hiked its quarterly dividend by 20%.

The stock has outperformed this year including a sharp rally in recent months supported by the solid outlook with demand from various industries expected to continue. We like the stock for its high-quality growth profile within tech and believe shares have more upside going forward.

ATEN Earnings Recap

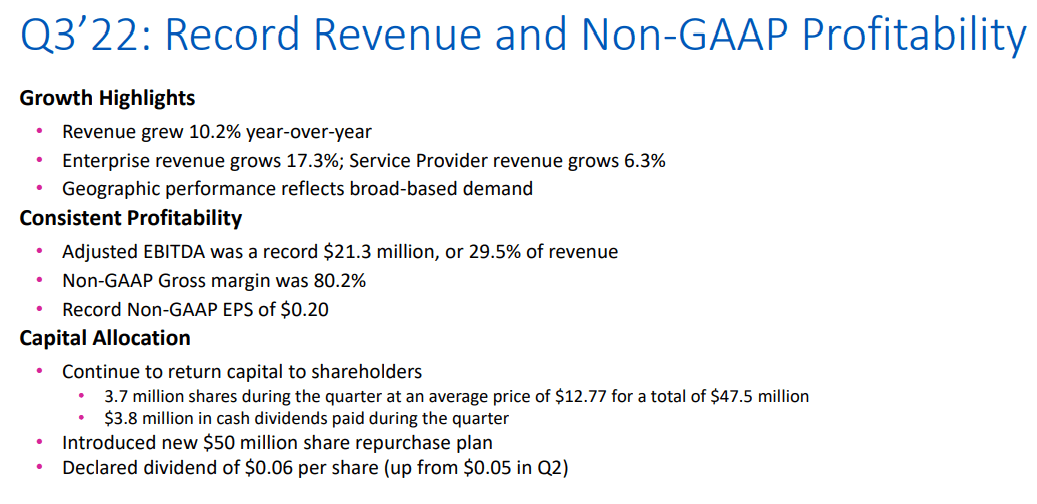

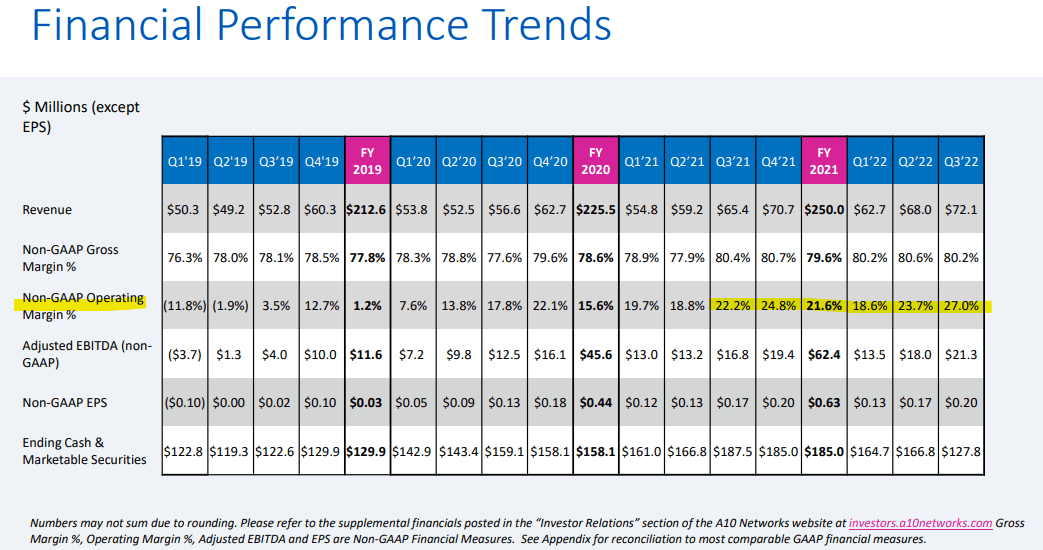

A10 reported its Q3 earnings on November 1st with EPS of $0.20, up from $0.17 in the period last year. Revenue climbed by 10.2% year-over-year to reach $72 million with management noting broad-based demand across its core global regions.

The theme has been the record sales from its hardware products, which include data-center appliances and servers, shipped with its specialized software. The momentum has provided a runway for the higher-margin services segment that is related to post-contract support, training, and technical services. In other words, new customers establish a relationship through the initial product purchase but continue to generate recurring revenues through various fees and a growing number of subscription options.

source: company IR

The other dynamic at play is the shifting composition towards enterprise customers, now representing 38% of the business from 35% last year. This is important because it confirms a diversification away from the company's historical concentration on "service provider" customers, being mainly large telecom players. During the earnings conference call, management noted that A10 is capturing market share with data suggesting superior performance in head-to-head testing versus alternative solutions.

The result is that the gross margin has steadily trended higher over the last few years while the adjusted operating margin at 27.0% in Q3 climbed from 22.2% in the period last year. This quarter, adjusted EBITDA at $21.3 million was up from $16.8 million in Q3 2021. The expectation is for these trends to continue.

source: company IR

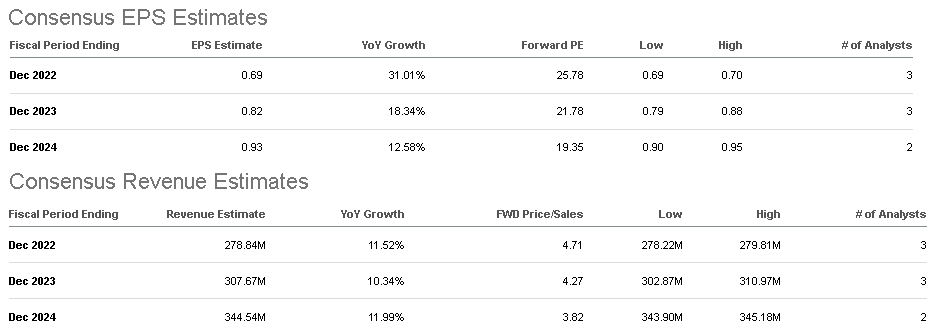

According to consensus, the forecast is for full-year EPS to reach $0.69 representing a 31% increase over 2022. The company is well on track to meet this target considering the trends from the first nine months of the year. Looking ahead, the market sees continued earnings growth of 18% in 2023, moderating to 13% by 2024. The driver here considers top-line momentum to remain above 10% annually, including 11.5% this year, which is consistent with management's current guidance for 2022 revenue growth between 10%-12%.

In our view, there is upside to these estimates as part of the bullish case for the stock, particularly in a scenario where the macro environment cooperates. ATEN would benefit from stronger global growth and a rebound in the Capex cycle of service providers that continue to build out their infrastructure. Adding just a few points to the revenue estimates would allow EPS to outperform expectations.

Seeking Alpha

ATEN Dividend Growth

A big development this quarter was the 20% dividend hike to a new quarterly rate of $0.06 per share. This was the first increase since the company initiated the payout in 2021.

While the forward yield on the stock at 1.3% is modest, the understanding is that there is room for annual dividend growth in line with earnings to maintain a payout ratio of around 30%. The effort is backed by the rock-solid balance sheet that ended the quarter with $128 million between cash and marketable securities against zero long-term financial debt.

Separately, ATEN has also been active with buybacks, repurchasing $80 million in stock thus far this year. On this point, the Board of Directors declared a new $50 million increase to the buyback authorization. Putting it all together, ATEN is proving to be shareholder friendly in terms of its capital allocation facilitated by strong underlying cash flows.

Is ATEN Undervalued?

With a current market cap of $1.4 billion, A10 has established itself as a small-cap leader checking off many boxes for consideration as an investment. From a top-down perspective, the company solutions capture many secular market growth drivers between the ongoing adoption of cloud applications, increased complexity of networks, and the growing importance of automation. What these buzzwords have in common is the need for data protection and cybersecurity. Evidence the company is capturing market share means customers are finding value in the solutions.

source: company IR

The key to understanding A10 is that its particular market segment within "infrastructure software" crosses over into various categories like DDoS protection, Gi/SGi firewall, CGN products, SSL Insight, and data center protection appliances. By this measure, it's difficult to draw a direct connection to a single competitor that offers a similar set of solutions for all markets.

On this point, we can bring up companies like F5 Inc (FFIV), Cisco Systems Inc (CSCO), NetScout Systems Inc (NTCT), Fortinet Inc (FTNT), and Qualys Inc (QLYS) among its peers. ATEN finds its place in the middle of the group in terms of its valuation premium, trading at a forward P/E of 26x and 15.5x on an EV to forward EBITDA multiple.

We note that the players more on the cybersecurity side like Fortinet command a higher earnings multiple at 45x consistent with the stronger growth opportunity in the segment compared to the more infrastructure players that carry a discount.

The argument we make is that A10 tilting towards the cybersecurity side can be considered undervalued and has room for some valuation multiples expansion to converge with the high-growth players. The company's momentum in margins with a higher proportion of recurring revenue can justify a higher premium.

With the exception of Juniper Networks and Cisco Systems, ATEN is also one of the few infrastructure/ cybersecurity stocks that pay a regular dividend which adds to its attraction. That fundamental quality which includes an outlook for continued earnings growth, and recurring free cash flow generation with the rock-solid balance sheet rounds out the strong points for the stock.

ATEN Stock Price Forecast

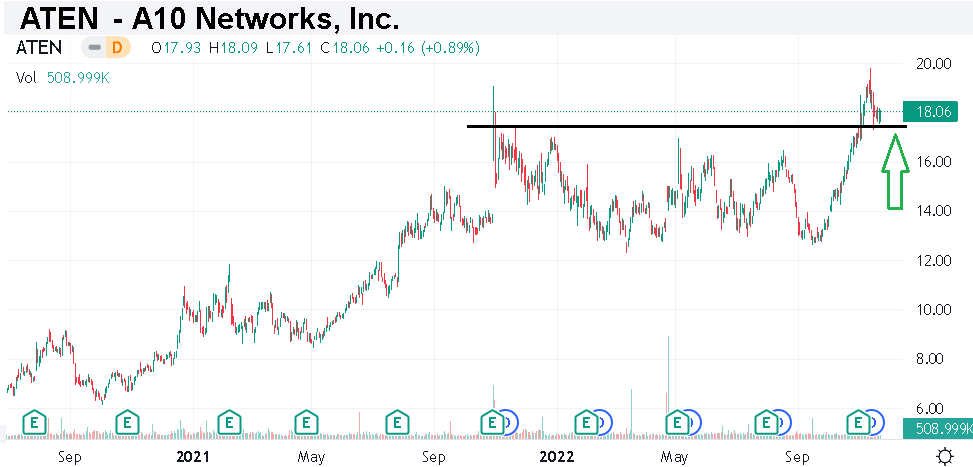

Shares of ATEN at $18.00 are currently up 9% in 2022, including a sharp rally from when the stock was trading under $13.00 as recently as October. It's clear that sentiment has turned positive with the market recognizing the operating and financial tailwinds that have been confirmed with the latest Q3 earnings release. From the chart, ATEN has broken out above an important trading range that was in play all year to retest the 2021 all-time high.

There is a case to be made the company's outlook is stronger than ever which can support more upside into the next year. We mentioned the bullish case where earnings can outperform expectations going forward and this is a case where ATEN is well-positioned to lead the broader market higher.

We rate shares as a buy with a price target for the year ahead at $23.00 representing a 27.5x multiple on the current consensus 2023 EPS. A higher multiple will be consistent with the market pricing ATEN as more of a cybersecurity name. The way we see it playing out is that a strong Q4 for the company can be accompanied by positive guidance as the catalyst for the next leg higher.

In terms of risks, a deterioration to the global macro outlook defined by a deeper recession would likely undermine sales demand and pressure shares lower. The operating margin will be the key monitoring point over the next few quarters.

Seeking Alpha

Gloss